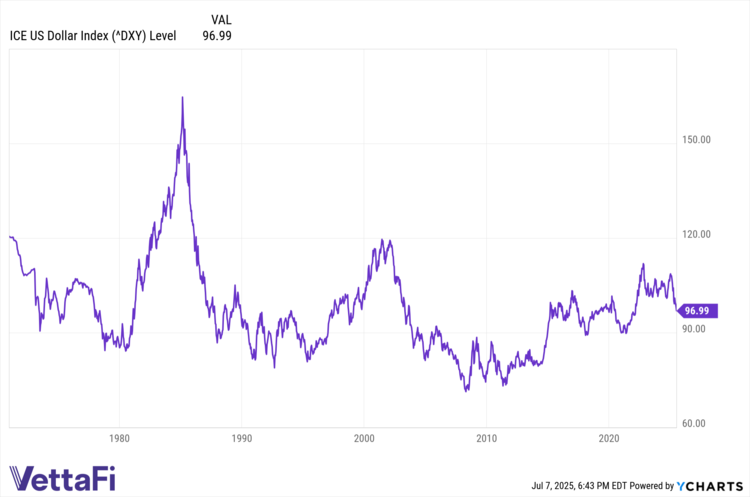

Don’t hold your breath for dollar recovery odds this summer. After the worst first half for the U.S. dollar since Nixon’s presidency, risk factors remain elevated in the near term. Given the macroeconomic regime shift currently underway, investors should understand what dollar weakening may mean for their portfolios.

The U.S. dollar fell 10.7% in the first half compared to global currencies. The rise of a new, aggressive U.S. tariff policy rocked global markets and global trade in the second quarter. The recently announced “reciprocal” U.S. tariff deadlines pushed back from their previous July 9 deadline to August 1 only underscores the unpredictable and volatile nature of U.S. tariffs under the current administration.

“The President’s strategic uncertainty is producing some short term results, but continuing to threaten exorbitant tariff rates is just paralyzing for business decision-making and erodes trust with our allies and major trading partners,” Jake Colvin, president of the National Foreign Trade Council, told the WSJ.

In addition to ongoing trade policy volatility, the recent passage of the spending bill in Congress adds further pressure. It increases U.S. deficits, already a rising worry for many investors, to $4.1 trillion by 2034 and $5.5 trillion if temporary measures are made permanent, reported the nonpartisan Committee for a Responsible Budget.

“Our fiscal condition is currently precarious, with debt-to-GDP soaring towards an all-time record, interest costs surging past nearly all other parts of the budget, and the Social Security and Medicare trust funds heading towards insolvency,” said Maya MacGuineas, president of the Committee for a Responsible Budget, in a press release on July 3, 2025. The reconciliation bill only exacerbates all of these problems, further eroding confidence in U.S. bonds and the dollar.

What Does U.S. Dollar Weakness Mean for Investors?

While the dollar slid precipitously in the first half, it began its decline from a relatively elevated position compared to historical averages. So, although down, the dollar is still a far cry from 2008 GFC crash levels.

A weakening dollar creates a complicated backdrop for U.S. investors. One on hand, dollar weakness compared to other currencies benefits exports. Cheaper costs of goods could result in increased demand for U.S. goods overseas. However, trade tensions and erosion of trust in the U.S. as a trade partner add layers of uncertainty. And just as it benefits exports, dollar weakness increases prices for imports, squeezing U.S. consumers further.

On the other hand, the weakening dollar erodes returns of U.S. equities when crossing the border. For foreign investors that convert S&P 500 returns back into local currencies such as euros, returns are diminished. At the same time, investing internationally can boost gains for U.S. investors converting back to the dollar. In such an environment, international stocks become more attractive by default, further diminishing potential U.S. demand.

For bond investors, dollar weakness and diminished investor confidence in U.S. exceptionalism, combined with the rapidly ballooning U.S. deficit, may make U.S. bonds an increasingly hard sell. U.S. bond auctions and Treasury yields will come under increasing scrutiny as markets parse foreign demand and impacts of the global regime shift currently underway.

Overall, the market environment remains a dynamic and potentially fraught one this summer. Fresh tariff stress only underscores the risks to U.S. dollar strength this year. Active management could prove a boon in the second half and beyond as inflation, tariff, and macro risk narratives unfold.

T. Rowe Price, an active manager with almost 1,000 investment professionals globally, offers a suite of actively managed ETFs for investors. These include the T. Rowe Price International Equity ETF (TOUS ) and the T. Rowe Price Ultra Short-Term Bond ETF (TBUX ).

For more news, information, and analysis, visit our Active ETF Content Hub.