Demand from advisors and investors alike for equity income strategies isn’t necessarily a new phenomenon. These strategies have long filled an important niche across a range of portfolio needs. Equity income funds can help diversify one’s yield portfolio away from the bond space, lower potential risk, and provide a hybrid blend of cash flow and long-term returns.

Some investors consider covered call ETFs as a potential source of equity income. While these funds can generate yield, they may also present transparency challenges, as investors and advisors often have limited visibility into the call option strategies used by fund managers to produce that income.

Today, investors don’t have to accept the uncertainty that often comes with call‑option strategies. Autocallable income ETFs provide an approach to equity income strategies, offering clearer insight into how the strategy works.

CAIQ Showcases Autocallable Transparency in Action

For example, take a closer look at how the Calamos Nasdaq Autocallable Income ETF (CAIQ) functions. CAIQ’s strategy focuses on seeking to deliver equity income through a laddered portfolio of autocallable yield notes.

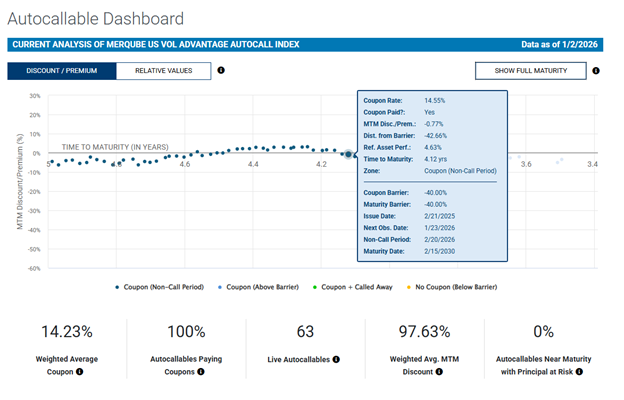

CAIQ’s autocallable yield notes offer more transparency than one might expect from a traditional covered call ETF. To start, each of CAIQ’s laddered autocallables uses the same index and barrier level. These notes all use the MerQube Nasdaq-100 Vol Advantage Autocallable Index with a barrier level of -30% and a 70% coupon barrier (observed monthly).

What this means is that as long as the MerQube index stays above the -30% threshold, CAIQ’s autocallables can continue to deliver income on a monthly basis until the note is called. If the index drops past -30%, income payments will stop until the index rises above the barrier level. Should the note get called while below its barrier level, investors may be subject to a partial loss of principal. The Calamos Autocallable Dashboard displays all autocallables in the underlying index, plus the specifications of each autocallable.

CAIQ is also offering the potential for income through the equity market. As of January 13, 2026, the fund has a weighted average coupon of 17.86%. Unlike traditional autocallable yield notes, fees are relatively lower and transparent and only 0.74% for each ETF.

CAIQ is not the only autocallable income ETF offered within the Calamos lineup. Calamos also has the Calamos Autocallable Income ETF (CAIE ), which recently surpassed $500 million in assets under management as of January 6, 2025. Much like CAIQ, CAIE takes a laddered approach to income through autocallable yield notes. However, while CAIQ’s notes provide access to the Nasdaq-100, CAIE’s autocallables instead focus on the S&P 500.

Regardless of which fund an investor chooses to invest in, these Calamos funds offer a compelling, transparent promise for both income and risk-managed principal. This makes CAIQ and CAIE particularly attractive vehicles for navigating potential volatility as the new year progresses.

For more news, information, and analysis, visit the Alternatives Content Hub.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

An investment in the Fund is subject to risks, and you could lose money on your investment in the Fund. There can be no assurance that the Fund will achieve its investment objective. Your investment in the Fund is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund can increase during times of significant market volatility. The Fund also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund’s prospectus.

The principal risks of investing in the Calamos Autocallable Income ETF and the Calamos Nasdaq Autcallable Income ETF include: autocallable structure risk, contingent income risk, early redemption risk, barrier risk, authorized participant concentration risk, calculation methodology risk, cash holdings risk, correlation risk, costs of buying and selling fund shares, counterparty risk, credit risk, derivatives risk, equity securities risk, index risk, interest rate risk, investment in a subsidiary, laddered portfolio risk, liquidity risk, market maker risk, market risk, new fund risk, non-diversification risk, premium-discount risk, secondary market trading risk, swap agreement risk, tax risk, trading issues risk, valuation risk, and volatility target index risk.

Autocallable Structure Risk: The Fund’s returns are correlated to the performance of a synthetic portfolio of autocallable notes tracked by the Laddered Autocall Index. Autocallable notes have specific structural features that may be unfamiliar to many investors.

Contingent Income Risk: Coupon payments from the Autocalls are not guaranteed and will not be made if the Underlying Index falls below the Coupon Barrier on observation dates. This means the Fund may generate significantly less income than anticipated during market downturns.

Early Redemption Risk: Autocalls in the Portfolio may be called before their scheduled maturity if the Underlying Reference Index reaches or exceeds the Autocall Barrier on observation dates. This automatic early redemption could force reinvestment of that portion of the portfolio at lower rates if market yields have declined.

Barrier Risk: If the Underlying Reference Index falls below the Protection Level Barrier at the maturity of an Autocall in the Portfolio, that portion of the Portfolio will be fully exposed to the negative performance of the Underlying Reference Index from its initial level. This conditional protection creates a binary outcome that can result in sudden, significant losses if barriers are breached.

The MerQube Nasdaq-100 Vol Advantage Autocallable Index is designed to reflect the collective performance of a theoretical portfolio of 52 to 260 synthetic Autocallables arranged in a laddered structure with staggered entry points with similar fixed parameters (the “Parameters”) as described below within the section entitled “Autocallable Index Portfolio Characteristics”.

Nasdaq® is a registered trademark of Nasdaq, Inc. (which with its affiliates is referred to as the “Corporations”) and is licensed for use by Calamos Advisors LLC. The Fund has not been passed on by the Corporations as to their legality or suitability. The Fund is not issued, endorsed, sold, or promoted by the Corporations. THE CORPORATIONS MAKE NO WARRANTIES AND BEAR NO LIABILITY WITH RESPECT TO THE FUND.

Calamos Financial Services LLC, Distributor

© 2025 Calamos Investments LLC. All Rights Reserved.

Calamos® and Calamos Investments® are registered trademarks of Calamos Investments LLC.