Here’s the problem with the crypto space right now: There’s quite literally so much cool stuff going on that it’s becoming legitimately impossible for any one person to even pretend to keep up with every interesting new project. Imagine I told you that I was up to speed on every cool small business idea in the world. You know I’d be lying. But that’s what the pace of growth is like in crypto right now, and that’s honestly a problem.

Why Tokenization Matters

At the heart of most of what’s interesting right now in crypto are “tokens.” For the crypto-noobs like myself, a key concept here is the difference between a “coin” — that’s what bitcoin and ethereum are, for instance, a digital currency of a sort that is issued, used, and managed on its own blockchain. That’s the unit of account for the big distributed ledgers everyone’s so excited about. For the most part, people are starting to grok this core idea: I have some bitcoin, and I keep it in a wallet, which is simply an address that the blockchain knows how to find and work with. In the case of Ethereum, my “wallet address” is also what’s associated with tokens.

Ethereum, because it was designed from the beginning not just to manage the coin ETH but to actually be a computational platform, has a lot of extensibility, and one of the first big use cases was a standard called ERC-20. ERC-20 is just a standard, like a building code, that says how to make a token that can be moved around and stored using Ethereum and Ethereum wallets. That’s it — what those tokens do or represent is just up to the folks making and using them. The token is just an immutable digital item, in the same way that, for instance, a share of stock is a token.

A share of stock is a token that gives me certain legal ownership rights to a company. Sometimes I get to vote on stuff, sometimes I get a claim on cash flows. But ultimately, my share of Tesla is a token of ownership, and I can move it around an ecosystem. I can sell it or buy it through my broker, on or off exchanges. I can pledge it as collateral to borrow against to do more stuff. I can get a physical copy and stick it in a safe if I really want to. Or I can move it from Schwab to Fidelity with a little paperwork. It’s just an ownership token.

So we know how financial tokens work — we use them every day in this business.

Token Sets? Token ETFs?

There are now quite literally thousands of ERC-20 tokens out there — that is, fungible tokens. Tokens where mine is the same as yours, and they can be created, destroyed, and used fractionally or en masse. Many of those tokens are connected to projects with significant financial backing. For example, Axie Infinity, the game/unregulated UBI for pre-teens system that I wrote about a few weeks ago, has an ERC-20 token called AXS, which is used in the game and as a medium of exchange for the game’s trading infrastructure. MANA is used in a game/environment called Decentraland to buy, well, fake land.

Given that it’s nearly impossible to pay attention to all this and still have a life, there clearly needs to be a way to approach these tokens in groups, if we were going to take a financial flier and just buy a bunch to hold on to because number go up.

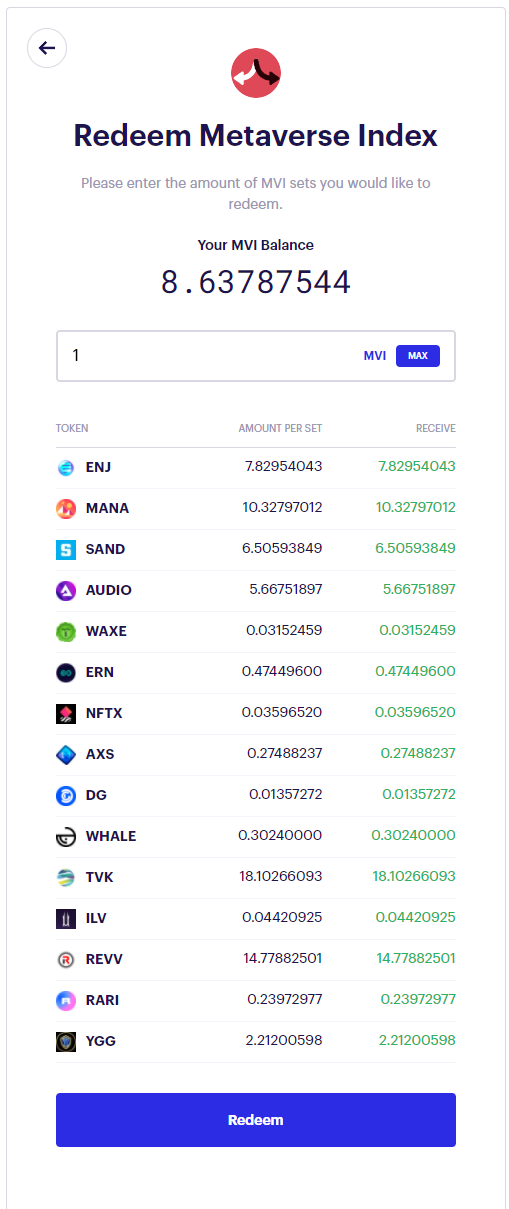

Enter TokenSets — an extraordinarily elegant set of more smart contracts on Ethereum that basically create exchange traded funds. Here’s one I own, called MVI, or the MetaVerse Index.

I bought this token (MVI, also an ERC-20 token) by swapping some ETH for MVI using a swap facility. That’s how most folks do it — you basically just use a decentralized exchange, which is another fancy word for “another smart contract that runs a liquidity pool to engender swaps between digital assets.” (I wrote about those in February, if you want the wayback machine.)

What I now “own” in my wallet is eight-and-change MVI tokens. However, at any point I could hit the “Redeem” button above and (after some gas fees), all those other tokens would just appear in my wallet, and my MVI would disappear. I could do this just as a cheaper way of getting this basket (as opposed to making a dozen individual transactions one by one). Or I could have staked tokens into liquidity pools to act as an automatic authorized participant to keep the values in line.

If that sounds familiar, it’s because this is essentially the ETF creation/redemption process, but just for actual individual human beings.

What’s wild about things like this is where the pieces lead. TokenSets — the underlying set of smart contracts that are driving most of the interesting collective-investment projects I’ve stumbled across — looks like just another scrappy community project. And indeed, the core contracts out there to do things like MVI are all free. There’s no “streaming fee” (get used to that, it’s the new buzzword for “management fee”) that’s cut out of each transaction and sent to a secret wallet or anything. They’re just services out there on the blockchain that you can use for the cost of gas.

But underneath, there’s a company: Set Labs Inc. It’s a small team of folks who have raised $14 million to build all this out from some 20 investors in a seed and a round. Presumably, they’ll make money by being in the center of this evolving ecosystem and building cool products that they will get paid for, but that’s sort of irrelevant. Nobody in crypto seems to be concerned with something as trivial as “getting paid in currency to do a thing.”

But Set Labs Inc. isn’t “behind” MVI. The actual project to make and manage MVI is from a group called IndexCoop. IndexCoop isn’t a company at all; it’s a Decentralized Autonomous Organization, or DAO.

What the Heck Is a DAO?

A DAO is a company that has no leadership structure. Everything is done by vote using tokens (of course, this time called a governance token). In the case of IndexCoop, they have their own native token called INDEX. If you have a lot of INDEX, you can determine what new product they make, for instance.

DAOs are themselves super interesting. Just last night, a recently formed DAO called ConstitutionDAO tried and failed to buy one of the 13 physical copies of the U.S. Constitution, largely just because. The idea was to pool a LOT of money together to go buy a big thing, and then everyone who contributed the money would somehow get to vote on what to do with it.

To get the money into the DAO, it used something called Juicebox, which is essentially a kind of automated escrow agent for DAOs, or a kind of programable treasury function. It itself is a collection of seven smart contracts that control core functions (like accepting certain kinds of coins as payment, like ETH, and managing the distribution of tokens from a project). It’s essentially the rails for kickstarter on DeFi. It’s also thousands and thousands of lines of code that I hope someone read and audited.

So ConstitutionDAO is an organization, sort of run by a team that more or less uses token ownership to decide what to do and to reward work being done, kind of like a capitalist version of the original open source standards movements. And in the process, it collected a lot of money (not just pledges, actual ETH deposited through the Juicebox contract suite to pool money for a purpose worth over $40 million).

That it failed is actually sort of unimportant. But if it had won, the legal issues would have been fascinating. The idea of a DAO is awesome — it’s like democracy at a fundamental level, just not for governments. Wyoming has started the process of at least recognizing a DAO as a thing, and it’s also worth noting that even under the Wyoming provisions, all that really happens is that the DAO registers as a plain old Wyoming LLC, with a lot of regular old responsibilities and paperwork that somehow “the DAO” would need to do, down to having a human being who acts as the rep in Wyoming for the DAO. Let’s just put it down to “it’s complicated, but exciting.”

And now that it’s failed, the folks behind it aren’t even sure how to unwind it. The smart contracts are sitting on over $40 million worth of ETH locked in a box, and nobody really has any idea exactly what to do next. This official blog post pretty much says it all:

The Meaning of Tokens and the Bridge to Asset Management

So how do we bridge from this world of DAOs, which are incredibly cool but still very much a new thing in terms of legal structure and what they can do, and TokenSets like MVI, which are also still very much a new thing in terms of legal structure and what they can do, towards a world of “real finance?”

The big issue is what a token actually means. The fun stuff around the “meaning” or “reality” in tokens is happening in NFTs. Here, there is a massive disconnect between what people think they’re buying (signatures) vs. what they think they’re buying (art) in many cases.

Perhaps the most interesting little salvo in the token wars to come happened just this week, when somebody put up a torrent of quite literally every NFT minted on Ethereum and Blockchain. That is, all the artwork, as referenced in all those NFT contracts. The reason this is interesting is because Pirate Bay, which is this is based off of, lived/lives a sketchy life of constantly avoiding DMCA copyright takedown notices.

The juicy part here is the question of who’s gonna sue. Yes, Beeple can (and probably will) go after them, but it’s a whole lot less clear whether someone can complain about their Bored Ape. On the website, there’s a paragraph about “you own your ape,” but I haven’t been able to find any actual legal language transferring anything in the ecosystem. (@DaveNadig on twitter, DMs open!)

But while NFTs may be somewhat inherently worthless (or at best, very much find their worth in the eye of the beholder), that’s not true for all tokens. Right now, if you aren’t a U.S. citizen, you can use a Tesla token at FTX to play around in their admittedly walled garden. They do this by bridging between a traditional brokerage account (with all the know-your-customer requirements) and a crypto environment. Because of the legal issues, all those equity tokens stay inside the platform. But in that case, the Tesla token, far from being valueless, represents a real claim on a real share of Tesla stock, which you can redeem the token for if you want. Put another way, if you owned that Tesla token directly on the blockchain, then all the crazy stuff we’ve been talking about could have “TSLA” in the mix instead of “ETH” or “MVI” or “AXS.”

The Point

The point is that all of these crypto ecosystems are living side by side: the very real and smart stuff being done at IndexCoop and TokenSets, the bonkers “let’s buy the Constitution with a DAO” stuff, the “NFTS are silly hype” stuff, and the “use my Tesla tokens as collateral for futures trading” stuff. It’s all crypto, it’s all there, and every angle of it is interesting.

Because of this, crypto spaces — and indeed, the markets themselves around the world — feel like they are in a particularly volatile flux state. It is simultaneously true that the most interesting financial innovations in nearly a century are happening right now, and at the same time, some wild scams, malfeasance, and generalized stupidity are going to keep making headlines, based on precisely the same underlying technologies.

That’s not scary. That’s exciting. What’s scary is my growing conviction that we, as a country, are going to blow it, and cede the field — and to some extent, America’s future — to stateless capitalists who coopt the future with regulatory arbitrage. Decentralization is great. But with no central authority, we will rely on a cascade of “trusted” third parties who we will trust, most likely, simply because they have all the money. I, for one, would love to play in the sandbox where we can bring TradFi into the future with DeFi, instead of devolving into two unequal systems where, most likely, the little guy will get crushed in between.

For more news, information, and strategy, visit the Crypto Channel.