Summary

- Nine constituents in the broad Alerian Midstream Energy Index (AMNA) spent a combined $956 million on equity repurchases in 2Q25.

- Buyback activity increased relative to recent quarters in terms of the dollars spent on repurchases and the number of companies participating as equity weakness created an opportunity.

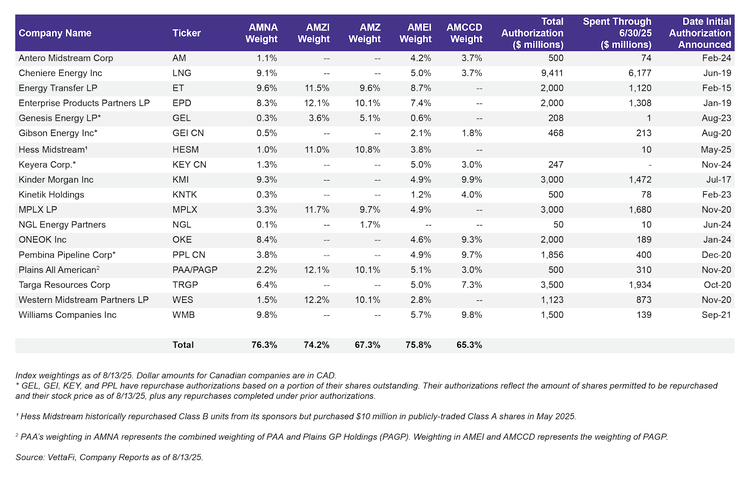

- Over 75% of AMNA by weighting has a buyback authorization in place, representing 18 constituents.

With equity weakness in the second quarter, midstream MLPs and corporations were more active with buybacks than they have been in recent quarters. The number of companies completing buybacks and the absolute dollar spend were up significantly from 1Q25. This note details 2Q25 repurchase activity and discusses how buybacks fit into midstream’s capital allocation plans.

Midstream buybacks approach $1 billion in 2Q25.

For 2Q25, nine constituents of the broad Alerian Midstream Energy Index (AMNA) repurchased $956 million in equity in total, compared with six names repurchasing a combined $693 million in equity in 1Q25 (read more). The last time this many names were active with buybacks in a quarter was two years ago in 2Q23. This also marks the highest aggregate spend on repurchases since 2Q24, when AMNA constituents collectively had $1.02 billion in buybacks.

For 2Q25, Targa Resources (TRGP) led the way with $324 million in repurchases and announced an incremental $1 billion share repurchase authorization. TRGP was followed closely by Cheniere Energy (LNG) at $306 million. Cheniere has typically had the highest quarterly buyback spend among midstream companies in recent years.

MLPs Enterprise Products Partners (EPD) and MPLX (MPLX) repurchased $110 million and $100 million in common units during 2Q25, respectively. While MPLX’s buybacks were consistent with 1Q25, EPD’s marked a significant increase from 1Q25 repurchases of $60 million. MPLX upsized its buyback authorization with an incremental $1 billion approved.

Of note, Kinetik (KNTK) repurchased $73 million in equity during the quarter and bought back another $100 million in shares between July 1 and August 6. Antero Midstream (AM) repurchased $17 million in equity during 2Q25. Other names with smaller repurchases include Plains All American (PAA/PAGP) and NGL Energy Partners (NGL).

Hess Midstream (HESM) has historically been excluded from the table below, because units were being repurchased from its sponsors. However, in May, HESM repurchased $10 million in publicly traded shares, alongside a $190 million repurchase from its sponsors. In August, HESM announced an agreement to repurchase $70 million in publicly traded shares, as well as $30 million from its new sponsor, Chevron (CVX).

The table below shows the energy infrastructure companies with buyback authorizations and their total repurchases as of June 30, 2025. The table also includes each company’s weighting in AMNA, the "Alerian MLP Infrastructure Index":https://vettafi.com/issuer-services/indexing/energy/alerian-energy-infrastructure/AMZI/ (AMZI), the Alerian MLP Index (AMZ), the Alerian Midstream Energy Select Index, and the "Alerian Midstream Energy Corporation Dividend Index":https://www.vettafi.com/indexing/index/amccd (AMCCD). The majority of the indexes by weighting as of August 13, 2025 have buyback authorizations in place.

Buybacks still a tool on the shelf for many companies.

For most energy infrastructure companies, dividend growth tends to be the highest priority for returning cash to shareholders, while buybacks are a nice tool for enhancing shareholder returns. As discussed last week, the vast majority of midstream names are growing their dividends (read more). However, a smaller subset of midstream names is active with buybacks, with a handful being particularly consistent. Authorizations are generally more likely to be used when equities see sharp sell-offs as in April (AMNA was down ~13% at its relative bottom in April).

Clearly, companies want to allocate capital where they can generate the highest return for shareholders. For many, investing in growth projects is a higher priority today given a slew of opportunities tied to growing natural gas demand (read more). Besides growth projects, dividend growth and debt reduction could also be prioritized ahead of buybacks. One of the appeals of repurchases is their flexibility and the ability to be opportunistic, relative to the greater commitment of a dividend.

Bottom Line

Midstream/MLP buyback activity picked up with the equity weakness in 2Q25. But buybacks continue to compete with other uses of capital, including dividend growth and new projects.

For the latest updates on the energy infrastructure space as well as a look ahead, don’t miss “Checking MLP/Midstream Fundamentals as 2026 Approaches” on Wednesday, September 3, 2025 at 2:00 p.m. ET. Follow the link here to register and receive one hour of CE credit for attending.

Looking for midstream insights in your inbox? Subscribe here keep a pulse on midstream investing through our weekly updates.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMZ is the underlying index for the JPMCFC Alerian MLP Index ETN (AMJB), the ETRACS Alerian MLP Index ETN Series B (AMUB), and the ETRACS Quarterly Pay 1.5x Leveraged Alerian MLP Index ETN (MLPR). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX). AMCCD is the underlying index for the Alerian Midstream Energy Dividend UCITS ETF (MMLP.LN).

Related Research:

1Q25 Midstream/MLP Buybacks Steady; More on Deck in 2Q?

2Q25 MLP/Midstream Dividend Recap: MLPs Deliver Growth

Rising Electricity Demand Needs Natural Gas & Midstream

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, AMJB, AMUB, MLPR, ENFR, ALEFX, and MMLP.LN, for which it receives an index licensing fee. However, AMLP, MLPB, AMJB, AMUB, MLPR, ENFR, ALEFX, and MMLP.LN are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, MLPB, AMJB, AMUB, MLPR, ENFR, ALEFX, and MMLP.LN.

For more news, information, and analysis, visit the Energy Infrastructure Content Hub.