Summary

- Midstream/MLPs have seen less impressive performance in 2025 after generating double-digit percentage total returns each year since 2021.

- In 2026, midstream companies are expected to continue executing on dividend growth and opportunistic buybacks as they generate free cash flow.

- Companies are generally expected to see moderate EBITDA growth next year, even as a muted oil price outlook drives expectations for flattish US oil production.

With 2025 winding down, investor attention has already shifted increasingly to 2026 (or perhaps holiday breaks). For the energy space, the 2026 outlook has arguably been an overhang for much of this year given concerns around oil prices and widespread expectations for an oversupplied market into the new year. This note briefly recaps 2025 before diving into the outlook for energy infrastructure into 2026, including the macro landscape, company guidance so far, dividend expectations, and more.

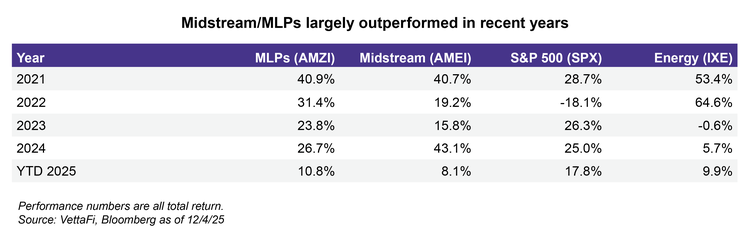

Midstream Takes a Breather in 2025 After Strong Run Since 2021

Midstream/MLPs are on track to end 2025 trailing the S&P 500 (SPX). Through December 4, the Alerian MLP Infrastructure Index (AMZI) was up 10.8%, and the Alerian Midstream Energy Select Index (AMEI) was up 8.1% on a total-return basis, compared to a 17.8% total return for the SPX. WTI crude is down almost 17% so far this year.

AMZI and AMEI have seen double-digit percentage gains for the last four years running, handily outperforming the SPX over the period and outpacing it each year except 2023 (when the SPX rebounded noticeably after a tough 2022). Compared to recent years, 2025 performance is admittedly less impressive as shown below.

Most companies executed well. Dividends were largely increased, several companies used their buyback authorizations, and financial results were generally tracking with guidance. However, there weren’t a lot of beat and raise quarters, and a weaker oil backdrop raised questions around production and volumes for midstream assets. Natural gas infrastructure names that saw strong performance last year faced a higher bar and gains came less easily. A few names saw specific issues in 2H25, including a moderated EBITDA outlook from Hess Midstream (HESM) and Venture Global’s (VG) adverse arbitration rulings (read more). It was a more muted year, but what may be in store for 2026?

Macro Picture Dominated by Oil Caution

Macro fundamentals tend to be in focus for next year. The 2026 Bloomberg consensus price forecast for West Texas Intermediate crude is $59 per barrel (bbl), which is essentially flat. Analysts have been cautious on oil for some time given oversupply concerns from lackluster demand growth and OPEC+ production cut unwinds. While OPEC+ proactively paused unwinds for January through March 2026, an oversupply still looms.

The International Energy Agency (IEA) estimates that the global oil market will be oversupplied by 4 million barrels per day (MMBpd) in 1Q26. While the IEA’s number represents an extreme and is likely overstated, a noticeable surplus is expected. The consensus price forecast for 1Q is $57.50/bbl, reinforcing oversupply expectations but likely not as bad as the IEA is modeling.

Meanwhile, the long-term outlook for North American natural gas demand growth remains robust, driven by liquefied natural gas (LNG) export capacity additions and power demand. In the near term, weather will be a central factor in natural gas prices, and stronger prices could support an uptick in output. The Henry Hub benchmark closed above $5 per million British thermal unit on December 4, marking the highest price since late 2022. For midstream, natural gas pipeline projects and data center deals will continue to be in focus in 2026.

From a production standpoint, the U.S. Energy Information Administration is forecasting flattish oil output next year on average and modest growth for natural gas (more detail here). Estimates have generally been moving higher in recent months. The current oil projection of 13.58 MMBpd for 2026 output is up 300,000 barrels per day from the August forecast.

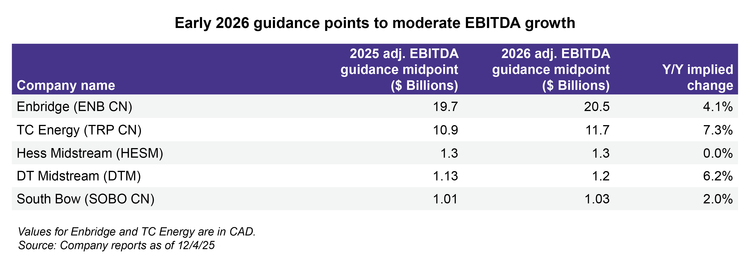

Early Midstream Guidance Points to Moderate Growth for 2026

Despite the muted oil outlook, 2026 financial guidance for most of the names that have provided numbers points to moderate growth as shown below. Kinder Morgan (KMI) announced expectations for 4% adjusted EBITDA growth after the close yesterday. Pembina (PPL CN) is also likely to issue 2026 guidance this week. While most will provide outlooks alongside 4Q24 results, companies are generally expected to see moderate EBITDA growth. Asset changes (acquisitions and divestitures) could augment those trends. More broadly, companies are expected to continue generating free cash flow, supporting dividend growth and buybacks.

Midstream Income Still Shines in Lower Rate Environment

Amid lower interest rates, energy infrastructure yields remain attractive. As of December 4, MLPs (AMZI) were yielding 7.7%, while broader midstream (AMEI) was yielding 5.4%. Midstream MLPs and corporations are expected to continue executing on dividend growth. For most, dividend growth will be in the mid-single-digits, though Targa Resources (TRGP), MPLX (MPLX), Plains All American (PAA/PAGP) and Cheniere Energy (LNG) have guided to heftier growth (read more).

Buybacks Remain a Tool

Over 70% of AMZI and AMEI by weighting having repurchase authorizations in place as of December 4 (read more). If oil weakness drives equity price volatility, companies may take the opportunity to use their authorizations in a more meaningful way. Admittedly, buybacks will likely continue to take a backseat to growth projects for some names, particularly those focused on natural gas infrastructure. With its buyback authorization upsized by $3 billion and expectations for greater free cash flow, Enterprise Products Partners’ (EPD) repurchase activity bears watching next year.

What Will the M&A Landscape Be Like?

The second half of 2025 saw a number of midstream companies snapping up gathering and processing assets in the Permian. TRGP’s acquisition of Stakeholder Midstream provides a recent example, but MPLX and EPD also went shopping (read more). Yesterday, Antero Midstream (AM) announced an acquisition of Marcellus gathering and processing assets and a sale of similar assets in the Utica. As companies compete for volumes in a flattish production landscape, bolt-on M&A may remain attractive into 2026. PAA was also active with acquisitions, as the sale of its Canadian NGL business to Keyera (KEY CN) is set to close in 1Q26.

Aside from Western Midstream (WES) acquiring Aris Water Solutions and ONEOK (OKE) closing the acquisition of EnLink in January, corporate-level M&A was fairly limited within the U.S. in 2025 (Sunoco acquired Canada’s Parkland). Macro uncertainty could potentially make larger deals more challenging.

What Should Midstream/MLP investors Be Watching For?

Into 2026, there are several items for investors to be watching:

- 2026 guidance announcements in 1Q26;

- Dividend announcements, as most names typically increase with the 4Q (February) and 1Q (May) payouts;

- Natural gas pipeline projects, including potential advancement in the Northeast and continued data center deals around the country;

- The potential for permitting reform to pass — one key outstanding item on energy infrastructure’s Washington wish list;

- Oil sentiment — when will it turn and what will drive it?; and

- Production trends in the U.S.

For more on the 2026 outlook, don’t miss our next webcast, “What’s in the Pipeline for MLPs/Midstream in 2026?” on Wednesday, January 14, 2026 at 2:00 pm ET. Follow the link here to register.

Related Research

Midstream/MLP 3Q25 Buybacks Surged to Record Level

3Q25 Midstream/MLP Dividends: Payouts Stay Strong

Energy Transfer Seizes Data Center Growth Opportunities

Beyond the Numbers: Midstream 3Q Earnings Highlights

Midstream MLPs Expand Permian Presence With M&A

Short-term Energy Outlook November 2025

Looking for midstream insights in your inbox? Subscribe here to keep a pulse on midstream investing through our weekly updates.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX).

For more news, information, and analysis, visit the Energy Infrastructure Content Hub.

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, ENFR, and ALEFX, for which it receives an index licensing fee. However, AMLP, MLPB, ENFR, and ALEFX,are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, MLPB, ENFR, and ALEFX.