Summary

- Record high winter electricity costs and voter frustration in the Northeast have triggered a policy pivot. That’s empowering companies to revive stalled natural gas infrastructure projects to bridge the regional supply gap.

- Williams (WMB) is capitalizing on this regulatory thaw by securing permits for its NESE project and reviving the Constitution Pipeline, aiming to connect Marcellus gas to premium markets in New York and New England.

- Enbridge (ENB) and Iroquois are also advancing smaller brownfield expansions to help alleviate supply constraints.

High winter electricity costs are forcing a historic policy pivot in the Northeast. That’s creating a significant growth opportunity for natural gas transportation. Driven by voter demands for lower utility bills, regulators are finally clearing the way to revive canceled pipeline projects and expand existing capacity. Learn more below about the race to unlock Marcellus gas and how this shift is redefining the region’s energy future.

High Costs Force a Northeast Policy Pivot

The Northeast, particularly New York and New England, have historically been more exposed to spikes in natural gas prices during the winter. Although the Marcellus Shale in Pennsylvania is the largest and most economic natural gas source in the U.S., regulatory hurdles and permitting challenges have constrained the infrastructure needed to better supply these markets.

This infrastructure deficit has limited flows to key markets. While pipelines connect the regions today, they are insufficient to handle peak loads, leading to severe disconnects in regional pricing. This volatility is most common during winter periods. Rising natural gas demand from liquefied natural gas exports (read more) and AI data centers (read more) has left the market increasingly vulnerable to price spikes during periods of peak demand.

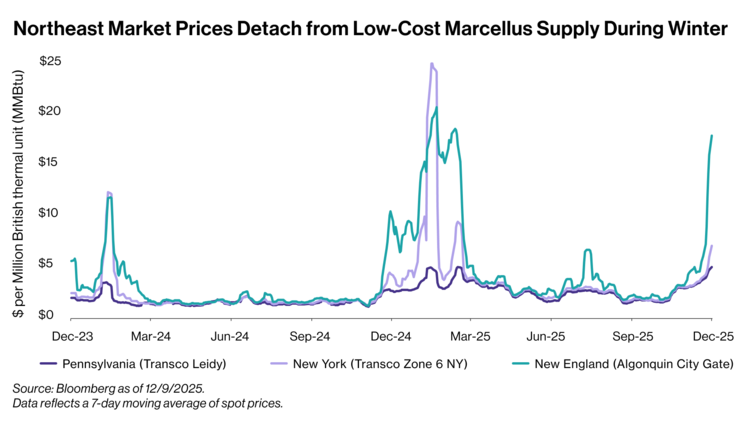

In early December, the U.S. natural gas benchmark Henry Hub closed above the $5-mark for the first time since 2022. Marcellus prices (Transco Leidy) tracked this broader move. From November 7 to December 8, spot prices more than doubled from $2.87/MMBtu to close at $5.89/MMBtu. Pipeline constraints exposed downstream markets to much larger increases. Over that same time frame, New York (Transco Zone 6 NY) spot prices rose from $3.04/MMBtu to $12.24/MMBtu. Meanwhile, New England (Algonquin City Gate) spot prices rose from $3.57/MMBtu to $21.28/MMBtu.

The region’s dependence on natural gas for both heating and power drives this volatility. During winter, heating demand consumes nearly all available pipeline capacity, forcing power generators to compete for the remaining supply. Gas-fired plants set the marginal price for the grid. Therefore, this scarcity forces rates upward and compounds the cost for consumers when usage is highest.

High electricity bills driven by these price spikes were a major issue in the November elections across the Northeast, particularly in the New Jersey gubernatorial race, where the winning campaign pledged to declare a “state of emergency” on utility rates. Similar voter frustration dominated legislative debates in Maine, where a nation-leading 36% surge. in rates spurred calls for reform, and in Connecticut, where the controversial Public Benefits Charge electric bills drove bipartisan demand for relief. This widespread constituent pressure is softening the region’s regulatory resistance. Facing a mandate to lower costs, policymakers are now reconsidering the infrastructure needed to bridge the supply gap.

Williams Offers Larger Solutions to Address Supply Constraints

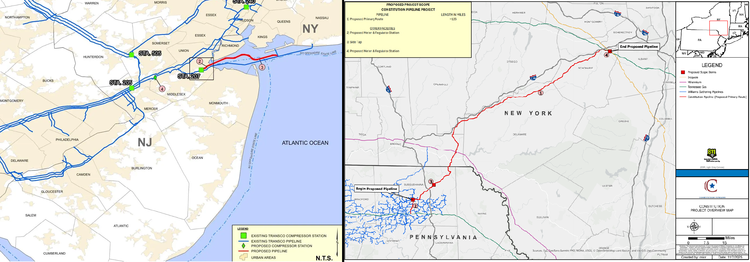

This year, state regulators have cleared long-standing obstacles, resulting in recent permit approvals for Williams’ "Northeast Supply Enhancement":https://www.williams.com/expansion-project/northeast-supply-enhancement/ (NESE) project. Capitalizing on this regulatory shift, Williams has also moved to revive its previously canceled Constitution Pipeline, positioning both assets as central pillars in a renewed strategy to unlock Marcellus gas for the Northeast market.

Williams handles roughly a third of all U.S. natural gas. Anchoring this network is Transco, the nation’s largest volume interstate pipeline system, which alone transports ~16% of U.S. natural gas and delivers roughly half of New York City’s supply.

NESE is designed as a strategic expansion of Transco rather than a greenfield build. Previously canceled in 2024 due to state regulatory opposition, the project would connect additional Marcellus supply to the premium New York City market. With state permit approvals and its FERC Certificate now secured, the project is targeting a 4Q27 in-service date and will add 400 million cubic feet per day (MMcf/d) of incremental capacity.

Building on its momentum, Williams has also revived the Constitution Pipeline, a greenfield project comprising 124 miles of new infrastructure. Constitution represents a new artery that would transport 650 MMcf/d of Marcellus supply directly into the Iroquois and Tennessee Gas Pipeline systems. The project was abandoned in 2020 after an eight-year regulatory battle, and it remains in a standoff today, lacking essential water quality permits from New York. As of last month, Williams had withdrawn its water permit application and was preparing additional filings. To break this deadlock, Williams has argued that the project will support over 2,500 jobs while curbing New England’s rising winter electricity rates.

Smaller Brownfield Expansions Also on the Table

While the Williams projects are quite sizable, there are smaller expansions on the table from Iroquois and Enbridge (ENB CN). Williams’ Constitution Pipeline is designed to physically feed gas into their respective Iroquois and Algonquin networks to reach consumers.

The Iroquois Gas Transmission System, a joint venture between TC Energy (TRP CN) and Berkshire Hathaway (BRK.B), is advancing a compression-only expansion. The ExC Project avoids laying any new pipe and would add 125 MMcf/d of capacity. The project secured a major victory by clearing air permits with the NY regulator in February. The win signals a softening environment. The project is expected to be completed by the end of 2027.

Meanwhile, Enbridge plans to enhance its Algonquin Gas Transmission system. The project would add 75 MMcf/d of capacity and is expected online in 2029.

The value of the region’s existing infrastructure was underscored in August 2024 when BlackRock (BLK) and Morgan Stanley Infrastructure Partners acquired the Portland Natural Gas Transmission System (PNGTS), which transports Canadian natural gas to New England, from TC Energy for $1.14 billion. The deal valued the pipeline at ~11.0x 2023 EBITDA, comparable to the current ~10.6x trailing EV/EBITDA multiple of the Alerian Midstream Energy Select Index (AMEI). AMEI is a broad energy infrastructure index. It consists 75% of US and Canadian C-Corps, including WMB, TRP, and ENB, and 25% MLPs.

Bottom Line

After years of regulatory headaches and challenges, Northeast natural gas pipelines are finally expanding. Smaller expansions using compression will help, while WMB’s NESE expansion and newbuild Constitution pipeline would represent more sizable solutions. The market will be watching closely for a concrete timeline on NESE construction and an update on the Constitution pipeline during Williams’ upcoming investor day in February 2026.

For the latest updates on the energy infrastructure space as well as a look ahead, don’t miss our next webcast “What’s in the Pipeline for MLPs/Midstream in 2026?” on Wednesday, January 14, 2026 at 2:00 pm ET. Follow the link here to register.

Looking for midstream insights in your inbox? Subscribe here to keep a pulse on midstream investing through our weekly updates.

AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX).

Related Research:

2026 Midstream/MLPs: Company-Level Tailwinds Amid Macro Clouds

IEA Report Highlights Tailwinds for U.S. Midstream

Midstream Leans Into AI Data Center Boom

Sizing Up the Next Wave of U.S. LNG Export Projects

Basin Basics: Appalachia Offers More Than Gas

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for ENFR and ALEFX, for which it receives an index licensing fee. However, ENFR and ALEFX are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of ENFR and ALEFX.

For more news, information, and analysis, visit the Energy Infrastructure Content Hub.