Summary

- Williams (WMB) is guiding to a 10+% compound annual growth rate for adjusted EBITDA to 2030, driven by power and transmission projects.

- WMB announced a fourth behind-the-meter power project. Its backlog of power opportunities represents 3x the combined gigawatts of its four sanctioned projects.

- WMB has 13 transmission (pipeline) projects underway, with a significant backlog of additional opportunities representing $15 billion in potential growth capital.

Since its last analyst day in February 2024, some elements of the Williams (WMB) story are very much the same. It still has a track record for solid EBITDA growth, strong project execution and an extensive natural gas pipeline footprint. Other elements of the story are newer, including an exciting power innovations business, expected to contribute significantly to a double-digit growth rate for adjusted EBITDA to 2030. This note discusses key takeaways from Williams’ analyst day last week. Williams is a component of the S&P 500 and a key constituent of Alerian midstream indexes, including the Alerian Midstream Energy Select Index (AMEI).

WMB Raises Long-Term EBITDA Growth Outlook

For years, WMB pointed to a long-term adjusted EBITDA growth target of 5–7%. From 2020 to 2025, the company actually delivered a 9% compound annual growth rate (CAGR) for EBITDA. Notably, this growth was achieved in a more muted backdrop for natural gas than we have today. Specifically, demand growth tailwinds are likely to be more prevalent in the coming years, driven by rising liquefied natural gas (LNG) exports and demand for power generation. WMB highlighted a U.S. natural gas demand growth forecast of 39 billion cubic feet per day (Bcf/d) to 2035, including 20 Bcf/d for LNG exports and 10 Bcf/d for power.

For 2025 to 2030, management has guided to a 10+% CAGR for adjusted EBITDA. Broadly speaking, the growth is coming from “power and pipe.” Management noted that projects already in execution today can underwrite an 8% CAGR in adjusted EBITDA to 2030. As discussed below, WMB has a significant backlog in both power and pipe beyond sanctioned projects, adding confidence to the growth trajectory to 2030 and byeond. Management plans to continue growing the dividend, with near-term increases likely to remain consistent with the 5% annual growth of recent years.

Specific to 2026, WMB initiated an adjusted EBITDA guidance range of $8.05–$8.25 billion, representing 6% growth relative to 2025 at the midpoint. However, management pointed to 7% growth if normalized for asset sales. WMB also expects to spend $6.4 billion in growth capital this year. Spending will largely be directed to high-return, take-or-pay projects, namely four power projects (~$4 billion for this year) and key transmission projects.

Power: New Project Added, Terms Extended, & a Robust Backlog

Some of the key announcements from the analyst day revolved around Williams’ behind-the-meter power business, which is serving data centers. Notably, the company added Socrates the Younger, a 340-megawatt natural gas power project in Ohio, backed by a 10-year agreement and expected online in 2H28. Additionally, the Aquila and Apollo projects in Utah and Ohio, respectively, were upsized and extended to 12.5-year terms from 10 years. The original Socrates project in Ohio for Meta (META) remains on track for completion later in 2026. WMB is investing over $7 billion in these projects. Management has cited a 5x multiple for power projects, implying 20% returns.

In addition to the four projects already announced (1.9 gigawatts combined), WMB has another 6 gigawatts in its backlog, which can support opportunities into the 2030s. Notably, WMB has secured major equipment for the backlog already. Management explained that their initial advantage in the power space was access to turbines, but as projects are executed, their edge relative to competitors will come from solid execution. Management noted a growing recognition that tailored power solutions will be needed by hyperscalers for the long term.

A potentially underappreciated element of the power business is its eligibility for 100% bonus depreciation, which is not the case for regulated natural gas pipelines. Overall, WMB expects $100 million in cash taxes this year but no cash taxes in 2027.

Pipe: Transmission Backlog Grows

While the power opportunity is new and exciting, the transmission (or long-haul natural gas pipeline) business remains WMB’s most valuable segment, with Transco the crown jewel. As a reminder, Transco stretches from Texas to New York, transporting ~15% of the nation’s natural gas. Currently, WMB has 13 transmission projects underway, representing 7.1 Bcf/d of capacity. WMB is on track to grow its delivery capacity by just over 20% from 2025 to 2030 with these projects, reflecting the significant natural gas demand growth on tap for the coming years.

Additionally, WMB boasts an impressive backlog, with another 14.3 Bcf/d of opportunity representing ~$15 billion in potential capital spend. Over the past year, the backlog has grown by over 5 Bcf/d. That translates to more than $3 billion in terms of capex. The rising backlog again reflects the strength of demand growth. While transmission projects are demand-pull opportunities, management noted that these projects and rising demand will drive more volumes into their gathering & processing (G&P) businesses, particularly in the Haynesville.

So What?

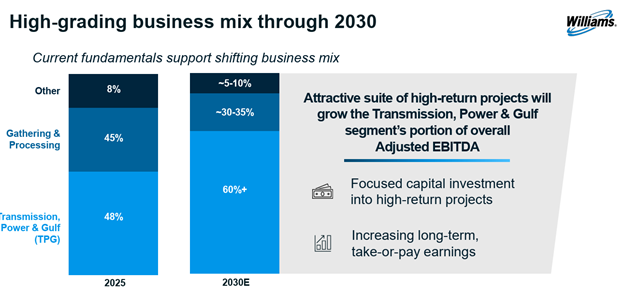

The 10+% CAGR for adjusted EBITDA to 2030 is a key headline from the analyst day. However, it’s also important to note how the business mix is expected to change, as shown below. G&P, which tends to be more sensitive to commodity price moves and production trends, will become a smaller part of the business. Transmission, Power & Gulf will become the majority of the business. By 2030, more than 60% of WMB’s adjusted EBITDA is anticipated to come from long-term, take-or-pay contracts. High-grading the business mix is a key element of the story and can support a stronger valuation over time given transmission trades at higher multiples than G&P businesses.

Looking for midstream insights in your inbox? "Subscribe here to keep a pulse on midstream investing through our weekly updates.":https://www.etftrends.com/energy-infrastructure-content-hub/natural-gas-demand-pull-pipelines-midstream-valuations/

AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX).

Related Research

Natural Gas, Demand-Pull Pipelines & Midstream Valuations

The Nationwide Expansion of Natural Gas to Meet AI Energy Demands

Power Crunch Sparks Northeast Gas Pipeline Revival

Midstream Leans Into AI Data Center Boom

One Big Beautiful Bill and MLP/Midstream Implications

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for ENFR and ALEFX, for which it receives an index licensing fee. However, ENFR and ALEFX are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of ENFR and ALEFX.

For more news, information, and analysis, visit the Energy Infrastructure Content Hub.