Elevated crude prices and a stronger macro backdrop have set expectations for record U.S. oil and gas production next year. Still, large producers have remained disciplined and are so far not materially increasing production. This note digs into current production dynamics and why the resulting tailwinds for midstream infrastructure companies may be more of a 2027 event.

Key Takeaways

- Despite higher crude prices, large producers are maintaining capital discipline and mostly growing volumes marginally through operational efficiency.

- Small, private producers are beginning to add rigs in response to the stronger oil price backdrop, with limited public companies increasing activity.

- A stronger U.S. energy production outlook into 2027 is broadly beneficial for midstream companies, complementing natural gas demand tailwinds.

U.S. Energy Production Forecasts Have Increased Since the War Began

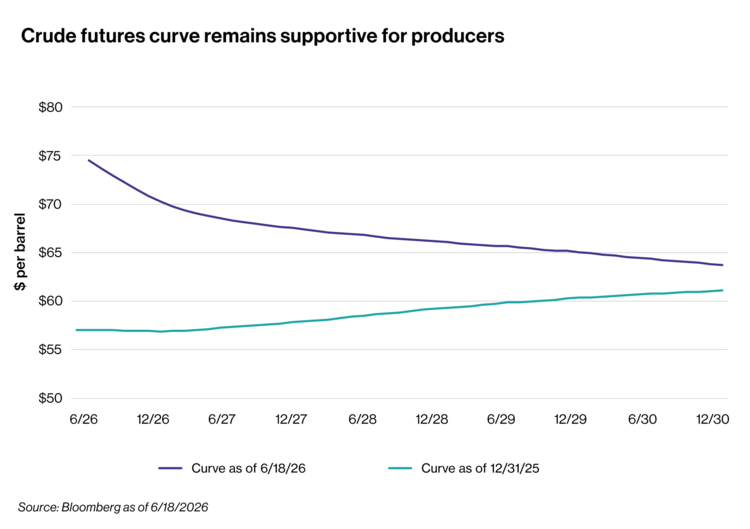

Coming into 2026, the consensus view for oil was very bearish on oversupply concerns. With the Iran war and a rapid depletion of inventories, the outlook for oil prices into 2027 has materially improved, as reflected by the higher futures curve shown below. Even with the recent downward pressure in oil prices across the curve, WTI futures for 2027 are still about $10 per barrel high than at the start of this year.

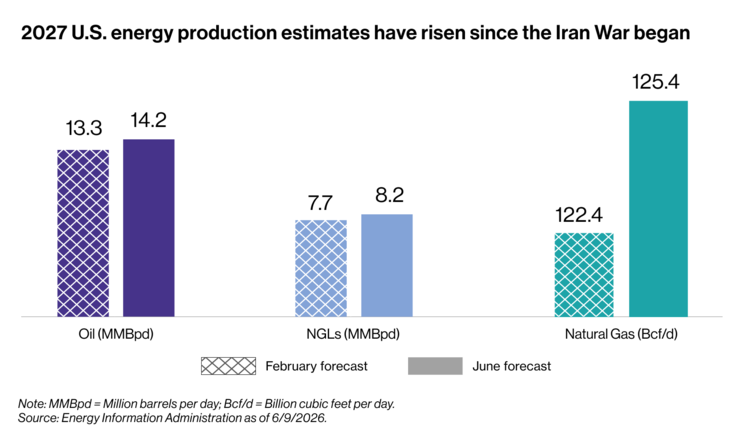

With stronger oil prices, energy production expectations for the U.S. have improved. While the estimate for 2026 oil production has risen by a modest 100 thousand barrels per day (MBpd), the greater growth is expected for 2027. According to the U.S. Energy Information Administration, U.S. oil production is expected to reach a new record high next year and increase by 428 MBpd relative to 2026. This compares to pre-war expectations for a sequential decline in 2027. Natural gas and natural gas liquids (NGLs) are also expected to reach new record highs.

Since the EIA’s latest forecast on June 9, the U.S. and Iran have come to an interim agreement on ending the war, putting significant downward pressure on oil prices. However, questions remain around the reopening of the Strait and a normalization of energy flows. The International Energy Agency (IEA) is warning that a full recovery will not be immediate given the time it will take to remove mines from shipping lanes and for supply chains to normalize. It is widely expected to take months for tanker traffic to resume to normal levels and for energy infrastructure in the Middle East to return to typical rates. In short, some of the weakness in oil prices lately could prove transient.

Where Is Near-Term U.S. Energy Production Growth Coming From?

Most large producers in the U.S. are extremely focused on capital discipline and returning cash to shareholders. Companies have learned hard lessons from growing too much in the shale boom and not focusing enough on returns. In that context, most producers are maintaining discipline, while a select few are increasing activity and spending modestly or squeezing more from their existing budgets.

For example, Chevron (CVX) recently kept its 2026 capex plan unchanged, with management emphasizing “capital and cost discipline no matter what.” Similarly, ExxonMobil (XOM) maintained its 2026 capex guidance, noting that the company’s disciplined approach remains steadfast. Other large producers that maintained full-year capex guidance include EOG Resources (EOG), Occidental Petroleum (OXY), Permian Resources (PR), and Ovintiv (OVV).

That said, some producers are finding ways to grow volumes within existing budgets by leaning on completion backlogs (bringing drilled wells to production), workovers (upgrading older wells), and operational efficiency rather than new drilling. PR raised its full-year 2026 oil production guidance ~2% at the midpoint with capex unchanged, driven by efficiency gains and increased workovers. EOG reallocated capital from dry gas to liquids-focused opportunities in the Delaware and Utica basins in response to the price environment.

Select public companies have decided to increase activity. Diamondback (FANG) raised both its 2026 capex and production guidance with 1Q26 results in response to higher prices. Specifically, the company increased its full-year production estimate to 520+ MBpd, up from initial guidance of 500–510 MBpd, while capex expectations increased 4%. FANG also changed its capital allocation plans, pulling its commitment to return a quarterly percentage of its adjusted free cash flow to shareholders in order to retain flexibility.

ConocoPhillips (COP) provides a similar example of a production and capex hike. COP raised its 2026 capex by 2% at the midpoint due to increased Permian activity in 2H26, namely adding a rig and more spending on non-operated wells. FANG and COP fell 3.5% and 1.9%, respectively, on the dates they reported and underperformed gains seen in broader energy on those days. Investors are still clearly focused on capital discipline. The reaction to the announcements from FANG and COP may preclude other public operators from ramping spending and activity this year.

Smaller Operators and Select Producers Add Rigs

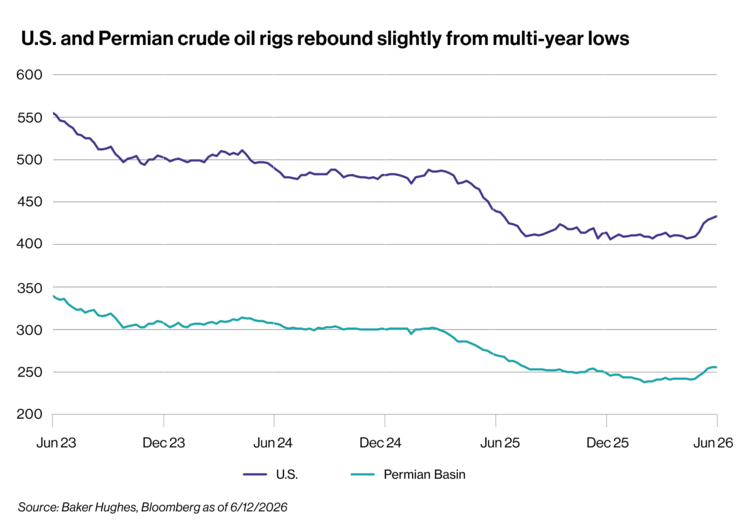

While large producers are maintaining discipline or squeezing more from existing plans, smaller, private companies are more inclined to add rigs to capitalize on the price environment. Per Baker Hughes, the number of operating oil rigs in the Permian Basin has increased from 239 at the end of February to 256 as of June 18.

The ramping rig count aligns well with improved natural gas takeaway capacity from the basin. The natural gas price benchmark for West Texas (Waha) switched last week into positive territory, after trading consistently in negative territory since February. The price improvement coincided with media reports indicating that Kinder Morgan’s (KMI) Gulf Coast Express Expansion was starting up, in line with its mid-2026 target. Additional relief should be coming from the Blackcomb Pipeline and Energy Transfer’s (ET) Hugh Brinson, which are both expected to startup this year.

As can be seen below, the oil rig counts for the Permian and the entire U.S. remain lower than a year ago, when crude was trading in the $65–$70 range, but have ticked up in recent months. About half of the 34 upstream executives surveyed by the Dallas Fed in mid-March signaled plans to drill more wells in 2026 than intended at the start of the year.

While most rigs are being added in the Permian, structural cost reductions have allowed legacy and mature basins like the DJ and Williston to remain economic. Companies can profitably drill wells in U.S. shale outside of the Permian and Eagle Ford with an average oil price of $62 per barrel. With the 2027 futures curve in the high $60’s per barrel as shown above, prices could underpin additional drilling activity in other basins.

Production Growth Implications for Midstream

For midstream, the outlook for U.S. energy production, particularly for oil, has noticeably improved since the start of this year. Oil production growth for 2026 is likely to be more marginal as public companies maintain discipline and may be reluctant to raise capex for fear of investor disdain. Private operators enjoy greater flexibility to capitalize on higher prices.

Production growth for oil is expected to be more noticeable for next year. The higher futures curve into 2027 may pave the way for companies to be a bit more aggressive with their growth plans for next year. To be clear, modest growth is still the expectation, but maybe a company chooses 4% or 5%, instead of 3%, given the stronger backdrop. Permian natural gas bottlenecks should also be largely alleviated, easing the path for production growth from the basin next year.

Expectations for future crude and natural gas production growth add to a strong outlook for midstream companies. Aside from company-level tailwinds from free cash flow and dividend growth, the improved outlook has arguably been supportive for performance. Year-to-date through June 18, the Alerian MLP Infrastructure Index (AMZI) has gained 15.2%, while the Alerian Midstream Energy Select Index (AMEI), which is 25% MLPs and 75% U.S. and Canadian C-Corps, is up 22.4% on a total-return basis. As of June 18, AMZI was yielding 7.3%, while AMEI was yielding 4.7%.

The energy infrastructure space has long enjoyed tailwinds from robust expectations for natural gas demand growth in North America in the coming years. An improving oil outlook augments natural gas tailwinds, making the midstream growth opportunity even more compelling.

Looking for midstream insights in your inbox? Subscribe here to keep a pulse on midstream investing through our weekly updates.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the Alerian Energy Infrastructure Portfolio (ALEFX).

Related Research:

Is Oil’s Peak Behind Us? Does It Matter for Midstream?

Plains All American on the Permian, Distribution Growth

Enterprise (EPD) on Macro Landscape, ‘27 EBITDA Growth

Revisiting Energy Market Impacts From the Iran War

Midstream Prepares for More Permian Natural Gas

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, ENFR, and ALEFX, for which it receives an index licensing fee. However, AMLP, MLPB, ENFR, and ALEFX are not issued, sponsored, endorsed or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing or trading of AMLP, MLPB, ENFR, and ALEFX.

For more news, information, and analysis, visit the Energy Infrastructure Content Hub.