State Street Investment Management (SSIM) is home to the lowest-cost S&P 500 ETF — the SPDR Portfolio S&P 500 ETF (SPYM) — and the largest gold ETF, SPDR Gold Shares (GLD ). Though these two ETFs have garnered the largest net inflows in October for SSIM, two other previously out-of-favor ETFs have also garnered significant interest. Before we take a closer look, I wanted to shout out SPYM, which is approaching the $100 billion asset mark. This is indeed impressive.

The Dow's Surprise October Haul

The SPDR Dow Jones Industrial Average ETF (DIA ) gathered $1.5 billion for the month of October (as of October 30). While DIA’s haul is not as impressive as the $6.3 billion and $2.5 billion gathered by SPYM and GLD, those funds have maintained investor favor for months. Even with the October cash haul, DIA has accumulated only $110 million of net inflows for the year. DIA’s performance in the past month has been more in line with the broader S&P 500 (3.1% vs. 3.9%), after lagging in the first nine months of the year. Year-to-date through October 30, DIA’s 13% gain was nearly 500 basis points behind SPYM.

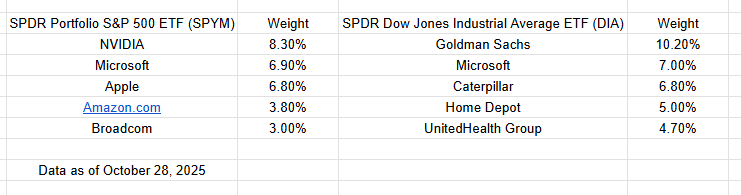

Relative to SPYM, DIA had more exposure to financials (27% of assets vs. 13%) and industrials (15% vs. 8.1%), while holding a smaller percentage in information technology (21% vs. 36%) and communications services (2.0% vs. 10%). Microsoft was among the top five positions in both ETFs, but DIA owned Caterpillar, Goldman Sachs, and Home Depot, and not Amazon.com, Apple, and NVIDIA, like SPYM. DIA is an ETF positioned to benefit from a rotation away from mega-cap growth stocks and into more economically sensitive value names.

Healthcare's Resurgence: A Look at XLV's Momentum

A separate rotation has benefited the healthcare sector. Recent performance earnings trends might help this trend’s persistence. The Health Care Select Sector SPDR Fund (XLV ) gathered $680 million thus far in October. Even with the strong recent flows, XLV had incurred net outflows of $1.6 billion for the year.

XLV was up 6% in the past month and, according to Christine Short, head of research at TMX Datalinx, strong recent third quarter earnings for the sector suggests this trend could persist. According to Short, healthcare has been led by exceptional strength in the pharmaceutical and hospital provider segments. Growth in pharma has been driven by high demand for blockbuster drugs, specifically GLP-1 weight loss drugs, while hospital providers have benefited from a rebound in patient volumes.

However, the results have been mixed for healthcare providers: While many reported strong revenue growth and even raised guidance, the companies also note they are facing significant profit pressure from medical cost inflation and rising utilization.

Healthcare represented 12% and 9% of DIA and SPYM assets, respectively. XLV is well diversified across industries, with pharmaceuticals (31% of assets) and healthcare equipment & supplies (23%) the largest, followed by healthcare providers (19%) and biotechnology (18%) all well represented. My colleague Cinthia Murphy recently looked at the holdings for the healthcare sector ETF.

Successful Blasts From the Past

DIA and XLV each launched in 1998, back when Bill Clinton was president and the ETF industry was significantly smaller. While SSIM has launched some exciting ETFs in 2025, in October investors returned to some of the classics. This recent flow suggests that investors are re-evaluating sector and factor exposures, potentially signaling a move toward value and defensive sectors that had lagged earlier in the year.

Author’s Note: I will be on CNBC’s ETF Edge November 3 at 1:10 pm talking about State Street Investment Management’s lineup and related ETF trends with Anna Paglia, the firm’s chief business officer.

For more news, information, and analysis, visit the ETF Strategist Content Hub.