Despite global geopolitical uncertainties and the ongoing conflict in the Middle East, the U.S. economy is showing signs of accelerating growth in the second quarter after a relatively soft start to the year. As often happens, stock market volatility is creating a lot of unease that masks the positive fundamentals. Legitimate concerns about stock market valuations are being stoked by unnerving headlines that ignore solid, and even improving, economic fundamentals. This can be a harsh reality in a mid-term election year, especially given the 24-hour news cycle, though we think that volatility creates opportunity for investors.

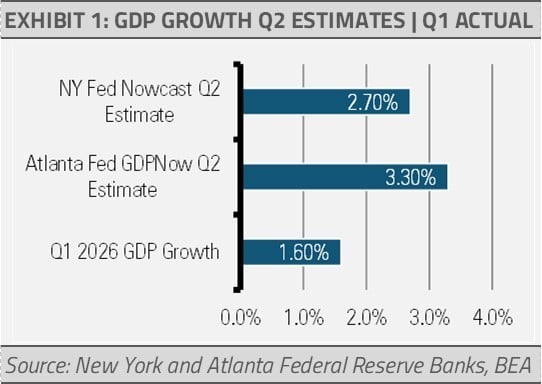

For example, forecasts for second quarter GDP growth reflect a resilient economy while headlines generate wide swings in stock markets. Federal Reserve Banks provide real-time tracking (nowcasts) for current quarter GDP growth, while the Bureau of Economic Analysis publishes official GDP statistics and revisions weeks and months after the quarter has ended. Two of the most prominent nowcast models, the New York Fed Staff Nowcast and the Atlanta Fed GDPNow, project second quarter growth at 2.7% and 3.3%, respectively, compared to 1.6% annualized growth in the first quarter.

The official GDP estimate for the second quarter will not be released until late July, so there is still time for data to drive further revisions before then. However, the information we can track now, especially related to the labor market, suggests solid growth in the current quarter.

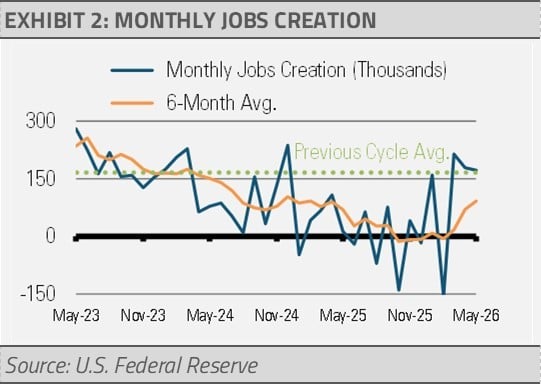

The strong employment report for June further supports our positive economic growth narrative. Following the February jobs losses, the months since have bounced back significantly (exhibit 2). Though the six-month moving average is still below the previous business cycle average, the recent uptick is moving in the right direction.

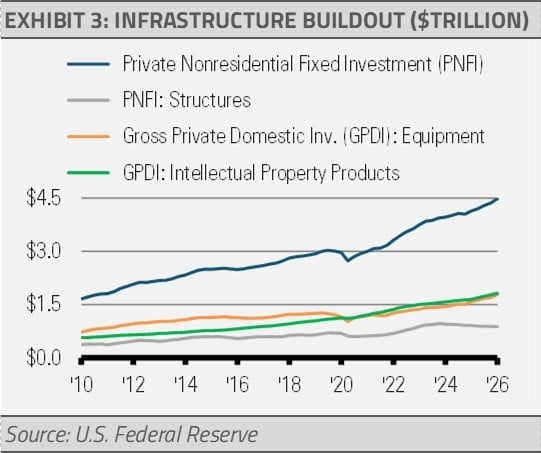

In addition, it is clear that the U.S. infrastructure buildout is having a significant impact on economic growth. Private fixed investment, which is the combination of structures, equipment, and research and development investments, has been growing for years.

Though projects in support of artificial intelligence (AI) have taken the lead, the increased investments in plant and equipment and related infrastructure began years before the AI research and development buildout went mainstream. Crucially, the investment in AI is no longer just a software narrative. This immense capital spending is filtering directly into the physical economy and driving significant revenue into industrial manufacturing, electrical equipment makers, and the energy grid infrastructure. These substantial capital investments should push long-term worker efficiency. Over time, these productivity gains can help support economic growth while naturally moderating broader inflationary pressures.

We expect these investments to have payoffs that will last for years into the future and are a primary reason we think that the next decade of U.S. economic growth will likely be stronger than anything we have seen since the 1990s.

INVESTMENT IMPLICATIONS

As a result, our Strategies remain tilted in favor of U.S. equities. At the sector level, we continue to emphasize financials (e.g., regional banks), industrials, and information technology. Within fixed income, we increased our exposure to mortgage-backed securities to capture attractive yields and a favorable risk/reward profile, while continuing to prefer the belly of the yield curve and high-quality asset-backed securities. With respect to our alternative investment allocations, we continue to favor equity option overlay strategies for current income and a multi-asset real return strategy for inflation mitigation and lower-correlation total returns. Our positioning is designed to be resilient across a range of geopolitical and energy-market outcomes. In our base case scenario, we consider volatility as an opportunity when selectively considering the current valuations.

THE CASH INDICATOR

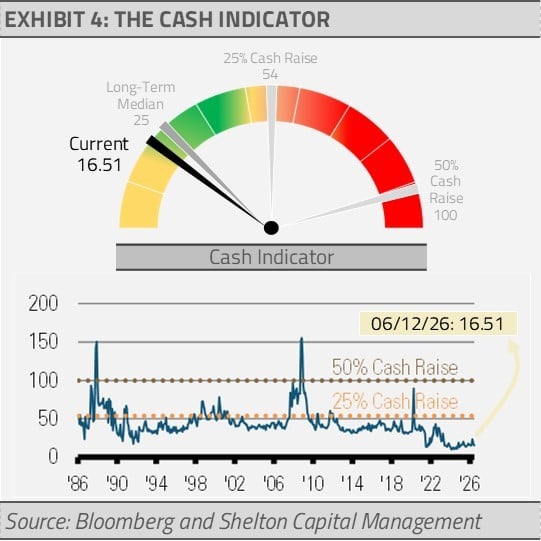

Our Cash Indicator (CI) has held steadily at levels below the long-term median all year, despite bouts of equity market volatility. The fixed income market has continued to reflect confidence in the economy and financial markets while keeping the CI relatively steady. Overall, the recent equity market volatility looks like a healthy reset back to “normal” levels of caution rather than a signal of trouble as we remain well below the point where the CI would call for moving to cash.

For more news, information, and analysis, visit the ETF Strategist Content Hub.

DISCLOSURES

Shelton Capital Management is an investment adviser in Denver, CO. Shelton Capital Management is registered with the Securities and Exchange Commission (SEC). Registration of an investment adviser does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. Shelton Capital Management only transacts business in states in which it is properly registered or is excluded or exempted from registration. Some of the firm’s strategies allocate client’s investment management assets among exchange-traded funds (“ETFs”). A GIPS Report along with a complete list and description of all composites is available by calling (800) 955-9988. A copy of Shelton Capital Management’s current written disclosure brochure filed with the SEC which discusses among other things, Shelton Capital Management’s business practices, services and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov. INVESTMENTS ARE NOT FDIC INSURED OR BANK GUARANTEED AND MAY LOSE VALUE. The views contained herein are not be taken as an advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted. The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Shelton Capital Management and has not been verified or audited by an independent accountant.