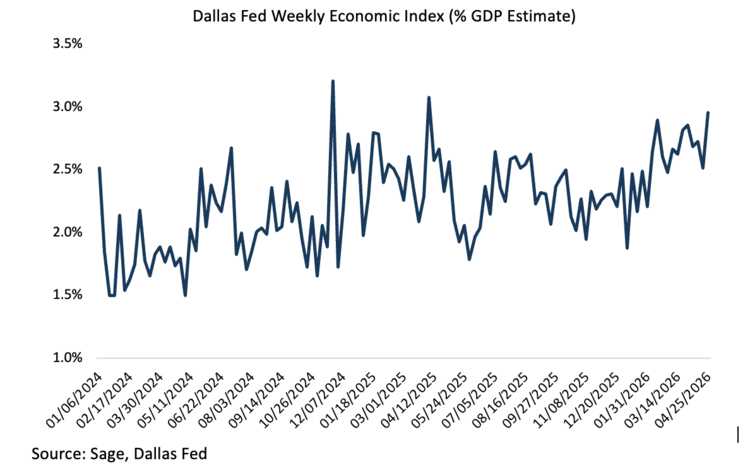

Market narratives remain split between two forces: tail risk to oil flows through the Strait of Hormuz and constructive US economic data supported by AI infrastructure capex. The Dallas Fed Weekly Economic Index (WEI), a real-time, GDP-equivalent signal of economic momentum, rose to 3.0% from 2.5% last week.

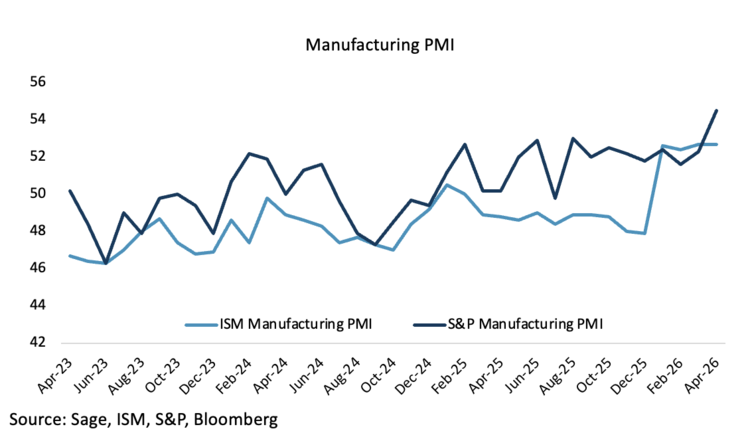

Manufacturing PMI surveys also signaled a continued manufacturing renaissance from AI infrastructure spending and reshoring, which could continue to boost both economic growth and productivity.

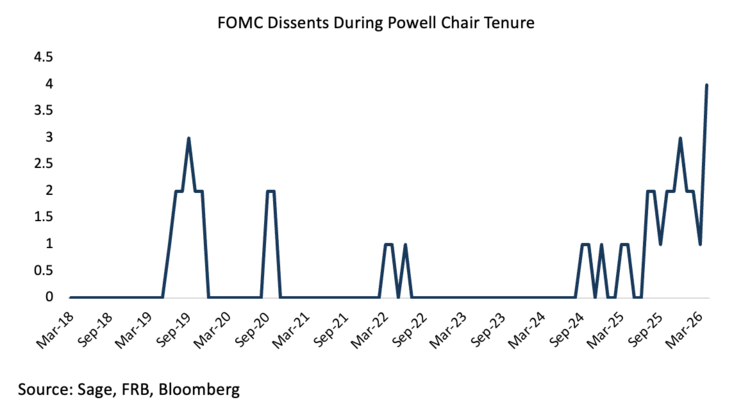

Stronger data, however, can bring its own risk. With energy-driven inflation pressure still a meaningful wildcard amid the Iran conflict, global central banks face a familiar dilemma. For the FOMC, that tension is heightened as the Fed navigates a leadership transition alongside a still-solid expansion.

When Powell took the helm as chair in early 2018, the Fed was in the midst of rate hikes after years of extraordinary accommodation, with inflation subdued and consensus-driven decision-making the norm. Today, inflation risks are more prominent and fiscal policy plays a larger role, with no end in sight to the fiscal deficit. Now, the Fed must contend with maintaining a solid economic expansion while mitigating inflation pressures. Interest rates should continue to remain rangebound at these levels as the Fed navigates competing objectives with less consensus than in past cycles.

For more news, information, and analysis, visit the ETF Strategist Content Hub.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our website at www.sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.