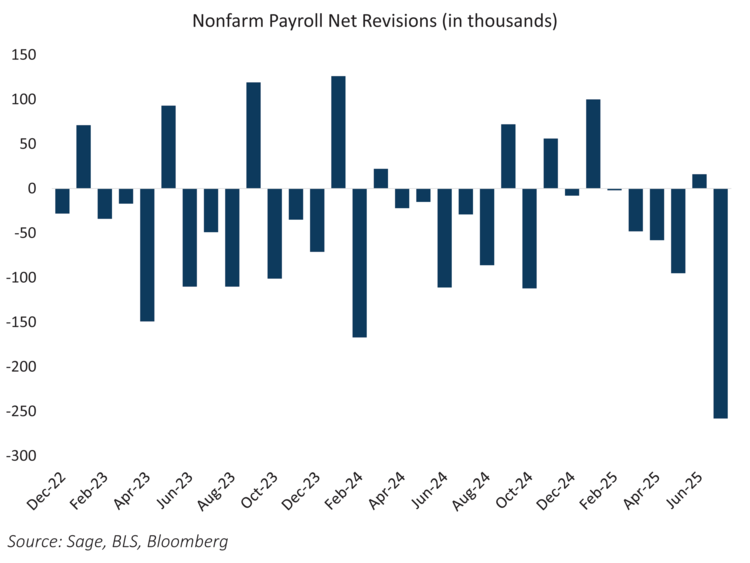

Last week’s payroll report delivered a sobering mix of disappointing data and significant downward revisions to the economic outlook. Nonfarm payrolls rose by just 76,000 in July, well below the consensus estimate of 110,000, while the unemployment rate ticked up to 4.2% from an expected 4.1%. While the headline miss drew attention, it was the revisions that had the greater impact: June’s figure was slashed to 14,000 from the originally reported 147,000, and every month in 2025 has now been revised downward.

Indeed, the July print saw revisions totaling 258,000, which is the largest negative revision since Covid. On Friday, President Trump fired the BLS chief after the outsized revisions. Whether it was politically motivated or not, nonfarm payroll numbers had been revised lower in 70% of the releases since 2022, which could point to a methodology issue.

Persistent downward revisions are not unprecedented, but they could signal inflection points in the business cycle. Periods such as late 2007 and mid-2001 saw similar patterns, where initial prints suggested stability, only to be followed by cumulative revisions that revealed a larger slowdown already in progress. This reflects the challenge of relying on real-time data — by the time the revisions are complete, the economy has often shifted meaningfully.

Historically, clusters of negative payroll revisions have coincided with an acceleration in the pace of policy easing. In 2001 and 2008, the revision trend influenced the Fed to acknowledge that labor conditions were deteriorating faster than expected, prompting larger and more rapid rate cuts. Even during softer mid-cycle slowdowns, such as in 1995 and 2019, sustained revisions acted as a catalyst for shifting policymaker expectations toward earlier accommodation.

At last week’s July FOMC Meeting, the Committee opted to leave rates unchanged, with two governors dissenting in favor of a cut — a level of Board-level dissent not seen since 1993. At the time, the labor markets appeared resilient and provided cover for patience. However, the latest jobs release and revisions undermine that premise and raise the possibility that policy is already behind the curve.

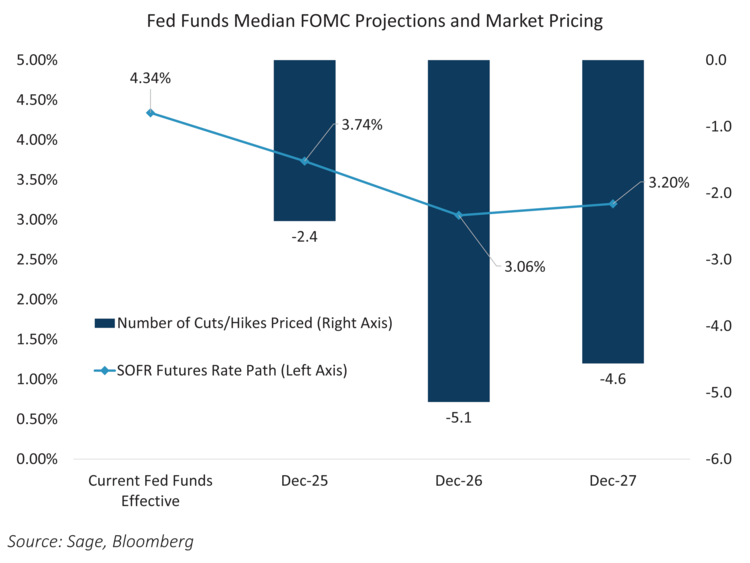

The rates market responded swiftly. Before the jobs data, pricing implied a more measured path of easing — just one full rate cut this year. Post-release, expectations shifted toward pricing in two full cuts in 2025 and five total cuts over the cycle. This still qualifies as a non-recessionary adjustment; a recession would presumably see multiple percentage-point reductions in the fed funds rate. The trajectory from here depends on whether the labor market is transitioning toward a slower-but-still-expanding economy or showing early signs of contraction. In both scenarios, the Fed cuts — in the first, to prolong the expansion with "insurance cuts;” in the second, more aggressively to offset recessionary pressures.

The distinction is critical for markets. Easing policy with unemployment below 4.5% has historically been supportive for risk assets, as seen in mid-cycle adjustments like 1995 and 2019. By contrast, easing into a recession — as in 2001 or 2008 — carries an entirely different risk-reward profile. For now, the bias for interest rates is lower, but the underlying cause will determine whether the adjustment is a tailwind or a warning for credit and equities.

Originally published August 4, 2025

For more news, information, and analysis, visit the ETF Strategist Content Hub.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy, or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis, and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our website at www.sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.