SUMMARY

- Rate moves on hold, as labor market stabilizes and the upside risk to inflation has

diminished.

- Leadership transition faces obstacles due to DOJ subpoenas.

- We believe the Fed will overcome challenges and maintain its credibility.

Chairmanship and Policy Change on the Horizon

The Federal Reserve (Fed) was established in 1913 to be the lender of last resort to the banking system. While the Fed’s original purpose still exists, it no longer has that singular focus. The Fed has had to adapt its role to fit the monetary landscape over the years, and it does not appear that 2026 will be any different. The Fed faces a number of challenges this year, including calibrating the appropriate policy rate, transitioning leadership, fighting a Department of Justice (DOJ) subpoena, and maintaining its independence. We believe that the Fed can overcome most, if not all, of these challenges, whether or not it receives cooperation from the executive, legislative, and judicial branches of government.

Fed On Hold as Labor Stabilizes and Inflation Risk Diminished

The Federal Reserve Reform Act of 1977 set forth the Fed’s dual mandate of ‘full employment’ and ‘price stability’. Last week, the Federal Open Market Committee (FOMC) met to set the appropriate interest rate policy to achieve its dual mandate. While the FOMC left the Fed funds rate unchanged at its January 28th meeting, committee members were not in complete agreement. Like the FOMC meeting in December, there were dissenting members that felt that the rate should be lower, calling for a 25-basis point cut. However, the vote was 10 to 2 in favor of holding rates steady, after cutting a total of 75 basis points over the prior 3 meetings. Fed officials pointed to stabilization of the unemployment rate as well as solid economic growth as reasons for holding interest rates steady. Chairman Powell stated that the Fed was appropriately positioned to manage the dual mandate, as the upside risks to inflation and the downside risks to labor have diminished.

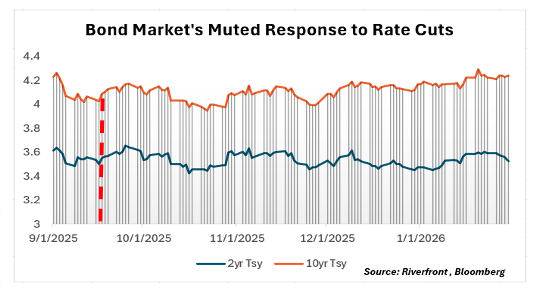

Currently, the target fed funds range is 3.50% to 3.75%, with the effective fed funds rate falling roughly in the middle of this range at 3.64%. However, despite the FOMC reducing rates since last September, the bond market has not reacted in a manner that would make a dramatic difference in the lives of consumers. For example, the chart on the page above shows that the 10-year Treasury yield (orange line) is higher now than it was when the FOMC made the first 25-basis point cut on September 17th (the dotted red line), thus keeping mortgage rates above the 6% mark. Even shorter maturity Treasuries like the 2-year are virtually unchanged over the period as well. This begs the question: why have yields not reacted more to Fed cuts? The short answer, as we explore in more detail below, is that the bond market does not believe inflation will moderate to the Fed’s 2% target anytime soon. We agree and remain underweight fixed income across our balanced portfolios as a result. The questions left on the minds of investors are: what data matters to the Fed, and what will it take to make it cut rates further?

We believe for the Fed to make additional cuts under a Powell-led FOMC, labor market deterioration would have to resume with the unemployment rising back up to 4.6% or higher from its current 4.4% level. Additionally, inflation would have to move closer towards the Fed’s 2% percent target.

Chairman Powell made the argument during his post meeting press conference that inflation is running just above 2% ex-tariffs. However, if this were truly the case, the bond market would reward investors with lower yields at the front-end of the yield curve represented by the 2-year Treasury, in our opinion, Chairman Powell insinuated that the embedded costs of tariffs are “transitory,” because economists calculate inflation on a year-over year basis. Hence, why members of the FOMC were willing to pre-emptively cut rates last year while its preferred gauge of inflation remained elevated at 2.8%. However, from consumers’ perspective, inflation is judged by the absolute dollar cost today versus the cost previously. For the time being, the bond market is voting with the consumer and not policymakers.

Fed Leadership Transition Sitting on a Tectonic Plate

Another challenge for the Fed is the upcoming leadership transition. Chairman Powell’s term as Fed Chairman is scheduled to end in May, and President Trump just announced Kevin Warsh as his successor on January 30th. According to reports, President Trump had narrowed his choices down to four candidates but chose a former Fed governor instead of picking an outsider. Under normal circumstances the transition would be routine, but this year it takes on a greater importance due to President Trump’s public disapproval of the Fed’s current monetary policy and the level of interest rates. Hence, the President sought to appoint a chairman that will be deemed credible to the financial community, while aligning with his thinking that interest rates need to be lower. The concern from market participants is that the next chairman will be beholden to the Trump administration’s wishes, lowering interest rates for political reasons rather than for the purpose of upholding the Fed’s dual mandate – a concern we discussed in the July 29, 2025 Weekly View.

Further complicating the leadership transition is the DOJ’s subpoenas to Chairman Powell regarding his congressional testimony on renovation cost overruns at two Fed buildings. This act was seen by some Democrats and Republicans in Washington as an escalation of political pressure that threatens the Fed’s independence. Republican Senator Thom Tillis has vowed to block all Fed nominations until there is resolution of the DOJ investigation. Technically, Powell could upset the apple cart further by deciding to serve out his full term as a Fed Governor, which expires in 2028 after his chairmanship ends. Not only would this be rare, but it would put additional pressure on his successor as chair to uphold monetary policy independence. We only give this outcome a 10% probability of occurring given that Powell believes in the traditions, culture, and collegiality of the Fed. We believe Powell will cede the spotlight to Kevin Warsh, if he is confirmed by the Senate, and make a graceful exit from the central bank.

Conclusion: We Expect Fed to Maintain Credibility; Remain Constructive on Stocks, Underweight Fixed Income

The Fed has done enough to maintain a solid economy, in our view, and now it must pause to see if the economic data supports its current monetary policy. As for the political and leadership headwinds, we believe the best-case scenario for markets would be the DOJ drops the investigation, the Senate confirms the new chair, and the President backs away from the public assault on the Fed, leaving Powell to stick with tradition and exit the central bank. This is the cooperation we alluded to earlier between the three branches of the government that could lower volatility in both the stock and bond markets and reinforce the Fed’s credibility, in our opinion.

However, even if the President continues to try and pressure the Fed into rate cuts, we believe FOMC members will respect the sanctity of the central bank’s independence and the creditability that it affords their decision-making process, regardless of their political affiliation. For this reason, if the Trump Administration nominates a chair-in-waiting to try to sway the thinking of members, there is no guarantee that their votes will subsequently align with the President’s wishes.

Also, as we discussed last week, we view Trump as a pragmatist who (eventually) is sensitive to market feedback. Investors view the Fed as an independent entity, and when the Fed’s status is perceived differently, bond buyers tend to push yields higher. Should the bond market become concerned regarding the level of rates, it will push rates up, increasing interest expense for government debt and pressuring the economy. We believe that this runs contrary to the Trump Administration’s aims, and they would likely find a politically palatable way to back off Fed pressure if it were perceived as a hinderance to yields falling and the economy expanding.

From a portfolio positioning perspective, we believe the Fed’s pre-emptive rate cutting has been fully priced into financial markets. Therefore, we are focused on the earnings growth potential a healthy economy affords companies. For this reason, we continue to tilt the portfolios towards sectors and industries such as technology, financials, and industrials that generate significant free cashflow. Currently, we prefer stocks over bonds, as the bond market is signaling that further rate cuts are not warranted.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Originally posted February 3, 2026

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

All charts shown for illustrative purposes only. Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

In general, the bond market is volatile, and fixed income securities carry interest rate risk. (As interest rates rise, bond prices usually fall, and vice versa). This effect is usually more pronounced for longer-term securities). Fixed income securities also carry inflation risk, liquidity risk, call risk and credit and default risks for both issuers and counterparties. Lower-quality fixed income securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer. Foreign investments involve greater risks than U.S. investments, and can decline significantly in response to adverse issuer, political, regulatory, market, and economic risks. Any fixed-income security sold or redeemed prior to maturity may be subject to loss.

Technology and Internet-related stocks, especially of smaller, less-seasoned companies, tend to be more volatile than the overall market.

Index Definitions:

A yield curve is a graphical representation of yields over time; it’s often depicted by plotting the yield of any given bond across different maturities in a given interval, perhaps by month.

A basis point is a unit that is equal to 1/100th of 1%, and is used to denote the change in a financial instrument. The basis point is commonly used for calculating changes in interest rates, equity indexes and the yield of a fixed-income security. (bps = 1/100th of 1%).

Definitions:

Inflation is a gradual loss of purchasing power, reflected in a broad rise in prices for goods and services over time.

Treasuries are government debt securities issued by the US Government. Treasury securities typically pay less interest than other securities in exchange for lower default or credit risk. With relatively low yields, income produced by Treasuries may be lower than the rate of inflation.

Federal Open Market Committee (FOMC) refers to the branch of the Federal Reserve System (FRS) that determines the direction of monetary policy in the United States by directing open market operations (OMOs). The committee is made up of 12 members, including seven members of the Board of Governors, the president of the Federal Reserve Bank of New York, and four of the remaining 11 Reserve Bank presidents who serve on a rotating basis.

The United States Department of Justice (DOJ) is an executive department of the United States federal government that oversees the domestic enforcement of federal laws and the administration of justice.

Interest rate sensitivity is a measure of how much the price of a fixed-income asset will fluctuate as a result of changes in the interest rate environment. Securities that are more sensitive have greater price fluctuations than those with less sensitivity. This type of sensitivity must be taken into account when selecting a bond or other fixed-income instrument the investor may sell in the secondary market. Interest rate sensitivity affects buying as well as selling.

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio. Asset class weighting discussion refers to our Advantage portfolios.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at riverfrontig.com and the Form ADV, Part 2A. Copyright ©2025 RiverFront Investment Group. All Rights Reserved. ID 5179905