Author: Kimberly Woody, Senior Portfolio Manager

Clarity and certitude are scarce. The only path to a soft landing is tame inflation and sound economic growth. For every measure of economic prosperity or recession there are multiple and equally persuasive countervailing scenarios. Arguably, the case should be made that much of the data upon which we rely remains distorted due to structural and monetary consequences stemming from the pandemic. The duration and magnitude have been extremely difficult for investors to predict or even understand, making our interpretation of what should be “normal” very challenging. You can see it in the frenetic volatility of interest rates and the breathtaking singularity of the Magnificent Seven’s outperformance.

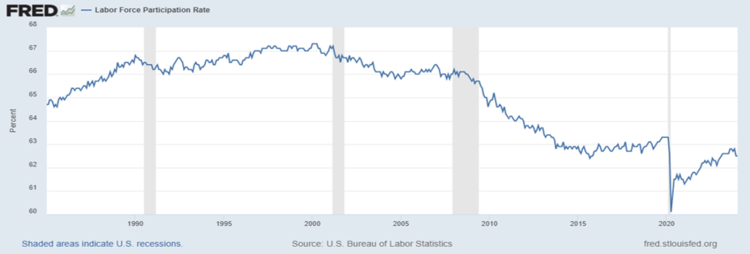

The latest round of employment data began with the Job Openings and Labor Turnover Survey (JOLTS) and showed that job openings are still plentiful at over 9 million but that quit rates are declining. The number of unemployed workers available per job is now at 0.7, which is consistent with the average of 0.8 in 2019, and on an upward trend from post-pandemic lows. These all suggest we might expect some moderation in wage inflation as jobs are becoming less plentiful and employees are less likely to job-hop for higher wages. Conversely, the most recent participation rate fell from 62.8 in August to 62.5, wage inflation ticked up to 4.5% after moderating since October 2023 and hours worked fell to 34.1 (see chart). While a number of labor market metrics have been deteriorating since summer, many metrics also confirm that the labor market remains tight.

Recession odds vary widely among economists. Some have reduced their odds of recession without eliminating the possibility, while some cling to it as a possibility but pushing it incrementally further out over the last 2 years. I am not suggesting strategists are typically great predictors of recession but in general they tend to move towards some semblance of consensus. We fail to find data that suggests the latter or even the former with conviction. The Institute for Supply Management’s measure of manufacturing activity, having contracted for the last 15 months, moved towards expansion territory last week. Confirming this was an uptick in overall job openings (JOLTS) with a noticeable uptick in manufacturing. Fourth quarter earnings were undeniably strong and point to a reacceleration in the US economy with 75% and 65% of S&P 500 companies reporting positive EPS and revenues surprises, respectively.

After months of moderation, inflation measures showed a slight uptick which may or may not signal a reversal in recent trends. Much like Chair Powell, we will need to see more readings to understand if this proves to be an anomaly. And even Powell is not currently moved to make any changes to monetary policy and commented “there is a wide disparity, a healthy disparity of views,” among FOMC committee members. But taken all together, macroeconomic data continues to come in better than expected. The US economy appears not only to be avoiding recession but perhaps re-accelerating, which spooks investors regarding inflation. Still, there is plenty of weak economic data in the US and especially abroad. Just last week as the producer price index reading ran hotter than expected, housing starts, and retail sales reversed course sharply.

Further muddying the picture is Washington’s continued profligate spending in relatively sanguine economic times. This means more spending, more and more debt issuance at high levels, and little left in the tank for truly countercyclical fiscal stimulus should the economy truly weaken. Not only is the Fed left seemingly bereft of ammunition but the still record high levels of M2 not only distort economic data readings but consumer and corporate behavior – the net of which we struggle to discern.

Uncertain times call for measured exposure. We believe it is imperative investors stay the course with regard to risk allocation, embrace diversification and most importantly resist chasing returns. Election year fears should not sway investment allocation or risk tolerance. As the lagged and variable effects of monetary policy begin to work their way through the economy, we will remain protective and vigilant. More to follow.

Sources: FactSet, Federal Reserve Bank of St. Louis, Institute for Supply Management, U.S. Bureau of Labor Statistics

GLOBALT has been registered with the SEC as an Investment Adviser since 1991. Effective October 1, 2023, GLOBALT is a limited liability company owned by the employees and succeeds the GLOBALT Investments business that was a separately identifiable division of Synovus Trust Co. GLOBALT is no longer affiliated with Synovus.

This information has been prepared for educational purposes only, as general information and should not be considered a solicitation for the purchase or sale of any security. This does not constitute legal or professional advice and is not tailored to the investment needs of any specific investor. Registration of an investment adviser does not imply any certain level of skill or training. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information may be required to make informed investment decisions, based on your individual investment objectives and suitability specifications. Investors should seek tailored advice and should understand that statements regarding future prospects of the financial market may not be realized, as past performance does not guarantee and/or is not indicative of future results. Content may not be reproduced, distributed, or transmitted in whole or in part by any means without written permission from GLOBALT. Regarding permission, as well as to receive a copy of GLOBALT’s Form ADV Part 2 and Part 3, contact GLOBALT’s Chief Compliance Officer, 3200 Windy Hill Road SE, Suite 1550E, Atlanta GA 30339. You can obtain more information about GLOBALT Investments and its advisers via the Internet at adviserinfo.sec.gov, sponsored by the U.S. Securities and Exchange Commission.

The opinions and some comments contained herein reflect the judgment of the author, as of the date noted.

For more news, information, and analysis, visit the ETF Strategist Channel.