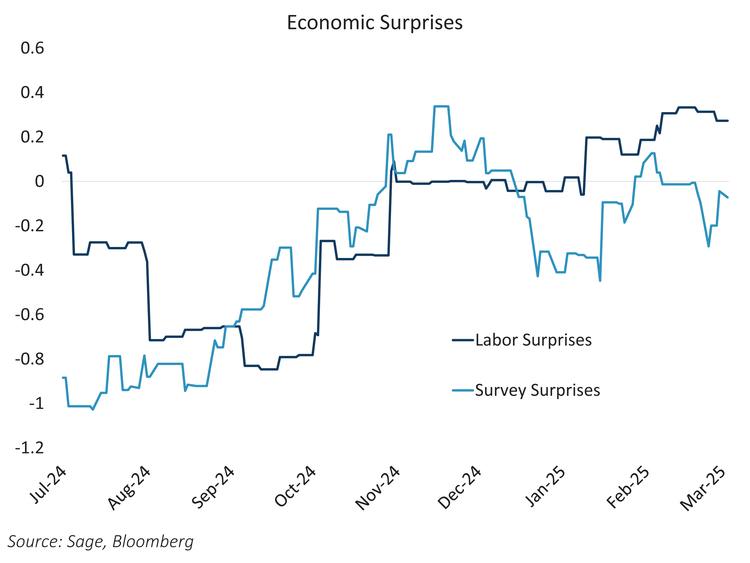

In recent weeks, markets have faced significant changes due to evolving economic data and the Trump Administration’s policies. After the November election, high fiscal deficits from tax cuts and tariffs raised concerns about inflation, pushing yields and term premiums higher. However, markets have since shifted their focus and are currently dominated by intense tariff negotiations, fiscal deficit control by Treasury Secretary Bessent, and federal job and spending cuts by the Department of Government Efficiency (DOGE). “Soft” economic data, such as survey data, reflect growing pessimism, while “hard” data, like labor statistics, remain resilient.

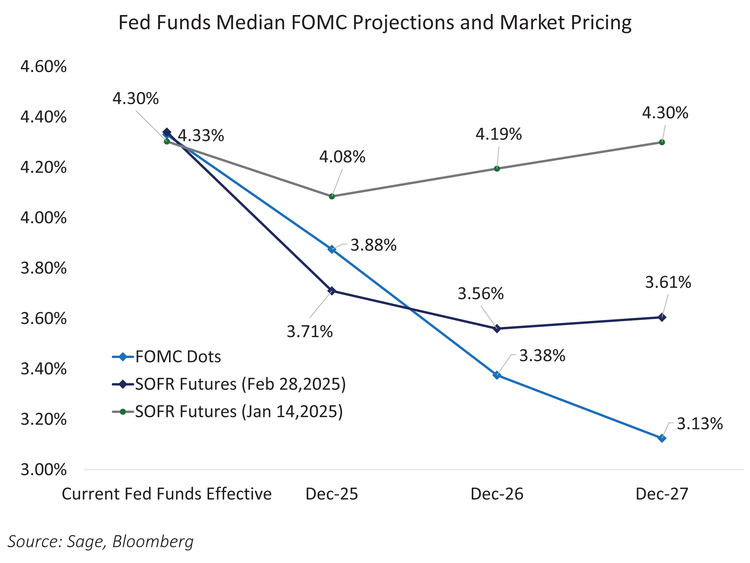

Bond yields have repriced since mid-January, shifting concerns from inflation to negative growth. The 10-year Treasury yield fell by 63 bps, and the 2-year yield dropped 43 bps, flattening the 2s10s curve by 20 bps. Fed pricing has shifted significantly, with expectations now including over two rate cuts this year and one next year.

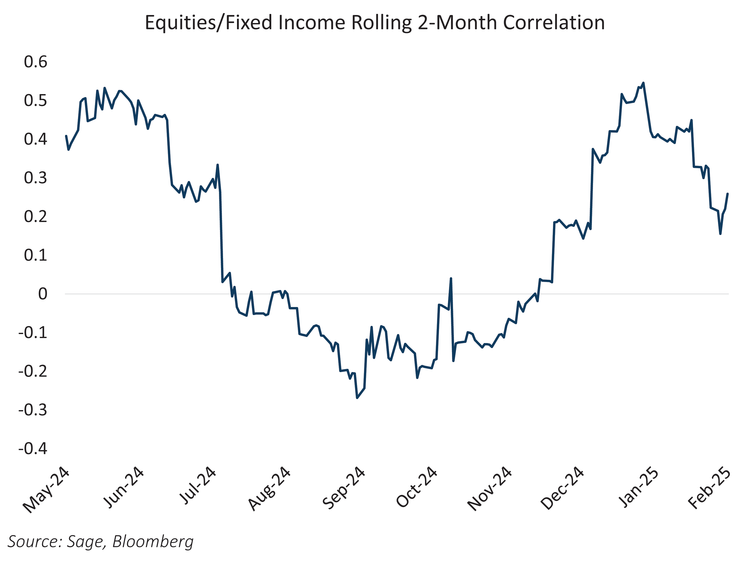

Interestingly, the correlation between stocks and bonds has shifted. During inflationary periods, both move in tandem due to the impact of higher interest rates on corporate profits and bond prices. In contrast, during periods of negative growth, stocks and bonds move inversely as investors seek the safety of bonds, driving their prices up and yields down while stock prices suffer.

The chart below shows the rolling 2-month daily return correlation of stocks versus bonds. The higher the number, the more that stocks and bonds move in tandem and vice versa. Since January 24th, stocks versus bond correlations have moved lower. If economic data continue to surprise to the downside, particularly regarding weakness in labor markets, the trend should continue as negative sentiment could morph into weakness in the real economy.

In recent weeks, expectations for a high fiscal deficit and “no landing” economic scenario have given way to fears of slowing growth compounded by the negative shocks from potential tariffs and federal job and spending cuts. Soft economic data, interest rates, and the correlation structure of stocks versus bonds signify the shift in tone. The extent to which this trend continues depends on whether real economic data, particularly concerning the resilient US labor market, start to disappoint to the downside.

For more news, information, and analysis, visit the ETF Strategist Channel.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.