By Rod Smyth, Vice Chairman

SUMMARY

- Low rates drove home prices above trend.

- Higher rates have not led to a housing slump…

- … Due to favorable supply demand conditions.

Working Off the Excesses…Still ‘Rusting’ not ‘Busting’

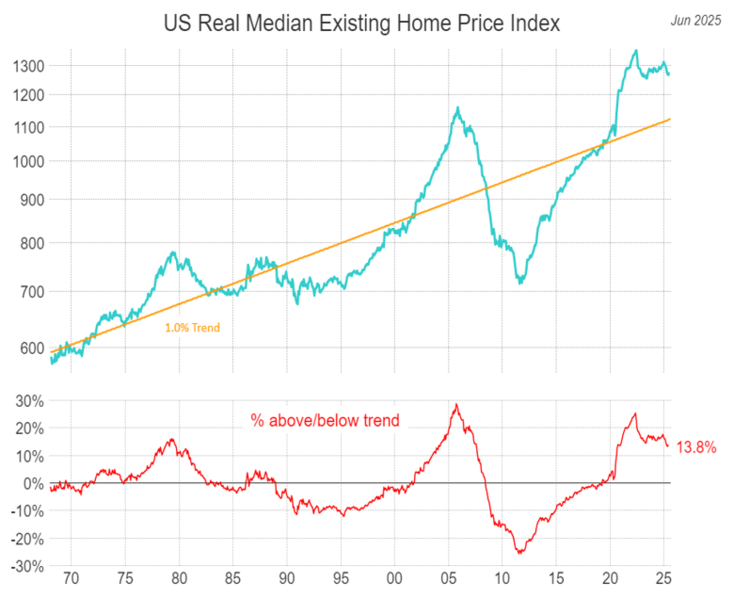

We last wrote about housing in May 2023. We made the case then that, although home prices were as far above trend as they were before the price collapse of 2007-2011, a big decline was unlikely. We wrote, “Our outlook is for prices to ‘rust’, i.e., go through a long period of stagnation, not ‘bust’ like they did in 2008/9”. That is still our view, and as you can see from the chart below, prices have generally been sideways since then.

Home Sales Have Fallen with Affordability

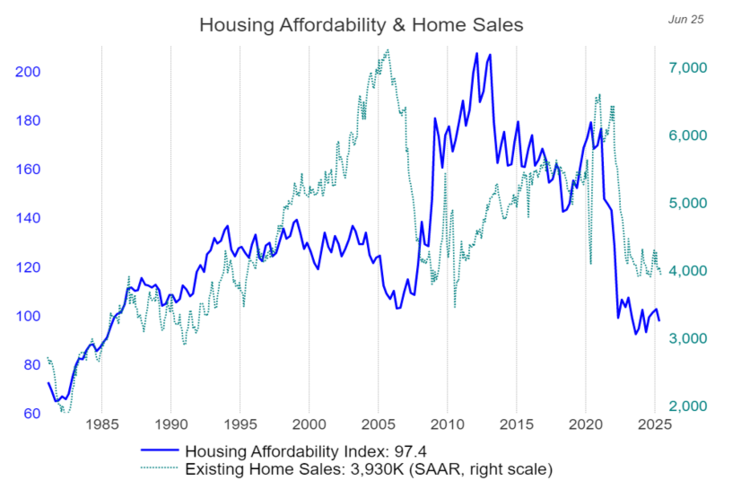

In some ways, the resilience in house prices is remarkable as mortgage rates have risen from 2.6% in 2021 to just under 6.6% today. The Housing Affordability Index (solid blue line in chart below) measures US income and interest rates to determine if a median-income family could qualify for a mortgage on a median-priced home. To interpret the indices, a value of 100 means that a family with the US median income has exactly enough to qualify for a traditional 30-year fixed-rate mortgage on a median-priced home. The higher the index in blue, the more affordable the median home is. This suggests homes are just ‘affordable’, but significantly less so than before the rise in rates in ‘21. We think this partially explains why home sales (dotted green line) have fallen. Another reason for falling sales is likely because homeowners who financed before the big rate rise are now ‘locked in’ to their low rates.

Rust not Bust: There is a Shortage of Supply

Having risen so far above trend, it is reasonable to ask if a sharp price decline, such as occurred during the 2008 to 2011 housing bust, is coming. In our view, if such a decline was going to happen, it would have been during the sharp rise in rates. Mitigating price declines in our view is a shortage of inventory, considerably less leverage and speculation than in prior bubbles, and household balance sheets that are normal by historical standards. Many homeowners refinanced their mortgages as rates fell to record low levels. This means they are unaffected by the rise in rates, as long as they don’t sell. Furthermore, according to Ned Davis Research, the number of months’ supply of existing homes is currently 4.5 months, above its’ all time low in 2022, but below the average of 6 and well below the 11 months seen during the housing crisis in 2008.

Demand is Supported by Demographics

The second structural factor that may lead to a ‘rust, not bust’ dynamic, is on the demand side; the ‘millennial’ generation are now in their household formation years. The oldest millennials are turning 44 and the youngest are turning 29. According to the US Census Bureau there are 74 million millennials, and they make up 22% of the US population as well as 35% of the workforce. Millennials are getting married later but household formation has picked up over the last five years, providing a source of structural demand.

When you combine these factors, the likelihood of a sustained period of house price stagnation seems high, but a collapse in house prices seems unlikely to us.

Some Final Advice on Buying a House Versus Renting

Buying a home is more than a pure financial decision. Unlike a stock portfolio which is purely an investment, you get to live in your house! This means there are all kinds of intangible emotional factors involved in buying a home. Since we all need somewhere to live, the choice is buying or renting and owning a home just feels different. Ownership involves maintenance costs, insurance and tax implications, but also allows you to add value to your home by improving it. The advantage of renting is flexibility, and a lack of repair costs… but rents are hard to predict and can rise rapidly. Generally, the longer you plan to live in a home, the more advantageous it is to buy.

Given our views on home prices, we suggest the decision be based on personal preferences, not on the expectation of further significant price increases in the next few years. As our chart on page one shows, home prices increase on a long-term trend basis of only roughly one percent over inflation and can have big price swings. This suggests that the main financial advantage of home ownership from current level is likely to be the ‘forced savings’ process of increasing your ownership stake by paying off a mortgage over time.

Originally published at Riverfront Investment Group

For more news, information, and analysis, visit the ETF Strategist Content Hub.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

All charts shown for illustrative purposes only. Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an

Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

Definitions:

The Housing Affordability Index measures whether a typical family earns enough income to qualify for a mortgage loan on a typical home. A value of 100 indicates that a family with the median income has exactly enough income to qualify for a mortgage on a median-priced home. This index is crucial for understanding housing market dynamics and the financial health of families in relation to homeownership.

Ned Davis Research (NDR) is a global provider of independent investment research, solutions and tools. Founded in 1980, NDR helps clients around the world make objective investment decisions.

Inflation is a gradual loss of purchasing power, reflected in a broad rise in prices for goods and services over time.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2025 RiverFront Investment Group. All Rights Reserved. ID 4752218