Few entities wield as much influence on the economy as the U.S. Federal Reserve (Fed). When the Fed embarks on an easing cycle and lowers its target interest rate, the ripple effects are felt across various sectors of the economy. This piece explores the nuanced impacts of such a cycle with a particular focus on mortgages, consumer credit, and cash investments.

Mortgage Market Dynamics

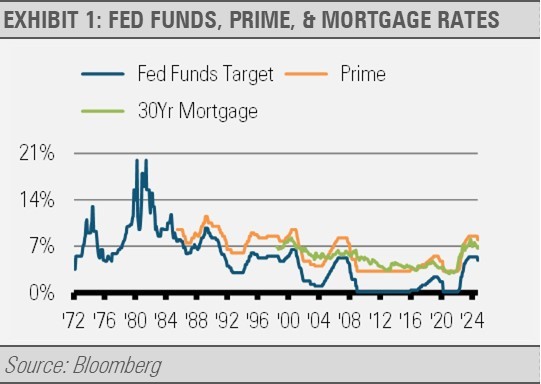

The mortgage market is significantly affected by Fed policy, albeit in varying degrees depending on the type of mortgage. Two primary categories dominate the landscape: adjustable-rate mortgages (ARMs) and fixed-rate mortgages (FRMs).

ARMs are generally more responsive to Fed rate cuts in the short term. These mortgages are typically benchmarked to shorter-term rates, which are more directly influenced by the Fed’s target rate. However, the impact on existing ARM holders can be delayed or muted due to several factors:

- Reset periods: Some ARMs may not adjust for several years after origination.

- Rate caps and floors: Many ARMs have built-in limits on how much rates can change, both per adjustment period and over the life of the loan.

These features can create a lag between Fed action and mortgage rate adjustment. Conversely, new ARM borrowers might see more immediate benefits as initial rates begin to reflect the lower Fed funds rate.

FRMs, or fixed-rate mortgages, march to a different drum. They are primarily impacted by the 10-year Treasury yield. These longer-term rates are more influenced by broader economic factors like economic growth expectations and inflation forecasts rather than short-term Fed policy. Consequently, FRM rates may not move in lockstep with Fed cuts, and borrowers might wait longer to see meaningful rate reductions.

It’s crucial to note that all mortgages carry a premium over their benchmark rate. This premium is influenced by various factors including risk perceptions and the supply and demand dynamics of mortgage-backed securities. Thus, even when benchmark rates fall, mortgage rates may not always follow suit proportionally or immediately.

Consumer Credit and Short-Term Borrowing

While mortgages show a complex response to Fed easing, other forms of consumer credit tend to be more directly reactive. Short-term borrowing vehicles, such as home equity lines of credit (HELOCs) and some auto loans, are often tied to the prime rate. This rate typically moves in close correlation with the federal funds rate.

Historical data shows that the prime rate often shadows Fed funds rate movements more closely than long-term mortgage rates. This means that consumers with prime-linked loans might see more immediate relief during an easing cycle. For instance, HELOC borrowers could experience lower monthly payments relatively quickly after Fed rate cuts.

Cash Investments and Short-Term Savings

For savers and conservative investors, a Fed easing cycle presents a different set of challenges. Cash and cash-equivalent investments, which have enjoyed higher yields in recent years, face downward pressure on returns during easing periods.

Money market funds and high-yield savings accounts are typically quick to reflect lower rates, often adjusting within days or weeks of a Fed cut. Certificate of Deposit (CD) holders might be temporarily insulated if they’re locked into a fixed rate, but upon renewal, they’ll likely face lower yields.

Short-term Treasury investors will also feel the impact as their securities mature and they are forced to reinvest at lower rates. This scenario underscores the importance of a diversified investment strategy that can weather various interest rate environments.

Broader Economic Implications

While the direct effects on borrowing and saving rates are significant, it’s important to consider the broader economic context of Fed easing cycles. These cycles are typically implemented to stimulate economic growth during periods of slowdown or in response to economic shocks.

Lower interest rates can encourage business investment, consumer spending, and overall economic activity. This can lead to job creation and wage growth, potentially offsetting the reduced yields for savers. Additionally, lower rates often support asset prices including stocks and real estate, which can benefit investors and homeowners.

However, prolonged periods of low interest rates can also have unintended consequences, such as inflating asset bubbles or encouraging excessive risk-taking in search of yield. This delicate balance highlights the challenging role the Fed plays in managing monetary policy.

A Fed easing cycle sets in motion a complex series of adjustments across financial markets. While some effects like lower rates on certain consumer loans, may be relatively straightforward, others, such as the impact on mortgage rates and long-term investments, are subject to a variety of influencing factors. As a result, individuals and businesses must remain vigilant and adaptable by understanding that the full impact of Fed policy changes often unfolds gradually and unevenly across different sectors of the economy.

For more news, information, and analysis, visit the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.