The Federal Reserve’s October 2024 Senior Loan Officer Opinion Survey (SLOOS) provides valuable insights into the current state of bank lending practices in the US. This quarterly report sheds light on changes in lending standards, loan terms, and demand across various sectors, reflecting broader economic conditions and credit availability trends. In recent years, the trends in the SLOOS survey have been dominated by tightening standards in response to the pandemic, inflation, rising interest rates, and regional bank stress. However, 2024 marks a subtle but noteworthy shift: standards, while still cautious, are tightening less aggressively compared to prior years.

Between 2020 and 2023, lending standards for both businesses and consumers tightened consistently. For commercial and industrial (C&I) loans, this tightening was especially stark, with small businesses hit hardest. The consumer side followed a similar pattern, with stricter requirements for mortgages and auto loans due to rising interest rates and concerns about credit risk.

By comparison, 2024 has seen banks moderating this trend. The share of banks reporting tighter standards has decreased from the highs of 2022 and early 2023. Although caution remains, particularly in sectors like small business lending, the pace of tightening has slowed.

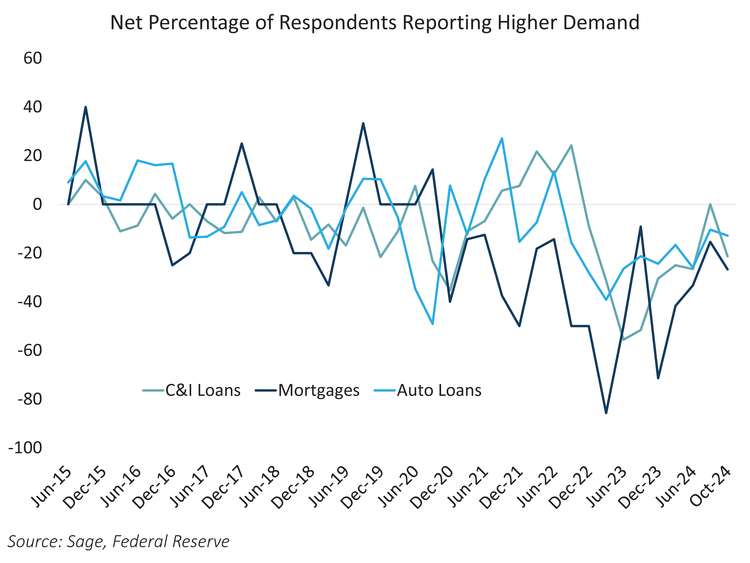

Even as standards have eased slightly in 2024, loan demand hasn’t bounced back in full force, although the fall in demand has eased throughout the year. The combination of high interest rates and economic uncertainty weighed on demand for business and consumer loans alike. Loan demand saw steep declines in 2022, particularly for mortgages and auto loans, but has recently begun to stabilize. What’s clear from the data is that while credit availability has improved somewhat this year, economic headwinds and/or concerns ahead of the elections were still holding borrowers back.

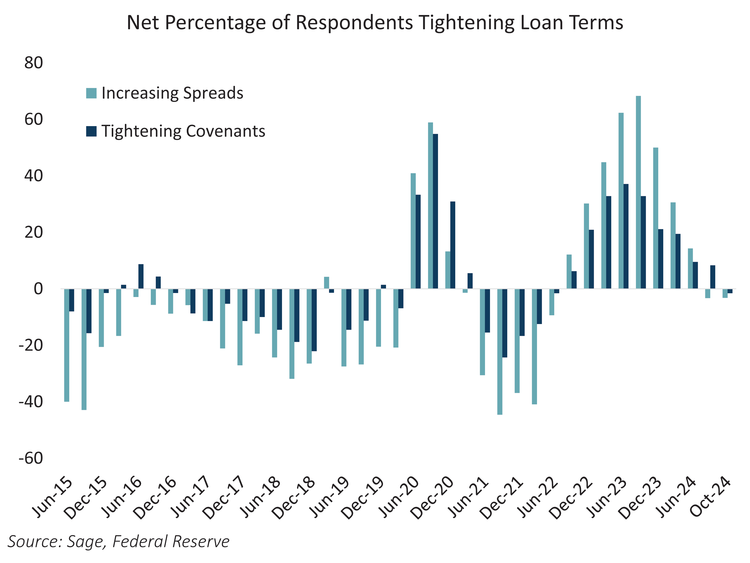

Despite slightly looser standards, many banks are still requiring higher spreads over funding costs and maintaining tighter covenants, although terms have started to loosen in recent months. Respondents are now reporting looser terms across spreads and covenants for the first time since 2022.

A Republican-controlled government should result in less regulation of the banking sector, potentially loosening rules and easing credit availability. Meanwhile, the broader economic picture remains robust. Key indicators like GDP growth, stable labor markets, and moderating inflation suggest that the US economy is on solid footing. While the lending data from the October 2024 SLOOS highlights a lingering sense of caution from borrowers, lenders are continuing to ease standards.

If the economy continues to expand at a healthy pace, the Fed continues to ease policy, and the federal government continues to run a large budget deficit and conduct pro-business policies, credit conditions could continue to ease, as illustrated by the nearly 30-year low for investment grade corporate spreads.

For more news, information, and analysis, visit the ETF Strategist Channel.

Disclosures

This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.