Summary

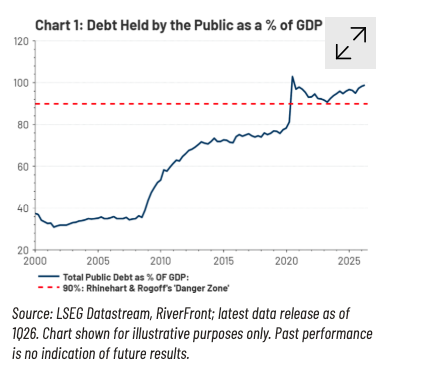

- US national debt held by the public now stands at around 100% of GDP — approaching post-WWII highs and well above the 90% threshold that academic research flags as a danger zone for growth.

- Despite these worrisome milestones, the US retains several important advantages that, in our view, make an imminent crisis unlikely — including economic dynamism, the dollar’s reserve currency status, and an enormous asset base.

- We identify three key warning lights to monitor: a spike in long-term interest rates, persistent elevated inflation, and a meaningful decline in the US dollar.

- History shows that large debt burdens can be reduced — the US itself did it after WWII through a combination of growth, fiscal discipline, and moderately higher inflation. We believe a similar multi-pronged approach, potentially supercharged by AI-driven productivity, represents the most plausible path forward.

- The time to start is now — not because a crisis is imminent, but because the longer we wait, the harder and more painful the adjustment becomes.

It’s now the dog days of summer… beautiful weather has returned, and most of the world is currently paying more attention to World Cup goals than fiscal goals. So today is a bit of a departure for us. Rather than focusing on actionable stock market matters, we want to step back and address a less tactical topic that we believe is crucial for the long-term health of American capital markets — and, frankly, for the country we love. After recently being asked to speak to the National Federalism Committee – a non-partisan government organization that advocates for a balanced relationship between the states and the federal government – on the worrying state of the national debt, we felt compelled to put our thoughts down on paper.

We want to be clear: we are not writing this piece because we believe a true debt crisis is imminent. We don’t. We are writing because we believe the current trajectory of debt accumulation is unsustainable and represents a key long-term challenge to some of the investment-related assumptions that underpin our portfolios.

Some Disturbing Milestones

The numbers are hard to ignore. The US has now accumulated over $31 trillion in total public debt, compared to roughly $31.8 trillion in GDP. That puts total publicly-held government debt at close to 100% of GDP — nearing the post-WWII high, and well above the 90%+ threshold that Harvard professors Carmen Reinhart and Kenneth Rogoff identified as a “danger zone” in their seminal research on historic debt calamities (Chart 1, above).

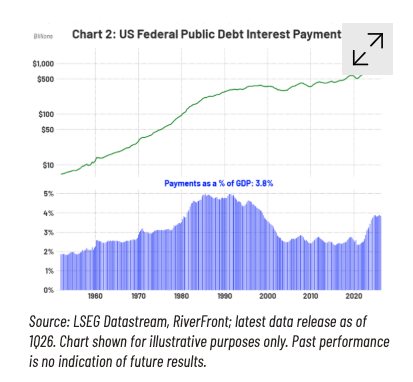

Perhaps even more striking is what this debt is costing us in real time. Federal interest payments have surged past $1 trillion annually — or roughly 3.8% of GDP. For the first time in modern history, the United States spends more servicing its past borrowing than it does defending our country. That comparison alone should give every American pause. Historian Niall Ferguson has documented what he calls ’Ferguson’s Law’ — that any great power which spends more on debt service than on defense risks ceasing to be a great power. History suggests we can still reverse course — but not indefinitely.

What Happens to Countries That Don't Control Their Debt?

The spectrum of historical outcomes concerning debt buildup is wide, and worth understanding. At the harshest extreme lies outright economic collapse, as in the case of Argentina. This South American nation has defaulted on its sovereign debt nine times, most recently in 2020; each time triggering devastating recessions, capital flight, and inflation that crushed the purchasing power of citizens. Greece’s debt crisis in 2010-2015 required massive external bailouts and imposed years of punishing austerity.

The more benign outcome — and, in our view, the more relevant one for the US — is less economic dynamism and slower future growth. Debt acts, in essence, like a turbocharger: it can pull potential future economic activity into the present. That can be enormously valuable during crises — as it was during COVID. But it comes at a cost, because borrowing robs future generations of growth they would otherwise have enjoyed. Economists call this ‘crowding out’ — the government’s borrowing competes with the private sector for capital, driving up rates and displacing the productive investment that powers long-term growth. In essence, the debt doesn’t just cost us interest — it costs us future prosperity.

Furthermore, high debt doesn’t just stunt future economic growth, but also increases the costs of funding that growth. Research from the IMF and the Federal Reserve consistently finds that higher debt levels have historically been associated with higher long-term interest rates — on the order of 3 to 4 basis points for every percentage point increase in the debt-to-GDP ratio. That may not sound like much, but for a country whose debt levels have spiked as meaningfully as ours have, that can compound into a significant drag over time on consumers, businesses and, ultimately, our republic.

Some Mitigating Circumstances for the US

It’s worth acknowledging that the United States is not Argentina or Greece. The US retains several important structural advantages that, in our view, make an imminent debt crisis unlikely.

Carrying costs are still manageable — for now. While interest payments have risen sharply, at 3.8% of GDP they remain within a reasonable range of historical experience (Chart 2, previous page). The US has operated at higher levels of relative interest expense before— notably in the 1980s and 1990s — without triggering a fiscal crisis. In fact, that time period is associated with strong US economic growth.

American ‘Economic Exceptionalism’ is real. The American economy remains the most dynamic, productive, and innovative large economy the planet, in our view. And we believe artificial intelligence (AI) is poised to extend that advantage. In our base case, RiverFront estimates that AI may boost US productivity by 0.5% to 1.0% over the next 5-7 years — a meaningful economic tailwind. Corporate profitability will likely benefit even more than that, as discussed in our recent Weekly View on "corporate cash flow.":https://www.riverfrontig.com/insights/the-ai-jobs-apocalypse-that-isnt/

A reflationary backdrop can actually help. This point is counterintuitive but important: ‘reflation’ – characterized by moderately higher-than-average growth and inflation— actually works in a debtor nation’s favor, because it erodes the real purchasing-power value of outstanding debt over time. This was a significant contributor to debt reduction after World War II, and it’s quietly working in the same direction today. As discussed in the Long-Term Capital Market Assumptions (CMA) section of our 2026 Outlook, RiverFront’s base case is that this current reflationary backdrop will generally persist over the next 5-to-7 years.

The US has extraordinary assets to offset its liabilities. Unlike smaller nations that have experienced debt crises, the United States controls some of the most valuable assets on the planet. Although it would be highly unlikely, if the US were ever obligated to post collateral for its loans, we believe there are plenty of assets it could pledge — prime land (including national parks), a vast portfolio of patents, digital spectrum usage rights, and enormous natural resource rights for energy and minerals. This makes an outright default — in the Argentine sense — exceedingly unlikely, in our view.

The US dollar remains the world’s reserve currency. This is perhaps the single greatest structural advantage. Because global trade and finance are denominated in dollars, the US enjoys a persistent demand for its debt that no other country can match. This doesn’t make deficits costless, but it does give the US significantly more room to maneuver than other countries in similar fiscal positions. This ‘reserve’ status is reinforced by the mechanics of global trade. So long as the US runs a large current account deficit, the corresponding capital account surplus compels foreign holders of dollars to recycle them into US financial assets — including Treasuries. This creates persistent structural demand for US government debt that has no parallel in countries like Argentina or Greece. This dynamic persists so long as the US remains one of the preferred destinations for global capital — a status we believe is durable but not a birthright, as we addressed here and one worth monitoring.

How to Monitor the Risks: Three Warning Lights

Rather than attempting to predict exactly if or when US debt becomes a crisis, we think investors are better served by monitoring three specific indicators that indicate significant probabilities of danger. When these warning lights begin to flash simultaneously, we believe it will be time to get genuinely worried about the federal debt.

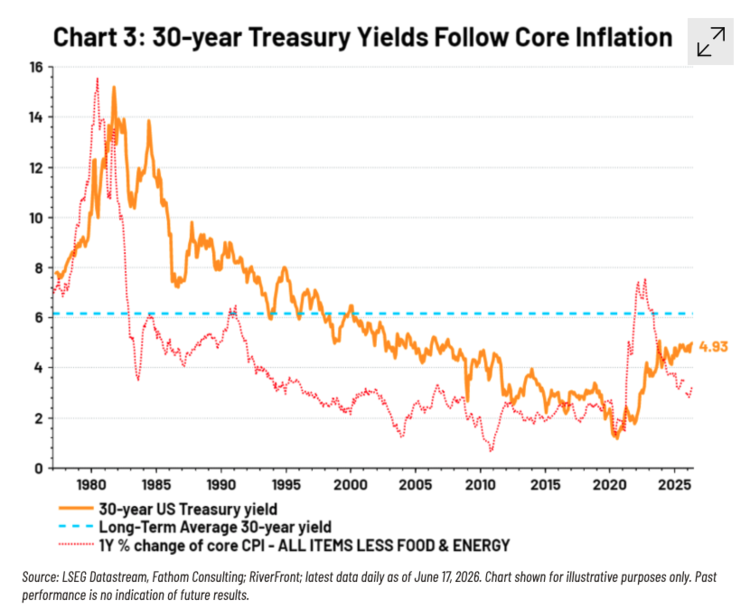

- Warning Light #1: If long-term interest rates spike to dangerous levels. While 30-year Treasury yields have risen considerably from their COVID-era lows (orange line on Chart 3, above), we would not characterize the move as a "spike” – the current level of roughly 5% is well within the range of historical average yields (blue dotted line). RiverFront expects fair value for long-term Treasuries to be in the 4.5%-5.5% range. A fast and sustained move above 6% – particularly if driven by term premium rather than growth expectations — would be of concern to us.

- Warning Light #2: Inflation spikes and stays there. After the 2008-2020 era of "financial repression” – extraordinarily low interest rates in the US and abroad — core inflation (i.e., ex-food and energy) returned with a vengeance in 2021-2023 due to COVID supply chain snafus. However, it has moderated meaningfully since (see red dotted line in chart 3) even after the advent of the Iran War in early 2026. A re-acceleration of core inflation back above 4 or 5%, sustained for multiple years, would signal that the debt burden is beginning to erode confidence in the government’s fiscal discipline. Such a confidence decline would likely trigger the rate spike we described above, as history suggests a high positive correlation between inflation trends and the level and direction of yields on US long bonds.

- Warning Light #3: The US dollar plunges. A sharp, sustained decline in the dollar — say, 15-20% against a broad basket of currencies over a short period — would signal that global investors are losing confidence in the US fiscal position. Importantly, a gradual weakening of the dollar is not, by itself, alarming; currencies fluctuate, and we think the dollar is likely still structurally overvalued after a decade-long bull market. What we would watch for is a disorderly decline accompanied by rising rates and capital outflows.

As of this writing, none of these three warning lights are flashing red yet, in our view. However, the upward move in rates and inflation bears continued monitoring. The last time we discussed this topic of the national debt back in 2020, interest rates were meaningfully lower, and core inflation was much closer to the Fed’s targeted 2% level. However, the USD in mid-2020 was at a similar level as today, demonstrating remarkable resilience.

How Could We Fix the Deficit? Some Suggestions from Either Side of the Aisle

Here’s where we want to shift to a more hopeful note — because the evidence strongly suggests that this problem is solvable with vision and political will. The US has done it before, and other countries have done it more recently.

The 40/40/20 Precedent – How the US Solved the Deficit After WWII: In 1946, US debt stood over 100% of GDP — a level strikingly similar to where we are today. Over the next three decades, that ratio fell to just 23%. How? Research from economists at Oxford, the IMF, and elsewhere decomposes the decline into three main forces: approximately 40% came from fiscal discipline (the government ran primary budget surpluses averaging 1.3% of GDP annually), approximately 40% came from robust economic growth (real GDP grew at 3.5%+ per year, powered by the baby boom, the GI Bill, and massive infrastructure investment), and approximately 20% came from “financial repression” — keeping interest rates below the rate of inflation, which quietly eroded the real value of the debt. In the ‘reflationary’ backdrop we are predicting for the foreseeable future, nominal economic growth and inflation

AI as a modern growth accelerator. We believe AI-driven productivity growth has the potential to serve as a powerful tailwind in a modern version of this three-legged stool described above. RiverFront’s base case view on AI mentioned earlier–is that AI-led productivity gains could represent one of the most significant productivity boosts in the post-war era.

The Canada model proves it can be done in the modern era. In the early 1990s, Canada was in dire fiscal straits — the Wall Street Journal called it “an honorary member of the Third World.” Then, starting in 1995, Canada launched sweeping reforms, more focused more on cutting spending than increasing taxes; spending cuts outweighed tax increases by a ratio of roughly seven to one. Canada achieved a budget surplus by 1997 and ran eleven consecutive surpluses thereafter, reducing its debt-to-GDP ratio by 35 percentage points in a single decade without causing a recession. It wasn’t painless — but it worked, and it happened in a country with a culture and economy similar to our own.

Concrete policy frameworks already exist. Warren Buffett once quipped that he could "end the deficit in five minutes” – just pass a law making all members of Congress ineligible for reelection whenever the deficit exceeds 3% of GDP. He was joking, of course, but the underlying point is serious: the incentive structures need to change.

More practically, the Committee for a Responsible Federal Budget (CRFB) has proposed a detailed framework that includes committing to a principle of “No New Borrowing,” adopting a 3% of GDP deficit target, implementing “Super PAYGO” rules that require any new spending or tax cuts to be offset by twice the amount in savings, addressing trust fund solvency before insolvency, and establishing a pre-negotiated “Break Glass Plan” for fiscal emergencies. None of these ideas are that ideologically radical, and could theoretically be embraced in a bipartisan way.

Perhaps most encouraging, in 2024 the Peterson Foundation’s Solutions Initiative commissioned plans from seven think tanks spanning the political spectrum — from the Economic Policy Institute on the left to the Manhattan Institute on the right — and every plan suggests the potential to reduce debt-to-GDP ratio by at least one-third over 30 years by using a combination of spending cuts and revenue increases. The disagreements are about which levers to pull — not whether workable levers exist.

Conclusion: The Time to Act Is Now

We want to end where we began: we do not believe an imminent debt crisis is likely for the United States. The economy is too dynamic, the dollar too entrenched, and the asset base too formidable for the kind of sudden unraveling that has afflicted other debt crisis nations.

But “not imminent” is not the same as “not important.” The CBO projects that under current law, debt-to-GDP will reach 175% by 2056. Every year of delay makes the eventual adjustment larger, more disruptive, and more painful. The interest expense alone will crowd out an ever-growing share of discretionary spending, reducing the government’s ability to invest in the future or respond to the next crisis.

The good news is that history tells us this is a solvable problem. The US did it after WWII. Canada did it in the 1990s. Seven ideologically diverse think tanks have all created credible ways to meaningfully decrease the deficit from today’s starting point. And AI-driven productivity growth may provide a tailwind that previous generations didn’t have.

What’s required is not economic genius — it’s political courage. And for those of us who care deeply about the long-term trajectory of this country and its markets, we believe it’s worth saying so — clearly, directly, and with the urgency the moment demands. Not because the house is on fire, but because the best time to fix the roof is while the sun is still shining.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

For more news, information, and analysis, visit the ETF Strategist Content Hub.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

The comments above are subject to change and are not intended as investment recommendations. There is no representation that an investor will or is likely to achieve positive returns, avoid losses or experience returns as discussed for various market classes.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

All charts shown for illustrative purposes only. Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

In general, the bond market is volatile, and fixed income securities carry interest rate risk. (As interest rates rise, bond prices usually fall, and vice versa). This effect is usually more pronounced for longer-term securities). Fixed income securities also carry inflation risk, liquidity risk, call risk and credit and default risks for both issuers and counterparties. Lower-quality fixed income securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer. Foreign investments involve greater risks than U.S. investments, and can decline significantly in response to adverse issuer, political, regulatory, market, and economic risks. Any fixed-income security sold or redeemed prior to maturity may be subject to loss.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Technology and internet-related stocks, especially of smaller, less-seasoned companies, tend to be more volatile than the overall market.

Artificial intelligence, or AI, refers to the simulation of human intelligence by software-coded heuristics. Nowadays this code is prevalent in everything from cloudbased, enterprise applications to consumer apps and even embedded firmware.

Definitions:

Gross domestic product (GDP) is a monetary measure of the market value of all final goods and services produced in a period (quarterly or yearly) of time.

Inflation is a gradual loss of purchasing power, reflected in a broad rise in prices for goods and services over time.

A recession is a significant, widespread, and prolonged downturn in economic activity. A common rule of thumb is that two consecutive quarters of negative gross domestic product (GDP) growth indicate a recession. However, more complex formulas are also used to determine recessions.

Reflation is a policy response to economic slowdowns that aims to boost spending and counter deflation. It can involve tax cuts, lower interest rates, expanding the money supply, or increased infrastructure spending, all meant to jump-start activity after a contraction. As the early phase of recovery, reflation helps move an economy from stagnation back toward growth.

Treasuries are government debt securities issued by the US Government. Treasury securities typically pay less interest than other securities in exchange for lower default or credit risk. With relatively low yields, income produced by Treasuries may be lower than the rate of inflation.

A basis point is a unit that is equal to 1/100th of 1%, and is used to denote the change in a financial instrument. The basis point is commonly used for calculating changes in interest rates, equity indexes and the yield of a fixed-income security. (bps = 1/100th of 1%)

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at riverfrontig.com and the Form ADV, Part 2A and/or Form CRS. Copyright ©2026 RiverFront Investment Group. All Rights Reserved. [ID 5627998]