Theoretically, the two foundational drivers of long‑run economic growth are population growth, which expands the labor force, and productivity, which determines how efficiently that labor can transform inputs into outputs. Despite recent trends pointing to a shrinking or slow‑growing workforce across the US economy, signs are emerging that productivity is beginning to firm — supported in part by post‑pandemic restructuring and the early impacts of AI‑enabled investment. If these productivity gains prove durable, they could help offset demographic headwinds and extend the economic expansion in ways that challenge the more pessimistic narratives surrounding the post‑COVID, AI‑era economy.

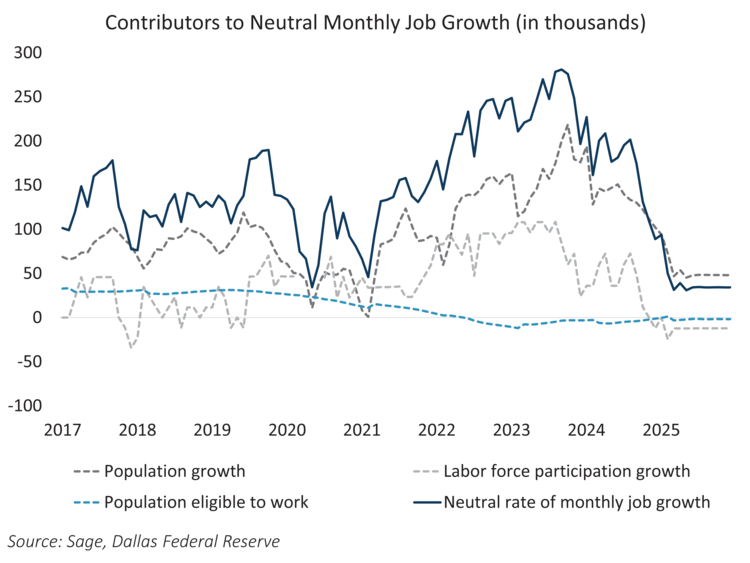

Labor force growth has slowed meaningfully in recent periods. According to the Dallas Fed, the breakeven pace of job creation — the monthly gain required to keep the labor market in equilibrium — is determined by three elements: overall population growth, the share of the population eligible to work, and the labor force participation rate. Their latest estimate puts this neutral job‑growth threshold at just 34,000 per month, a steep decline from more than 280,000 in 2023. With the pool of available workers temporarily constrained, sustained economic expansion increasingly depends on productivity stepping up to fill the gap.

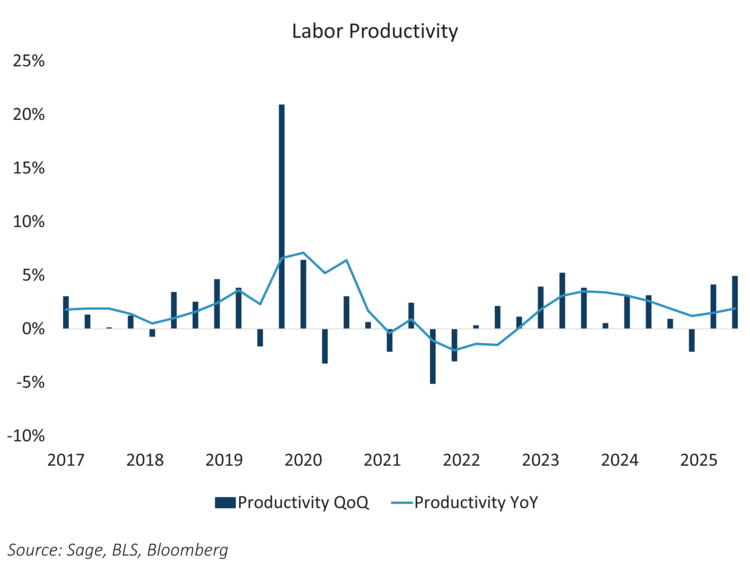

The most recent US productivity release showed a marked increase in productivity, with output per hour growing by 4.9% in 3Q 2025, after a similarly strong 2Q, while unit labor costs declined over those same two quarters.

At a time when the workforce is shrinking and the labor market appears stuck in a “no hire, no fire” stagnation, this rebound in productivity takes on increased importance. If sustained, it could provide the necessary engine to extend the current economic expansion even in the absence of meaningful labor force growth — helping the economy do more with less, and potentially easing concerns about stagnation in a structurally tighter labor market.

Higher output per worker, coupled with easing labor costs, supports corporate margins at a time when the labor market is no longer a growth engine. That combination strengthens corporate fundamentals, tempers default risk, and should help maintain tight credit spreads, particularly for issuers with the flexibility to capture AI‑enabled efficiency gains.

From a rates perspective, stronger real growth with less inflation pressure reduces the urgency for aggressive Fed easing and on balance should keep yields elevated. The result is a backdrop where the cyclical lift from stronger productivity must be weighed against downside risks from a softening labor market and ongoing geopolitical shocks, a balance that should keep yields largely stable at these levels. This reinforces the notion that income — rather than price appreciation — is the primary driver of total return for bonds this year.

Originally published January 12, 2026

For more news, information, and analysis, visit the ETF Strategist Content Hub.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our website at www.sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.