We have recently experienced market volatility and obvious signs of rotation among stock market sectors. Currently, most of the damage to the stock market seems to be concentrated within software business. For example, semiconductor stocks are still doing well along with the information technology sector. Still, other areas of the U.S. stock market are participating better, such as the health care and industrials sectors. Most importantly for our outlook, the underlying economy appears to be blossoming. This is vastly different from the backdrop we saw at the end of the Tech Bubble going from the late 1990s to the early 2000s. At that time, we also saw elevated equity market valuations, but the U.S. Federal Reserve (Fed) was raising interest rates and the economy eventually slipped into recession, taking the stock market down with it.

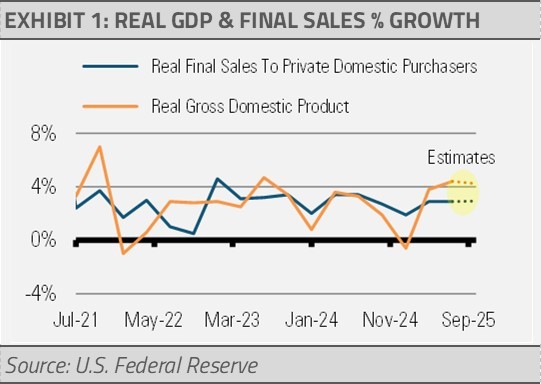

In contrast, this time the Fed has been cutting interest rates due to softening inflationary pressures and slower employment gains. Meanwhile, economic activity continues to grow at a strong pace and ended 2025 with a 4% growth rate over the last half of the year. We expect economic growth in the year ahead as Fed policy normalizes and the private sector continues to drive economic activity.

When it comes to tracking overall U.S. economic growth, we prefer to look at real final sales to private domestic purchasers because it gets to the heart of the U.S. economy, the private sector, by excluding the effects of net trade, inventories, and government spending. As a result, this data series provides a clearer picture of true economic strength. It is also significantly less volatile, which helps better gauge the actual health of the U.S. economy by cutting out the noise from those other factors. As the following graph indicates, while much discussion has been made of the swings in the pace of GDP growth, real final sales to private domestic purchasers has continued to consistently chug along with little fanfare, reflecting the quiet strength of the U.S. economy.

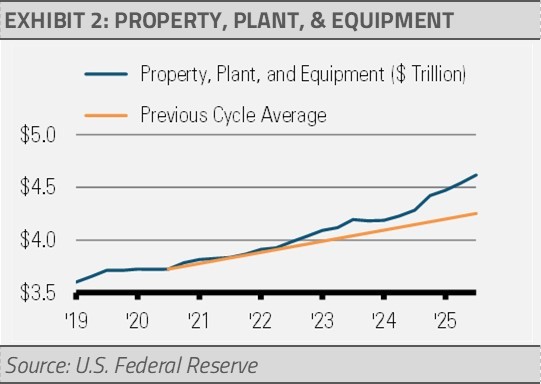

We see further confidence displayed by U.S. corporations’ increasing investments in property, plant, and equipment. These kinds of investment should lead to greater levels of industrial production over time. While it can take years for new manufacturing facilities to come online and for new equipment to increase productivity, the end result should be solid economic growth ahead.

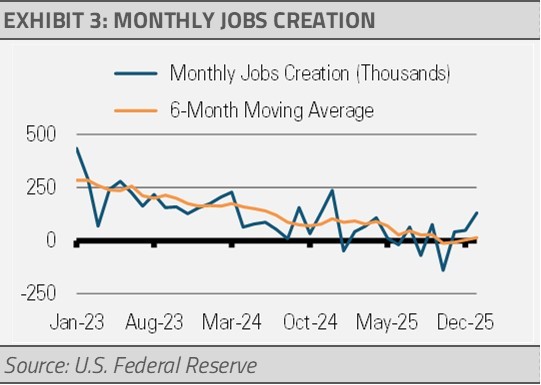

We are also optimistic about the labor market. We prefer to monitor jobs creation through a 6-month moving average in order to smooth out the month-to-month volatility, and we are seeing positive signals in both the monthly numbers and the 6-month average. The jobs market was challenged last year by uncertainty due to changing trade policies and the significant reduction in the federal workforce.

Employment growth slowed further following the April 2025 tariff announcement, but it seems to have bottomed out in October as the bulk of the federal government layoffs hit the statistics. With both of those headwinds mostly in the rearview mirror, we expect to see more persistent jobs growth. The healthcare sector has recently been leading employment gains, and we expect that to continue with strong demand for qualified and highly paid workers. Overall, we think that on average jobs creation will approximate the labor force growth rate of roughly 100,000 new entrants per month going forward. We note that this pace of hiring is still slower than the previous business cycle average and reflects the realities of today’s slower labor force growth.

Risks do remain, of course. For example, we expect to see more muted overall economic growth that, combined with stabilizing inflationary pressures, should help keep the Fed in a more accommodative stance. Yet, slow growth is still growth, meaning that the total number of employed people should continue to increase, as will income, investment, and spending. Robust growth in the business sector combined with persistent growth in the household sector should propel overall economic activity.

INVESTMENT IMPLICATIONS

The recent broadening of equity market participation toward other countries and industries outside of the Magnificent 7 is a pleasant change. While we think that the businesses that led the initial stock market gains will continue to be important, other sectors, such as industrials and healthcare, are now participating in a more meaningful way. We continue to be overweight equities and favor the previously mentioned sectors as well as small caps and financials. Regarding fixed income, we see the best opportunities in the belly of the yield curve and prefer asset backed securities for both their quality and attractive yields. Our alternative asset allocations are focused on options overlay equity strategies along with a real return multi-asset strategy.

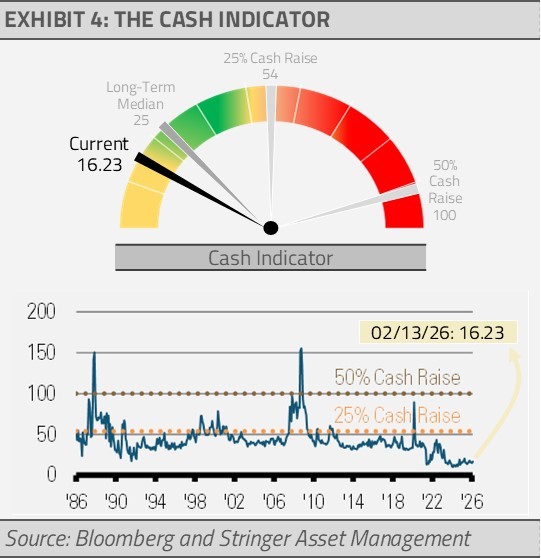

THE CASH INDICATOR

The Cash Indicator (CI) has been relatively stable, even as equity market volatility has increased. Bond market confidence has acted as an important stabilizer. Overall, we see the current CI level as reflecting a healthy amount of investor skepticism.

For more news, information, and analysis, visit the ETF Strategist Content Hub.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are solely the authors as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not be taken as an advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted. The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Shelton Capital Management and has not been verified or audited by an independent accountant.