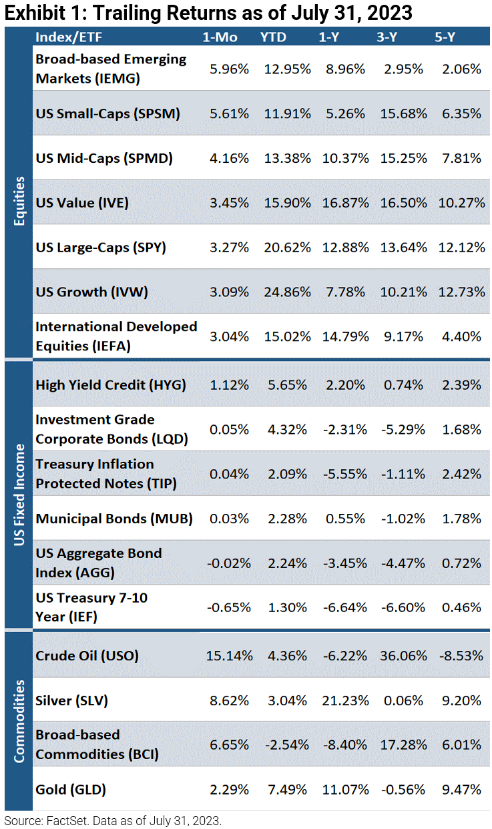

Major Indices Rise for Fifth Straight Month

As of July’s end, both the S&P 500 Index and Nasdaq Composite Index posted their fifth consecutive monthly gain. The positive equity performance for the month comes on the back of cooling inflation, better than expected earnings, and increased probabilities of a soft landing. Broad-based emerging market equities (+ 6.0%) were among the best performers, followed by US small-caps (+ 5.6%) and US mid-caps (+4.2%). Bonds were mixed as high yield credits rose 1.1% while 7-10 year US Treasuries fell 0.7%. Commodities produced positive returns as crude oil was up 15.1%, silver increased 8.6%, broad-based commodities gained 6.7%, and gold rose 2.3%.

Fed's Hike in July May be its Last

The Federal Reserve raised interest rates by 25 bps at the July FOMC meeting, causing the fed funds rate to increase to the 5.25–5.50% range, its highest level in more than 22 years. Despite notable softening in headline inflation measures, the hike comes after a skip at the previous meeting as core annualized CPI and PCE for June remain at more than double the 2% target (4.8% and 4.1%, respectively). Though policymakers previously expressed two more 25 bps rate hikes for the year at the June meeting, the bond market is currently pricing no additional hikes in 2023. Fed Chairman Jerome Powell left the door open for additional tightening dependent on incoming data, and indicated that future interest rate decisions will be made on a live meeting by meeting basis. Given the resilience of the economy, he signaled there may be a chance for inflation to return to its target without heavy job losses, but there is “a lot left to go to” before a soft landing may be achieved. Moreover, the central bank’s staff is no longer forecasting a recession, but still sees “a noticeable slowdown in growth starting later this year.”

Consumer Confidence Hits Two-Year High

The Conference Board Consumer Confidence Index measures consumer views on current and short-term business and labor conditions. Despite the Fed continuing to raise interest rates to curb demand and reduce inflation, the index recently notched its highest print in two years. Could an unusually healthy consumer force the Fed to continue tightening?

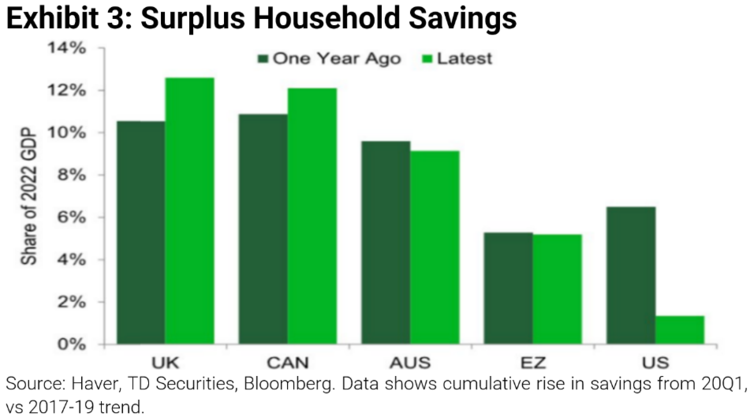

Will the US Consumer Soon "Tap Out"?

Consumer health has largely garnered support from households’ excess savings left over from the wake of the COVID-19 pandemic. This support could fade soon as recent data shows that American households are burning through their excess savings at a much faster pace than their rest-of-world (ROW) counterparts.

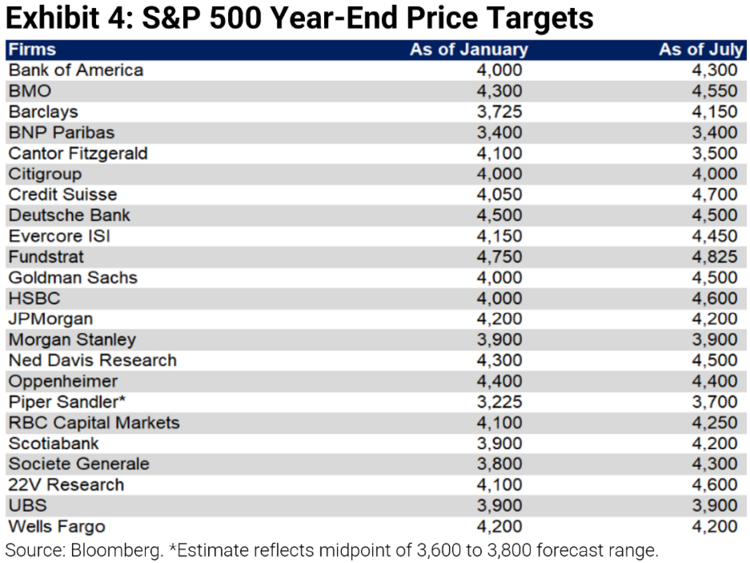

Revised Predictions Still Signal Contraction

Even though most Wall Street firms have revised their projections for 2023-end S&P 500 levels upwards, most of them are still expecting a contraction in 2H 2023. The index closed at 4,588.96 on July 31st, and only 4 of the 23 firms surveyed expect that number to increase by the conclusion of 2023. However, the S&P 500 is currently above most year-end predictions made as of January. Will these firms have a better idea this time around?

Soft Landing Probabilities have Increased, but Recession Risks Persist

The market’s performance has drawn investor sentiment to levels above historical averages. For instance, according to the AAII Investor Sentiment Survey, bullish sentiment has been above its historical mean for eight consecutive weeks. Additionally, the labor market remains historically tight and continues to be one of the primary sources of strength for consumer spending. Recent economic data has seemingly been net positive for investors anticipating a soft landing, and at the very least, the recession has been kicked down the road. However, we continue to emphasize that we are far from out of the woods. Consumer health has been driving the economy since the pandemic, which is problematic as some indicators are beginning to show signs of deterioration. For instance, Redbook Retail Sales have declined for three straight weeks as of July’s end, representing the first three decreases (excluding the pandemic) since the Great Financial Crisis. Spending has also been bolstered by consumers’ excess savings generated from unsustainable or expiring government initiatives such as Medicaid and the student loan moratorium. We have maintained that the consumer “tapping out” or a rise in unemployment could be the catalyst for the economy to weaken. Moreover, the yield curve has been inverted for eleven straight months; in the seven times it has inverted since 1978, on average, a recession has followed sixteen months later. Global M2 money supply growth has also recently touched 50-year lows as the liquidity picture grows increasingly murky. For portfolios, we have been recommending international equity markets for some time now and continue to do so, as we believe them to be behind the US in the business and inflation cycle. ROW markets continue to be attractively priced. As always, we advocate an allocation towards alternatives, a focus on high-quality, inflation hedges, and diversifying across factors.

For more news, information, and analysis, visit the ETF Strategist Channel.

Warranties & Disclaimers

As of the time of this publication, Astoria Portfolio Advisors held positions in IEMG, IVE, SPMD, SPY, SPSM, IVW, IEFA, MUB, TIP, AGG, IEF, HYG, LQD, BCI, GLD, USO, and SLV on behalf of its clients. There are no warranties implied. Past performance is not indicative of future results. Information presented herein is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. The returns in this report are based on data from frequently used indices and ETFs. This information contained herein has been prepared by Astoria Portfolio Advisors LLC on the basis of publicly available information, internally developed data, and other third-party sources believed to be reliable. Astoria Portfolio Advisors LLC has not sought to independently verify information obtained from public and third-party sources and makes no representations or warranties as to the accuracy, completeness, or reliability of such information. Astoria Portfolio Advisors LLC is a registered investment adviser located in New York. Astoria Portfolio Advisors LLC may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration requirements.