By Dan Zolet, CFA, Associate Portfolio Manager

SUMMARY

- US Equities close the year on top.

- US Growth took back leadership from US value.

- Portfolios maintain exposure to both growth and value themes.

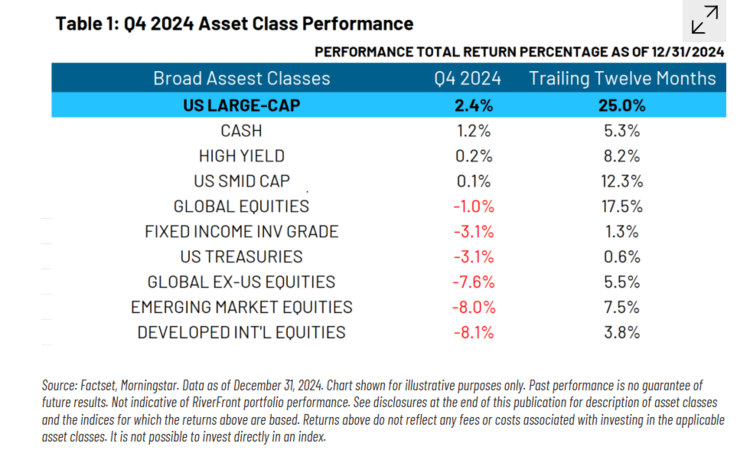

The fourth quarter of 2024 saw the predominant themes that drove the first two quarters of the year regain leadership after losing it briefly during the third quarter. For instance, the US regained leadership among global equity markets, while ’growth’ sectors posted better returns most of their ‘value’ counterparts.

Outside of the brief value rotation that occurred in Q3 overall 2024’s returns told a cohesive story, in our view. Mega-cap US growth continues to produce strong earnings in an environment where most other equities were unable to. We continue to believe that the macro environment is becoming more conducive for value-oriented assets to begin to change this trend, though both market performance and relative earnings trends suggest that this has yet to occur. With all of this in mind, let’s dive deeper into fourth quarter returns.

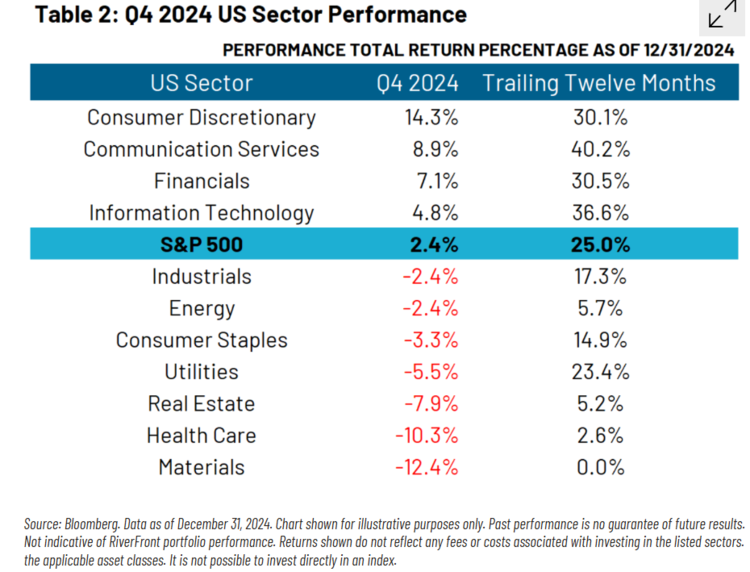

US Sectors: ‘Growth’ Back on Top

Table 2 (below) shows sector performance. Continuing a trend from the first half of the year, technology-related themes in Consumer Discretionary, Technology and Communication Services posted higher returns than the S&P 500. Joining them at the top was the Financials sector. With the Fed cutting, albeit at a slower pace than originally anticipated, the market is expecting a steeper yield curve which exists when shorter rates are lower than longer term rates. This type of environment is typically a boon for the traditional financial business models like Banking, because they tend to borrow at short term rates and lend at longer term rates.

We have discussed in past Weekly Views, that we believe the macro environment of an easing Fed and

moderate but elevated inflation should provide a tailwind for Value indexes. We began to see this in the 3rd quarter and briefly after the election, but these sectors fell noticeably in December. We believe this shift in sentiment was driven by Fed chair Powell’s guidance after the December Fed Meeting that they would be more cautious about cutting interest rates. Since defensive companies tend to be highly levered and have lower profit margins, the resulting rise in long-term treasuries was enough to dampen returns.

For other cyclicals, the issue they are facing is more around an uncertain economic environment. A steep yield curve implies the kind of healthy environment in which cyclicals can thrive for a sustained period, so any guidance that might make that destination less likely increases uncertainty. Since we are focused on a longer-term view and believe economic growth can continue and rates gradually decline, we continue to see opportunities in cyclical sectors. See our recently released Outlook: Goldilocks and the Two Bears, for more on this.

China Falters, US Dollar Strength Hits Everyone Else

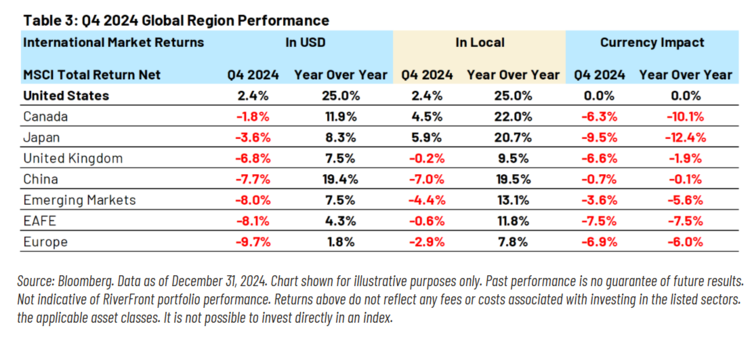

Moving to Table 3 below, each international market in our global universe posted a negative return for US investors. Europe was the largest laggard. Our view is that inflation and slow growth still loom large over this market and will continue to be a headwind in 2025.

Additionally, China’s negative return was a stark reversal of the last month of the third quarter. We believed that the market’s initial positive response to the country’s announced stimulus measures in Q3 would prove to be an overreaction, and we believe this more recent pullback represents an appropriate reconsideration of this exuberance.

In a reversal of the third quarter, each international currency in our universe depreciated relative to the US dollar, accounting for the majority of the negative returns we saw. While this dampened returns for US-based investors versus local investors, this could create a tailwind for more export driven markets in the future. This tailwind may occur because a weaker domestic currency makes exports less expensive, and thus more attractive for foreigners. Specifically, we believe a weak Japanese yen and British pound could potentially help the local earnings of Japanese and UK equities, moving forward.

Portfolios Currently Employing ‘Barbell’ Strategy Between Growth & Cyclicals

When looking at the differences between the third quarter and fourth quarter, we can see that a rotation in market leadership is never a smooth transition. To position our portfolios for this uneven rotation, we are currently employing a ‘barbell’ strategy within our equity selection. On one end, we are maintaining growth exposure through US mega-cap tech. We view this exposure as prudent given the strong earnings momentum in this space. On the other end of our barbell, we have cyclical exposure. We gain this exposure through large cap industrials and international value across all our portfolios, as well as US small- and mid-cap equities in our long horizon portfolios. These positions provide exposure to the value rotation that we still expect to be a theme in 2025. In order to offset our overweight in these two themes, and US stocks in general we are underweight defensive equites, international equities, and fixed income. An important difference between our long and short horizon portfolios is that the longer horizon portfolios are invested in longer-tenured Treasuries to help offset some of the higher potential risk associated with the higher volatility of our small- and mid-cap equities.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Originally Published at RiverFront Investment Group

For more news, information, and analysis, visit the ETF Strategist Channel.