SUMMARY

- We view Kevin Warsh as a credible choice for Fed Chair.

- Software companies’ shares have struggled as AI upstarts gain traction.

- We continue to favor technology-related themes, but prefer hardware to SaaS software.

The past week or so, the market has had a lot of news to absorb. President Trump’s appointment of Kevin Warsh to Fed Chair sparked volatility in the US dollar, rates, and precious metals. In addition, a rash of technology-related news caused a large selloff in software and broader tech shares. Today we sift through this tumult and share our views on where the market may be headed.

Kevin Warsh: Experienced, Pragmatic and Pro-Growth

While Warsh’s appointment still needs to be confirmed by the Senate, we expect him to survive confirmation. Warsh is not an unknown to the market, having previously served as a Fed Governor from 2006-2011 as well as a professional investor at prominent firms like Morgan Stanley and Duquesne. His experience in helping successfully restructure the banking system during the Great Financial Crisis suggests pragmatism, a cool head in crises, and a deep understanding of the US financial system…all positive traits for a Fed Chair. In summary, he is:

- An experienced practitioner who is savvy to the intricacy of the US financial system and markets

- An outspoken critic of the Fed’s past reliance on quantitative easing and balance sheet expansion, as well as their tendency to ‘overcommunicate’ to the public

- An eloquent champion of pro-growth fiscal and monetary policy and less corporate regulation – in that way, he is a good fit for the Trump Administration, in our view

- A believer – as are we – that the effects of "artificial intelligence":https://www.riverfrontig.com/insights/ai-the-future-is-happening-part-one/ are generally productivity-enhancing and disinflationary

- Aligned with Treasury Secretary Scott Bessent in views, background, and shared experience: Warsh has expressed that Treasury and the Fed should coordinate policy, keeping the Fed focused simply on monetary policy

The bottom line is that we view Warsh as a credible choice for Fed Chair, who is likely to be pro-growth, shake up the status quo regarding policy choices and communication, yet respect the independence and apolitical nature of the office. While the US dollar, bond yields and precious metal prices were initially volatile in the wake of his announcement, we think markets will eventually accommodate his influence. We don’t view Warsh’s appointment as a reason to change our overall constructive view of US markets. In addition, we suspect that the global rotation into value and cyclical stocks – in place well before Warsh was appointed – may continue in light of his policies.

Tech Spending and the Anthropic Announcement – What to Make of the ‘SaaSpocalypse’

New AI companies threaten traditional software incumbents. Software-as-a-service (SaaS) is a business term for buying software as a regular subscription rather than as a one-time installed product. It is how most software is now delivered, and is a better model for software companies as it provides a regular stream of income. 2026 has witnessed an ongoing bout of selling pressure in SaaS stocks – aka the ‘SaaSpocalypse’ – as investors assess how newly-released AI models might replace existing software. This week the private company Anthropic did just that by announcing an upgrade to its Cowork AI assistant, which has the potential to replace existing software in areas like financial and legal analysis.

Big earnings, big spending. While the most acute selling has so far been confined to software companies, technology shares’ performance in general in ‘26 has also suffered from increasing concerns over an AI spending ‘bubble.’ Bellwethers such as Alphabet (Google) and Microsoft beat earnings estimates last week, but also guided the Street to higher-than-expected capex, which marred otherwise strong earnings announcements. According to a recent MSN article, the four largest tech companies are likely to spend approximately $650bn on AI infrastructure this year alone. For the major technology companies who are spending so much to build the AI infrastructure and develop products, the key is whether they ultimately get a good return on that investment. The uncertainty of that answer is what is creating the volatility in their share prices. In general, we are optimistic on mega-cap tech, but acknowledge that this is a hotly debated issue on Wall St. and Main St. alike. We would make two important points here:

- AI creates winners and losers – we prefer hardware over software: We have written a lot about the macro and micro effects of AI on markets – one thing that is clear to us is that AI is a disruptive technology that will create clear winners and losers at the company and industry level, even as it creates broad productivity and economic growth across the US economy. Late last year, we wrote about the AI Gold Rush, broke AI business models down into those spending to build infrastructure, those developing new products and those benefiting from the spending buildout. For now, we believe semiconductor companies are the big winners from all the spending – and it remains to be seen whose products will ‘win’ the AI race.

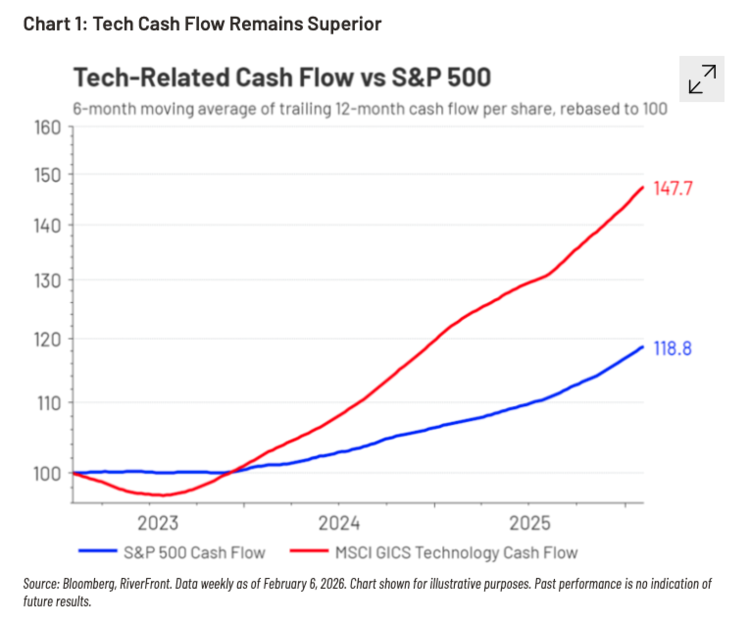

- The tech sector as a whole is still a winner: We view concerns of a significant slowdown in AI spending as unlikely in 2026 while maintaining a preference for AI ‘picks and shovels’ providers over smaller AI model provider ‘miners’. We believe this preference continues to be justified by recent earnings and cash flow results – mega-cap technology cash flows have well outpaced the broader S&P 500 over the last three years (Chart 1, above). When looking at our current portfolio positioning, all our portfolios are overweight hardware relative to their benchmarks, with individual stock positions in each of these segments where our models allow it. Additionally, we have broad exposure to physical infrastructure through thematic ETFs in our longer horizon portfolios.

Conclusion: Recent Volatility Unlikely to Persist, in Our View

As we recently discussed in our January 21st ‘Three Rules’ update, the market has entered the new year with a strong trend but highly optimistic crowd sentiment…suggesting a potential near-term pause in the market uptrend. The recent volatility over the Warsh appointment and software’s struggles may be the beginning of such a pause. As always, the difficulty for a tactical investor is determining which market corrections will be deep and prolonged enough to try and successfully time, especially as both the trend and macro fundamentals continue to suggest to us a positive market stance. Our current view is that the current volatility will likely be too brief and shallow to be able to successfully avoid without ‘whipsawing’ investors, ala last April’s ‘Liberation Day’ meltdown (and dramatic subsequent rebound). Nonetheless, we are closely monitoring both fundamental and technical indicators for any degradation that may cause us to become more tactically cautious.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Originally posted at RiverFront Investment Group on February 10

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

The comments above are subject to change and are not intended as investment recommendations. There is no representation that an investor will or is likely to achieve positive returns, avoid losses or experience returns as discussed for various market classes.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

All charts shown for illustrative purposes only. Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

In general, the bond market is volatile, and fixed income securities carry interest rate risk. (As interest rates rise, bond prices usually fall, and vice versa). This effect is usually more pronounced for longer-term securities). Fixed income securities also carry inflation risk, liquidity risk, call risk and credit and default risks for both issuers and counterparties. Lower-quality fixed income securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer. Foreign investments involve greater risks than U.S. investments, and can decline significantly in response to adverse issuer, political, regulatory, market, and economic risks. Any fixed-income security sold or redeemed prior to maturity may be subject to loss.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Technology and internet-related stocks, especially of smaller, less-seasoned companies, tend to be more volatile than the overall market.

Artificial intelligence, or AI, refers to the simulation of human intelligence by software-coded heuristics. Nowadays this code is prevalent in everything from cloudbased, enterprise applications to consumer apps and even embedded firmware

Index Definitions:

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

A yield curve is a graphical representation of yields over time; it’s often depicted by plotting the yield of any given bond across different maturities in a given interval, perhaps by month.

Definitions:

Software as a Service (SaaS) is a software licensing model that provides access to applications via the Internet on a subscription basis, eliminating the need for local installation and maintenance.

Disinflation is a temporary slowing of the pace of price inflation. The term is used to describe occasions when the inflation rate has reduced marginally over the short term.

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio.

Don’t Fight the Fed – ‘Supportive’ means the Fed’s monetary policy regarding inflation and employment is in what we believe based on our analysis to be the investors’ best interest; ‘Against’ means the Fed’s monetary policy, in our view, is going against the investors’ best interest; ‘Neutral’ means the Fed’s monetary policy is neither supportive or against the investors’ best interest in our view. Don’t Fight the Trend – Terms correlate to the 200-day moving average as it relates to the equity indexes: ‘Positive’ means that the trend is rising, ‘Flat’ means the trend is flat, ‘Negative’ means the trend is falling. Beware the Crowd at Extremes – Terms correlate to the NDR Crowd Sentiment Poll and its measurement of Extreme Optimism (Bearish), Neutral, or Extreme Pessimism (Bullish).

Mega cap is a designation for the largest companies in the investment universe as measured by market capitalization. While the exact thresholds change with market conditions, mega cap generally refers to companies with a market capitalization above $200 billion.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

_To review other risks and more information about RiverFront, please visit the website at riverfrontig.com and the Form ADV, Part 2A. Copyright ©2026 RiverFront Investment Group. All Rights Reserved. [ID 5202758]

_