The current economic landscape is often defined by its loudest headlines: geopolitical strife, shifting central bank leadership, and the ghosts of sticky inflation. However, the challenge for disciplined investors lies in peering through this noise to discern the structural engines driving the U.S. economy. While uncertainty has undeniably increased following recent military actions in the Middle East, the underlying economic momentum suggests a diversified resilience that continues to defy pessimistic forecasts.

A cursory glance at the labor market suggests stagnation with net new jobs growth averaging close to zero since August 2024. Nevertheless, the unemployment rate has remained remarkably steady. As the graph below illustrates, this apparent paradox is explained by a simultaneous cooling in labor force growth. Even though the measure of labor force growth is more volatile than jobs growth, they are both moving in the same direction. While we expect modest employment gains as the bulk of federal government downsizing has concluded, the real story is not the quantity of workers, but their efficiency.

Real, inflation adjusted, economic growth is the sum of labor force expansion and productivity. With the former stalling, the latter has stepped up as the primary driver. Healthy GDP growth in this environment indicates a robust increase in productivity, which is the ability of employees to increase their output per hour and generate higher revenue per worker.

For investors, this is a critical tailwind as productivity drives both corporate earnings and real income growth, even when the headline jobs count remains muted.

It is impossible to ascertain when major combat operations in the Middle East will end, but we can think through these uncertainties using our multiple scenario analysis (MSA) framework of best-case, base-case, and worst-case scenarios. For the best-case scenario, the conflict ends quickly and we are soon back to normal levels of energy production and transport. While oil may not retreat to its pre-conflict levels due to a continued uncertainty premium, energy prices would likely fall, and financial markets would respond accordingly.

Our base-case scenario is that the conflict lasts for a number of weeks. This would likely keep energy prices elevated, favoring energy-related investments, and act as a headwind to the global economy and stock markets.

The worst-case scenario would obviously be a prolonged conflict and higher energy prices for a sustained period of time. While this scenario would be a challenge to energy importers, such as the major Asian and European economies, it will likely not be a major headwind to the U.S. economy. As a net energy exporter, the U.S. might even benefit overall from higher prices, though consumers would not like that outcome. Furthermore, the U.S. economy is far less energy intensive and energy price sensitive than it was in previous decades. As a result, this uncertainty favors U.S. equities over foreign.

Inflation remains a complex beast. While housing price gains have subsided, keeping a lid on core metrics, headline pressures are being stoked by the Strait of Hormuz crisis, which is a critical sea passage in the Persian Gulf. While the media focuses on the 20% of global oil passing through the Strait, the 30% of global fertilizer production also routed through the same channel is arguably just as vital. Higher fertilizer costs bake sticky prices into global agriculture, and could keep inflation lingering near 3%, well above the Fed’s 2% target.

This situation adds to pressure on the K-shaped economy where upper-end households benefit from the wealth effect while others struggle. Higher food and fuel costs squeeze household budgets even as other areas of the economy continue to grow. We expect the Fed, remaining data-dependent under new leadership, to navigate this by gradually bringing rates toward a “neutral” level of 3%. Current market pricing reflects a 60% probability of reaching this target by the end of 2026, a reasonable expectation in our view given the tug-of-war between sluggish hiring and persistent prices.

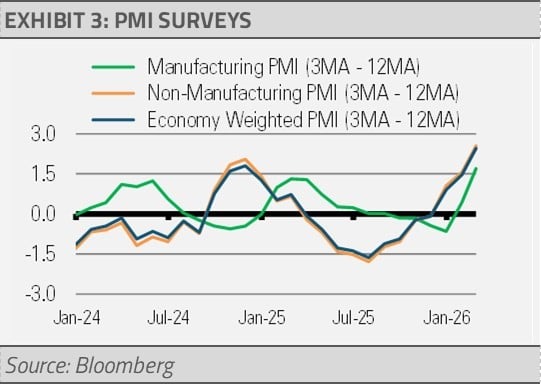

Despite consumer softness in early 2026, industrial production and business surveys have turned sharply positive. Our economically weighted Purchasing Manager Index (PMI) model shows momentum moving higher, which reflects an economy where industrial strength may outweigh consumer caution. This is another example of the resilience of the U.S. economy that is so diverse that weakness in one sector may be offset by improvements in another.

INVESTMENT IMPLICATIONS

In this environment, our allocations remain tilted toward U.S. equities, specifically healthcare, industrials, and regional banks as well as small caps. We continue to favor the belly of the yield curve and asset-backed securities in fixed income.

To manage volatility and enhance yield, we utilize equity option overlays and multi-sector real return ETFs, which provide exposure to the commodities and sectors that may benefit from today’s geopolitical and inflationary realities, such as energy and infrastructure.

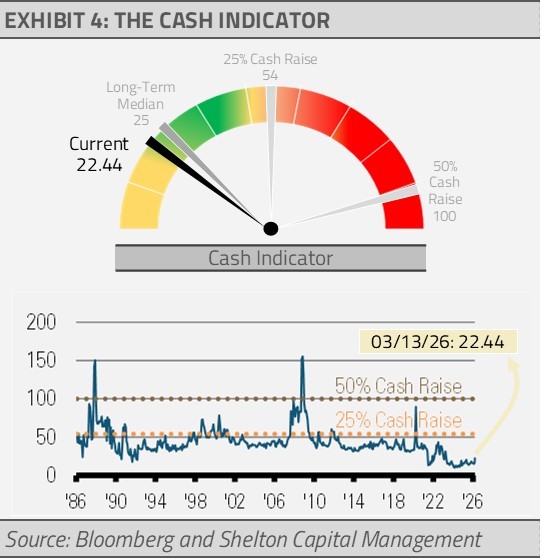

THE CASH INDICATOR

The Cash Indicator (CI) has elevated to reflect geopolitical and financial market uncertainties. However, the current level has only risen closer to the long-term median level. Increased market volatility has largely been offset by relatively steady credit markets. As things stand, the CI does not suggest an impending market dislocation. Rather, combined with the positive economic backdrop, the CI suggests that investors should stay the course.

For more news, information, and analysis, visit the ETF Strategist Content Hub.

Disclosures

Shelton Capital Management is an investment adviser in Denver, CO. Shelton Capital Management is registered with the Securities and Exchange Commission (SEC). Registration of an investment adviser does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. Shelton Capital Management only transacts business in states in which it is properly registered or is excluded or exempted from registration. Some of the firm’s strategies allocate client’s investment management assets among exchange-traded funds (“ETFs”). A GIPS Report along with a complete list and description of all composites is available by calling (800) 955-9988. A copy of Shelton Capital Management’s current written disclosure brochure filed with the SEC which discusses among other things, Shelton Capital Management’s business practices, services and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov. INVESTMENTS ARE NOT FDIC INSURED OR BANK GUARANTEED AND MAY LOSE VALUE. The views contained herein are not be taken as an advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted. The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Shelton Capital Management and has not been verified or audited by an independent accountant.