Economic indicators play a central role in understanding the health and performance of the U.S. economy. They are essential tools for policymakers, advisors, investors, and businesses because they allow them to make informed decisions regarding business strategies and financial markets. In the week ending on November 22nd, the SPDR S&P 500 ETF Trust (SPY ) rose 1.07% while the Invesco S&P 500® Equal Weight ETF (RSP ) was up 1.16%.

In this article, we look at three indicators from the past week – Michigan consumer sentiment, existing home sales, and the Conference Board’s Leading Economic Index (LEI). Examining these data points provides valuable information about different aspects of the country’s overall economic health and all can be considered as leading indicators.

Michigan Consumer Sentiment

Consumer sentiment worsened for a fourth consecutive month in November. According to the final report of the Michigan Consumer Sentiment Survey, the index fell to a six-month low, settling at 61.3. This represents a 3.9% decrease from October’s final reading and is slighlty higher than the forecasted value of 60.4. To put the latest figure into a historical context, the current index level is at the 5th percentile of the series, highlighting the persistantly subdued sentiment consumers have felt since the beginning of the pandemic.

The Michigan Consumer Sentiment Index is a monthly survey measuring consumers’ opinions with regards to the economy, personal finances, business conditions, and buying conditions. In the latest report, current assesments and future expectations of personal finances improved from October while future expectations of business conditions plummeted to its lowest level since July 2022. Additionally, inflation continues to be a top concern despite consumers recognizing that inflation has cooled recently. Inflation expectations for both the short term and long term increased in November, hinting at consumer worries that inflation may resurge in the coming months.

The Consumer Discretionary Select Sector SPDR ETF (XLY ) is tied to consumer sentiment.

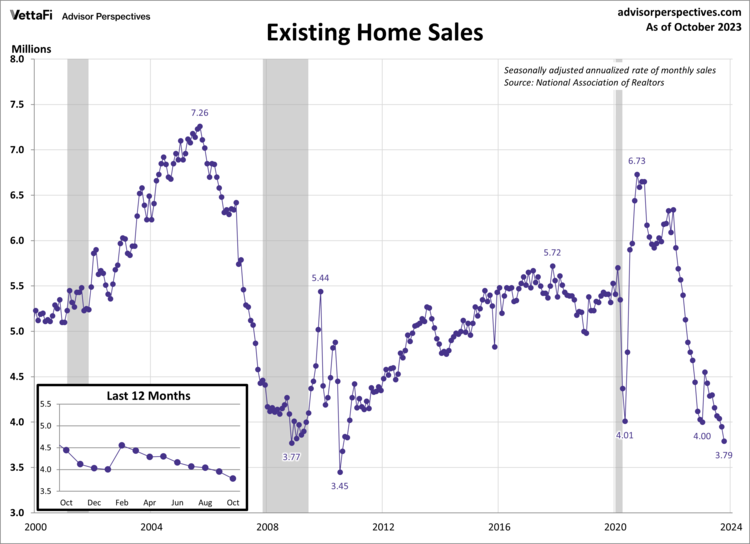

Existing Home Sales

Elevated mortgage rates and a lack of inventory continue to impact existing home sales which have fallen even further, remaining at their slowest pace since 2010. In October, existing home sales fell by 4.1% to a seasonally adjusted annual rate of 3.79 million units. This decline marks the 19th drop in the past 21 months, highlighting the consistent downward trend in existing home sales over the past few years. The latest figure was lower than expected, with sales falling short of the projected 3.90 million units. While inventory remains low, the National Association of Realtors predicts that recent drops in mortgage rates will result in an increase in inventory and ultimately an improvement in home sales.

The lack of inventory has created competition among potential homebuyers which has led to multiple offers on a home and subsequent price hikes. The median price for an existing home sold in October was $391,800, representing a 3.4% increase compared to one year ago. This is the fourth straight month of year-over-year increases for existing homes.

Leading Economic Index

The Conference Board Leading Economic Index (LEI), a composite index designed to predict the economy’s trajectory, resumed its recession signal for the near term. October marked the 19th consecutive month of decline for the LEI, with a 0.8% drop to 103.9 – its lowest level since May 2020. The Conference Board has updated their recession prediction to reflect a very short recession in 2024 because of elevated inflation, high interest rates, and a reduction in consumer spending. The only other times the index has declined for 19 months or longer was during runups to the Oil Embargo Recession (1973-1975) and the Great Recession (2007-2009).

In October, the majority of the index’s components were flat or made negative contributions. The largest declines came from consumers’ expectations for business conditions, ISM® Index of New Orders, S&P 500 Index of stock prices, and the interest rate spread (10-year Treasury bonds less federal funds rate). Positive contributions were made by the manufacturer’s new orders for consumer goods and materials and building permits.

Economic Indicators and the Week Ahead

The upcoming week will deliver some of the most closely watched data that provides insight into consumption and consumer attitudes. On Tuesday, the Conference Board will report the November reading for their Consumer Confidence Index. Consumer attitudes have worsened each of the last three months, which could impact the Consumer Discretionary Select Sector SPDR ETF (XLY ). Then on Wednesday, the Bureau of Economic Analysis (BEA) will release the second estimate of the 2023 Q3 GDP. As a reminder, the 2023 Q3 advance estimate came in at 4.9%, more than twice as much as the 2023 Q2 final estimate of 2.1%. Lastly, the BEA will publish October’s PCE price index data on Thursday. The core PCE price index, the Fed’s preferred measure of inflation, will tell us if inflation continues its downward trend towards the Fed’s 2% target rate.

For more news, information, and analysis, visit the Innovative ETFs Channel.