Last week’s economic reports presented a narrative similar to what we’ve seen over the past few months: resilience coupled with concerns. The labor market demonstrated continued strength, but with signs of moderation. Both the service and manufacturing sectors expanded, yet each revealed underlying vulnerabilities. The service sector’s growth was tempered by uncertainty regarding tariffs and federal spending cuts, while manufacturing faced rising inflationary pressures. Compounding these concerns, recent GDP forecasts have shown negative growth in the first quarter, further fueling market volatility. These factors have collectively contributed to the market wiping out nearly all gains seen since the November election, leaving investors and policymakers navigating a landscape marked by uncertainty and shifting economic tides.

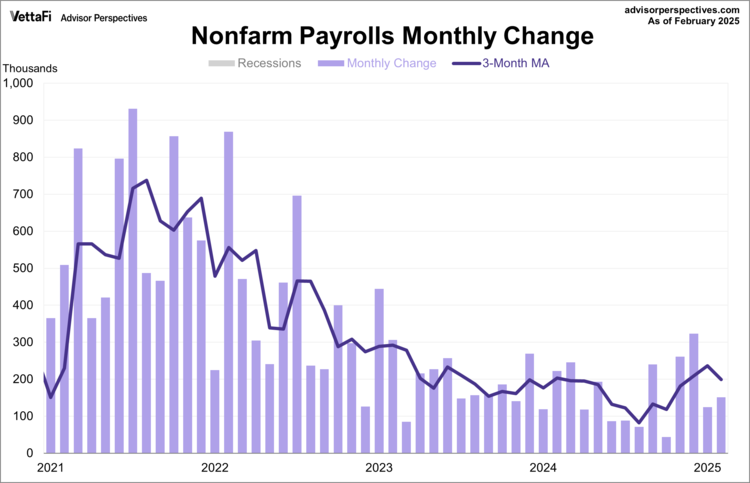

Employment Report

The U.S. labor market added fewer jobs than expected in February but remained strong. The latest employment report showed that 151,000 jobs were added last month, falling short of the expected 159,000 but a slight pick up from January’s 125,000 gain. Meanwhile, the unemployment rate unexpectedly inched up to 4.1% from 4.0% in January, remaining near historically low levels. Wage growth also remained stable, with average hourly earnings increasing by 0.3% from the previous month, aligning with expectations. Annually, wages grew by 4.0%, a minor acceleration from 3.9% in January but lower than the projected 4.1% growth.

The labor market has shown resilience, with 50 consecutive months of job growth, despite elevated interest rates in recent years. While the latest jobs report supports the narrative of resilience, concerns have arisen regarding a potential downturn due to mass layoffs of federal workers and ongoing tariff uncertainty.

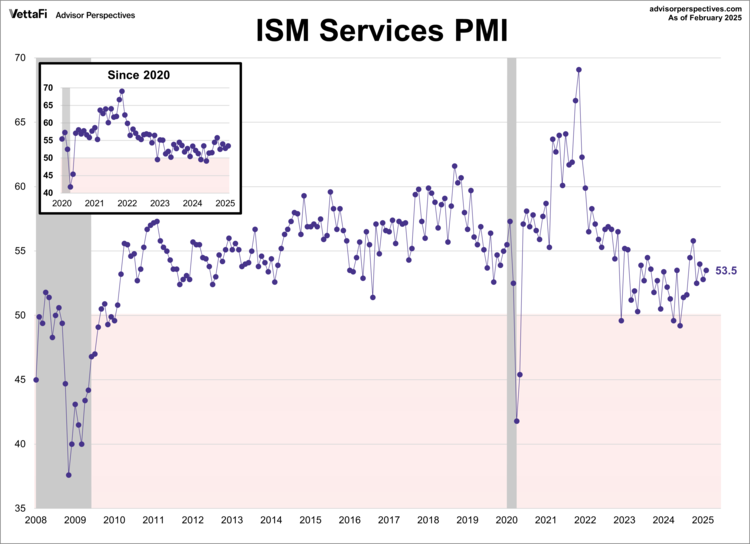

ISM Services

The U.S. services sector continued to expand in February, marking its eighth consecutive month of growth. The ISM Services PM unexpectedly rose to 53.5 from 52.8 in January. The index was expected to inch down to 52.5. All four components that factor directly into the PMI were in expansion territory last month. Despite this, the business activity subindex reported slower growth, primarily due to concerns regarding tariffs and federal spending cuts. The services sector has now expanded in 24 of the last 26 months, dating back to January 2023. However, respondents indicated significant uncertainty about the future and expressed doubt regarding continued growth.

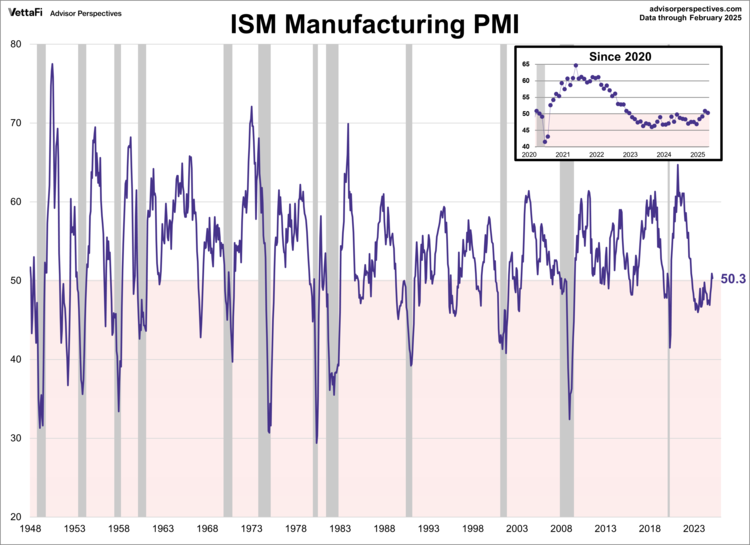

ISM Manufacturing

U.S. manufacturing activity expanded in February but was weaker than expected. The ISM Manufacturing PMI inched down to 50.3 from 50.9 in January, falling short of the 50.6 forecast. Despite the overall growth, several subcomponents hinted at inflationary pressures on the rise because of tariffs. The New Orders and Employment components slumped into contraction territory last month, while price pressures surged to nearly a three-year high. The manufacturing sector has now expanded for two straight months, following 26 consecutive months of contraction. However, respondents reported significant concerns regarding tariffs and their overall impact for future growth.

ETFs associated with industrials and manufacturing include: First Trust Industrials/Producer Durables AlphaDEX Fund (FXR ), Industrial Select Sector SPDR Fund (XLI ), Vanguard Industrials ETF (VIS ), and iShares U.S. Industrials ETF (IYJ ).

Market Reactions

The S&P 500 dropped 3.1% this week, its largest weekly decline since September. As a result, the SPDR S&P 500 ETF Trust (SPY ) fell 3.0% last week. Meanwhile, the S&P Equal Weight Index fell 2.0% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP ) was down 1.9%.

The 10-year Treasury yield finished the week at 4.32%, while the 2-year note finished at 3.99%.

According to the CMEFedWatch tool, markets are currently pricing in three rate cuts in 2025. The anticipated cuts are now expected at the June, September, and December meetings.

Economic Data in the Week Ahead

The upcoming week will be packed with important economic data. The Bureau of Labor Statistics will release the JOLTS report for January on Tuesday, followed by the Consumer Price Index (CPI) for February on Wednesday, and the Producer Price Index (PPI) for Thursday. These reports will be closely monitored as the labor market and inflation continue to be major areas of focus for the Fed. To close out the week, the University of Michigan will release its preliminary consumer sentiment report for March on Friday, which has recently caused market fluctuations due to heightened consumer concerns around tariffs and inflation.

For more news, information, and analysis, visit the Innovative ETFs Channel.