Economic indicators are released every week to provide insight into the overall health and performance of an economy. They serve as essential tools for policymakers, advisors, investors, and businesses. That is because they allow them to make informed decisions regarding business strategies and financial markets. In the week ending June 6, the SPDR S&P 500 ETF Trust (SPY ) rose 2.31%. In the same time frame, the Invesco S&P 500 Equal Weight ETF (RSP ) was up 0.90 %.

Among all economic indicators, some of the most closely watched are those surrounding the labor market. They provide insight into the health of the economy, impact individuals’ lives, and play a central role in government policy decisions. Last week, several employment updates were released that offer insights into different aspects of the U.S. labor market. This article discusses the key data points from each report and explore their potential implications.

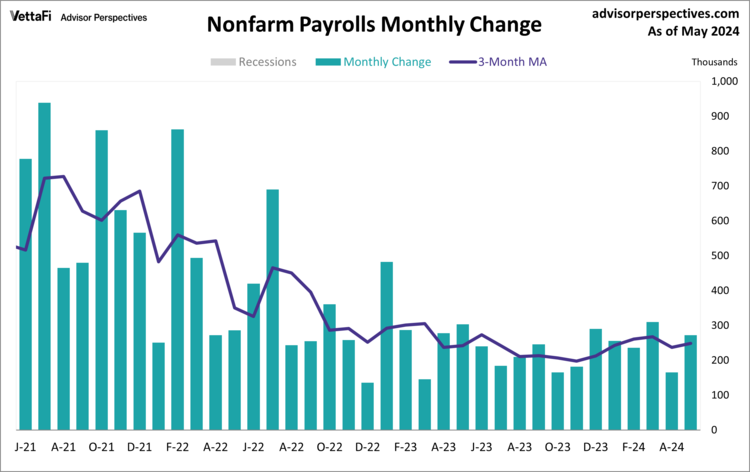

Employment Report

The U.S. labor market added more jobs than expected last month as the labor market remains surprisingly hot. The May employment report revealed 272,000 jobs were added last month. That exceeded the expected 182,000 addition. May’s jobs numbers were a pickup from April’s downwardly revised 165,000 addition.

The report also revealed a slight increase in the unemployment rate to 4.0%. That’s its highest level since January 2022. Additionally, hourly earnings saw a larger-than-anticipated rise. Monthly wages gained 0.4% compared to the forecasted 0.3%. On an annual basis, wage growth accelerated to 4.1% instead of the anticipated slowdown to 3.9%.

Overall, the latest jobs report reinforces expectations that the Fed will hold off on cutting rates at its meeting next week. It could prolong the first cut even more.

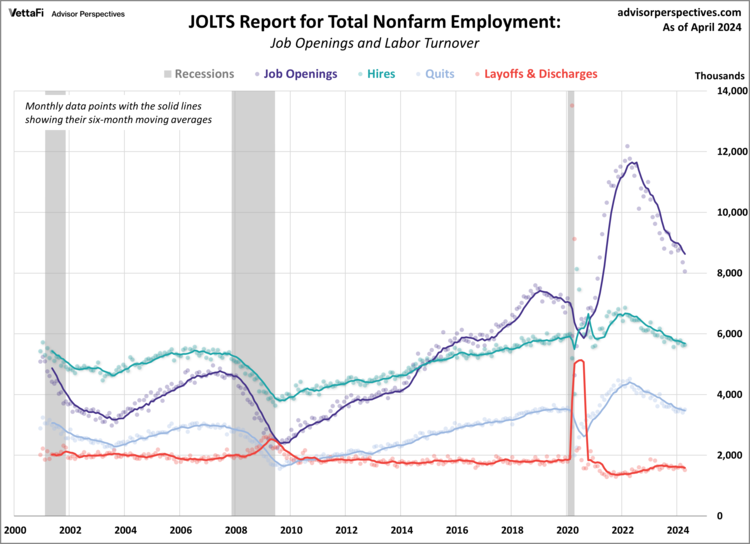

Job Openings and Labor Turnover (JOLTS)

Unlike the BLS’ May jobs report, the April JOLTS report highlighted an easing labor market as job openings fell to its lowest level since February 2021.The number of job openings decreased by 296,000 to 8.059 million. That was below the predicted 8.370 million vacancies. Job openings have steadily declined over the past two years. But they remain above prepandemic levels.

Other key data points from the report showed that the number of hires and quits increased from the previous month while layoffs declined. Most notably, the number of layoffs dropped to 1.5 million. That’s the lowest level since January 2022.

The JOLTS data serves as a barometer for assessing labor demand. Any disparity between workforce demand and supply could potentially exert upward pressure on inflation. Since the beginning of 2023, the gap between the two has consistently narrowed as the overall trend in job openings declined from its 2022 peak. In April, the number of job openings per employed worker dropped to 1.24. That’s the lowest level in almost three years.

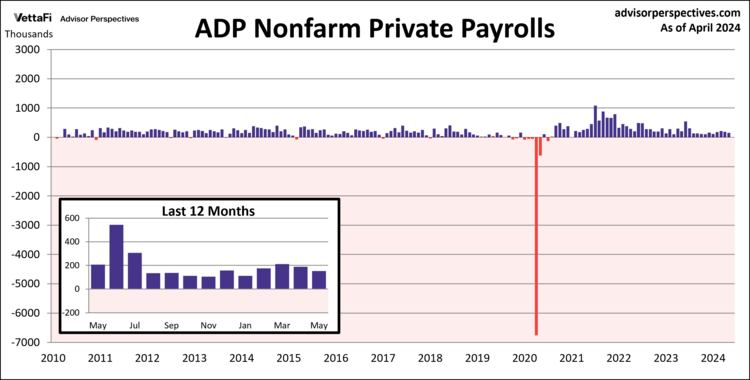

ADP Employment Report

Nonfarm payroll employment increased and exceeded expectations in May. But the same cannot be said for the private sector. The ADP employment report showed 152,000 private jobs were added in May. That’s less than the projected 173,000 addition. The report also revealed little change in pay growth, with pay gains for job-stayers remaining at 5.0% for a third consecutive month. Meanwhile, pay gains for job-changers fell for a second straight month to 7.8%. But that remains higher than at the start of the year.

The pickup in May was most notable among large companies (500+ employees), as they added 98,000 jobs combined. That accounts for almost 65% of May’s private job growth. Additionally, a handful of industries decreased hiring last month. The majority of job losses came from goods-producing industries such as manufacturing and natural resources and mining.

Despite the latest downtick, the six-month moving average — a more stable indicator amid monthly volatility — increased for a fourth straight month to 166,000 in May. The six-month moving average is now at its highest level in the past six months.

Economic Indicators and the Week Ahead

The big news this week will be the Fed’s meeting on Tuesday and Wednesday. They are expected hold rates steady between 5.25% and 5.50% for a seventh straight meeting. Additionally, the economic calendar will feature the latest inflation and sentiment data.

On Wednesday, the Bureau of Labor Statistics will release May’s Consumer Price Index (CPI) followed by the Producer Price Index (PPI) on Thursday. Consumer prices are expected to increase 0.2% and 0.3% from May for the headline and core indexes, respectively. Producer prices are expected to increase 0.2% and 0.3% for the headline and core indexes, respectively.

Then on Friday, the preliminary report for the Michigan Consumer Sentiment Index, which could impact interest in the Consumer Discretionary Select Sector SPDR ETF (XLY ), is predicted to increase to 73.0 from May’s final reading of 69.1.

For more news, information, and analysis, visit the Innovative ETFs Channel.