Last week’s economic data presented a challenging picture for the U.S. economy. Key inflation reports delivered conflicting signals: consumer prices showed signs of heating up, even as business-side inflation unexpectedly fell. Meanwhile, consumer sentiment dipped for a second straight month, and a timely labor market indicator added to the narrative of a weakening job environment.

The data helped solidify the odds of a Fed rate cut this week, which fueled a four-day win streak for the S&P 500 and led to three new record highs. However, the path ahead for the Fed remains complicated as it balances the need to support a softening labor market without stoking inflation.

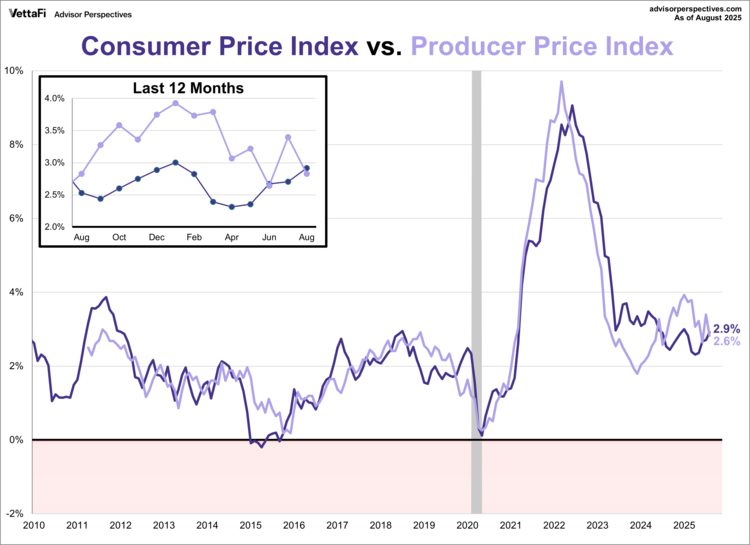

Inflation

Consumer inflation heated up in August, reaching its highest level in seven months. The Consumer Price Index (CPI) rose to 2.9% last month, up from 2.7% in July and in line with expectations. On a monthly basis, prices were up 0.4%, surpassing the expected 0.3% increase. Core inflation, which excludes volatile food and energy, remained at 3.1% in August and prices were up 0.3% from the previous month. Both readings were consistent with their respective forecasts.

However, business-side inflation told a different story, as the Producer Price Index (PPI) unexpectedly fell in August. The index dropped 0.1%, down from July’s 0.7% increase and well below the expected 0.3% growth. On an annual basis, wholesale prices rose 2.6%, a slowdown from 3.1% in July and significantly lower than the expected 3.3% growth.

The PPI is considered a leading indicator of consumer inflation, as falling costs for producers often precede a slowdown in consumer prices. Despite the unexpected drop in wholesale prices, consumer prices have now accelerated for four consecutive months. This highlights the persistent and sticky nature of inflation, casting doubt that the pressure relief will reach consumers in the near future.

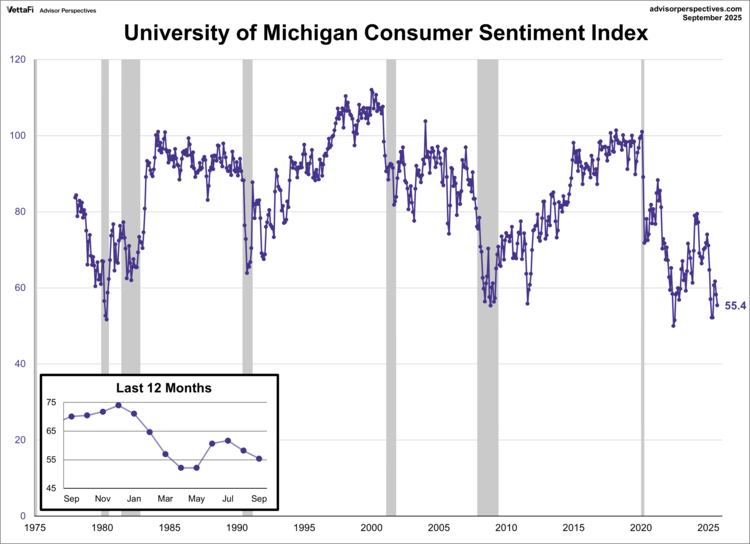

Consumer Sentiment

Consumer sentiment fell for a second consecutive month in September, reaching its lowest level since May. The University of Michigan Consumer Sentiment Index dropped by nearly 5.0% to 55.4 this month, coming in below the forecast of 58.2.

The index’s deterioration was driven by consumers’ lingering concerns about business conditions, the labor market, and inflation. However, the overall decline was mitigated by less pessimistic views on current and expected personal finances, which both eased by about 8% this month.

Inflation expectations for the near term held steady at 4.8% for the year ahead. Meanwhile long term expectations heated up for a second straight month, jumping from 3.5% to 3.9% for the five-year outlook.

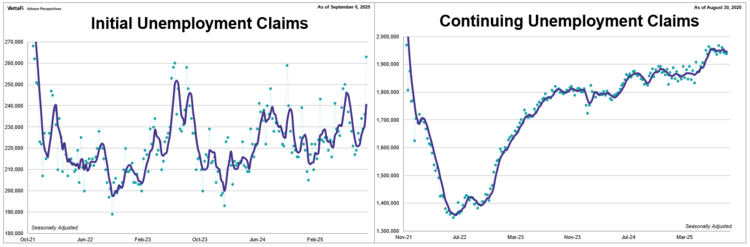

Weekly Unemployment Claims

The number of people who filed for unemployment for the first time jumped to its highest level in nearly four years. Initial jobless claims by 27,000 from the previous week’s figure to 263,000, its largest weekly rise in almost a year. The latest reading, with data through September 6th, was significantly higher than the forecast of 235,000.

Meanwhile, the number of people who had already filed for unemployment and continued to claim benefits was unchanged at 1.939 million. The latest reading, with data through August 30th, was just below the 1.950 million forecast.

Over the past few months, initial claims have steadily risen while continuing claims have hovered near multi-year highs. The latest report underscores the increasing weakness in the labor market, suggesting that workers are facing greater difficulty in both finding and keeping a job.

Market Reactions

The S&P 500 three new record highs last week, ultimately finishing up 1.6%. This marks the index’s fifth weekly gain in the past six weeks. As a result, the SPDR S&P 500 ETF Trust (SPY ) rose 1.6% last week. Meanwhile, the S&P Equal Weight Index was up 0.3% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP ) rose 0.3%.

The 10-year Treasury yield the week at 4.06%, while the 2-year note finished at 3.56%.

The CME FedWatch Tool currently shows a 94% chance of a 25 basis point rate cut and a 6% chance of a 50 basis point cut at this week’s Fed meeting. Markets are also pricing in two additional 25 basis point cuts at the October and December meetings this year and three more in 2026.

Economic Data in the Week Ahead

The week ahead will be led by the Fed’s next interest rate meeting, which will be the primary focus for market watchers. Other highly anticipated releases include Retail Sales and Industrial Production, which will offer key insights into the health of the consumer and the manufacturing sector, respectively. The housing market will also be in focus with the latest readings on Housing Starts, Building Permits, and the Zillow Home Value Index. Finally, a look into regional factory activity will be provided by the Empire Fed and Philadelphia Fed Manufacturing Indexes, while a fresh read on the labor market will come from Weekly Unemployment Claims.

Originally published at Advisor Perspectives

For more news, information, and analysis, visit the Innovative ETFs Content Hub.