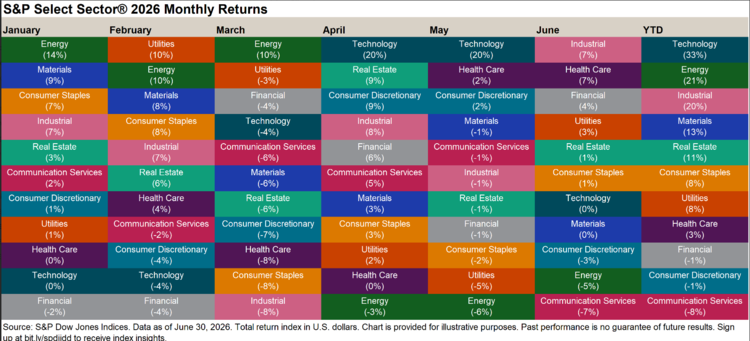

The top performing sector SPDR’s in 2026 were led by the State Street Technology Select Sector SPDR Fund (XLK ) with gains of 33% year-to-date, followed by the State Street Energy Select Sector SPDR Fund (XLE ) and the State Street Industrial Select Sector SPDR Fund (XLI ), which rose 21% and 20% respectively in the first half of 2026.

Key Takeaways

- XLK leads sector performance with 33% a return in 2026, despite a June pullback fueled by investor apprehension over AI infrastructure spending and the Federal Reserve hinting toward future rate hikes.

- The Energy sector performed strongly in the first half of 2026, with XLE rising 21%, largely powered by supply disruptions and geopolitical-driven price premiums earlier in the year.

- Industrial performance was fueled by the sustained AI data center buildout, steady demand for aerospace and defense projects, and increased commodity equipment upgrades, resulting in a 20% gain for XLI.

Tech Sector Leads YTD Despite June Underperformance

Despite an anomalous rally in early Q2, where tech valuations reached record highs, mega-cap tech stocks lagged in June, primarily driven by high valuations, caution around AI spending, and shifting macroeconomic headwinds.

Many investors rotated out of large-cap tech and into value stocks to lock in profits. They were responding to growing apprehension over the massive AI capital expenditures from hyperscalers and concerns about when revenues from these massive infrastructure projects might actually be seen. Compounding these fears, surging component costs for memory and storage chips threaten profit margins and force price hikes for vital AI infrastructure components.

Driven by a better-than-expected May jobs report paired with sticky inflation, the Federal Reserve took a hawkish stance at the last meeting, hinting towards future rate hikes later in the year to combat inflation. The looming threat of rising rates heavily pressured growth-oriented tech stocks, contributing to the sector underperformance seen in June.

While tech underperformed in June relative to other sectors, XLK still leads sector year-to-date returns. This sustained performance is insulated by a buffer from the tech outperformance seen early in Q2, as well as heavy portfolio weighting towards semiconductor developers who have seen strong gains throughout 2026.

As we look ahead to the second half of the year, XLK’s top holdings continue to feature a strategic mix of semiconductor developers and mega-cap tech giants.

Nvidia (NVDA), with a 14.66% weight in the fund, saw a return of 5.4% YTD, while Broadcom (AVGO), weighted at 5.48%, returned 7.08% over the same period. Fueling XLK gains, Micron (MU), weighted at 5.52%, saw substantial gains of over 290%, driven in part by the firm’s thriving storage and memory chip business

Apple (AAPL) sits at a 12.85% portfolio weight in XLK and rose 6.28% for the first half of the year, while Microsoft (MSFT), with an 8.50% weight, dragged on portfolio gains with a loss of -22.99%. Despite beating analyst expectations on both top and bottom lines, growing investor skepticism over Microsoft’s heavy AI spending, triggered a major selloff in June, resulting in a near 20% price decline for the month.

Semiconductors Remain As Tech's Stronghold

Energy Surge and Stabilization

The energy sector surged roughly 37% in Q1 driven by supply disruptions and geopolitical tensions in the Middle East that allowed firms across the value chain to benefit from price premiums. However, this performance for many holdings stuttered in Q2 as geopolitical tensions in the Middle East showed signs of normalization, eroding the oil price premiums seen earlier in the year.

XLE’s two largest holdings come from the integrated supermajors — Exxon Mobil (XOM) at a 22.40% portfolio weight and Chevron (CVX) with a 16.24% weight. These holdings benefited from the substantial price premiums earlier in the year, but saw declines throughout the majority of Q2. However, they still managed to gain 13.85% and 8.93%, respectively, for the first half of 2026.

ConocoPhillips (COP), representing 6.54% of the fund, rose 11.06%, as oil supply disruptions in the Middle East allowed the company to collect price premiums from upstream North American operations. Overshadowing the other, smaller midstream companies with its 5.04% portfolio allocation, the Williams Companies (WMB) saw a return of 23.67% due to rising natural gas volumes, pipeline expansions, and increasing electricity demand from AI data centers.

Looking downstream, Valero Energy (VLO), with a 4.71% weight, saw a significant 59.53% gain. When geopolitical tensions in the Middle East disrupted global refining, Valero was still able to operate its refineries in the Gulf Coast, allowing the firm to export finished fuels at heavily inflated price premiums. As tensions eased in Q2, Valero’s crack spread benefited from the sharp price decline in raw oil, allowing the firm to maintain strong performance going into the second half of the year.

Data Centers Drive Industrial Gains

The performance in industrials, as represented by XLI, was fueled by increasing data center construction and high commodity prices, along with steady policy-driven expenditures into aerospace and defense.

XLI’s top holding with a 8.37% portfolio allocation, Caterpillar (CAT), benefited from the AI data center buildout as well as global mining companies upgrading their equipment in response to higher commodity prices. A leading equipment manufacturer, CAT returned 84.37%. Similarly, GE Verona (GEV) sits at a 5.21% weight and saw gains of 77.69%, attributed to the provision of the electricity hardware needed to construct AI data center projects.

At a 6.86% portfolio weight, GE Aerospace (GE) rose 20.66%, as the company captured high margins from jet service and repairs.+ RTX Corporation+ (RTX), at a 4.44% weight in the fund, and Boeing (BA) at 2.98% have lagged behind the broader market in 2026, yielding 3.40% and -0.77% returns, respectively.

For more news, information, and analysis, visit our Sector Investing Content Hub.