Last week, I published an update on the crypto ETF landscape, but one area worth revisiting is crypto equities—particularly Bitcoin miners. For many investors, miners can seem too niche, too volatile, or simply redundant now that spot Bitcoin ETFs exist. But that view misses how much the space has evolved. Bitcoin miners were once primarily seen as high-beta proxies for Bitcoin, especially before spot Bitcoin ETFs made direct exposure easier. Today, they offer an equity-based way to access the digital asset ecosystem, with growing exposure to artificial intelligence (AI) infrastructure, data centers, and high-performance computing (HPC). That helps explain why Bitcoin miner ETFs have recently outperformed spot Bitcoin ETFs, even as flows into the category remain relatively muted.

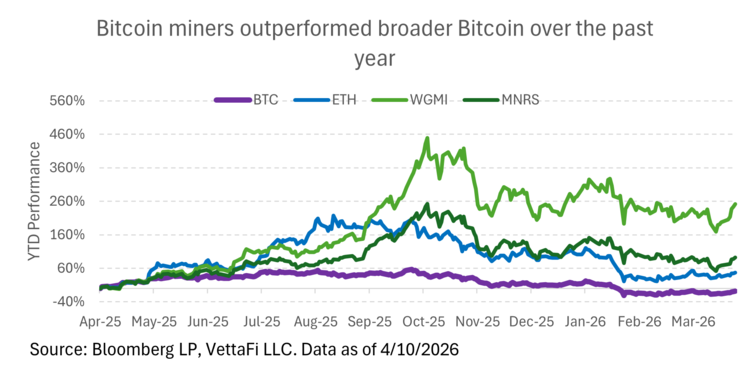

Bitcoin miner performance surprisingly resilient

Bitcoin miners had a difficult 4Q25. Bitcoin itself dropped around 30% from its early October high to late December levels, but miners were hit even harder as their underlying economics deteriorated alongside the price decline. Lower Bitcoin prices in addition to higher network competition weighed on profitability, making 4Q one of the most challenging quarters for the group.

1Q26, however, became more interesting. While mining fundamentals remained under pressure, miner equities traded on more than just Bitcoin prices and near-term margins. Some stocks held up better than Bitcoin as investors increasingly rewarded companies with exposure to AI and high-performance computing, highlighting how quickly the market is starting to view certain miners as broader digital infrastructure plays.

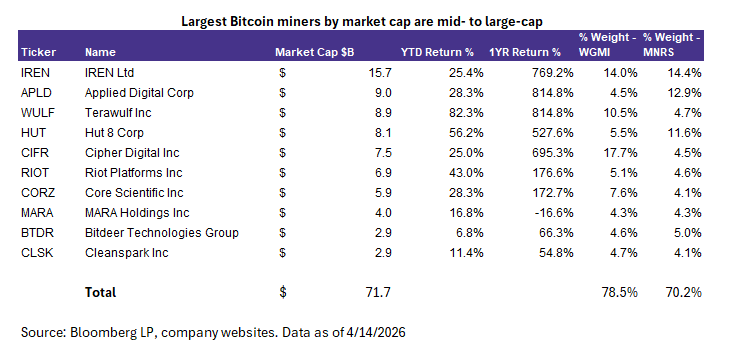

Bitcoin miners are no longer small, niche stocks

Some of the largest Bitcoin miners are listed below, and this group is not as niche as it may seem. Public Bitcoin-mining stocks now represent roughly a $70 billion market cap universe, with names like IREN Ltd (IREN) exceeding $15 billion on their own. As mentioned above, many companies are increasingly using their power access and data center footprints to pursue AI and high-performance computing, turning themselves into broader digital infrastructure stories. As the space adapts rapidly to the volatility of Bitcoin prices, market caps are growing along with valuation multiples and investor sentiment.

While a slow transition, it is already showing up in reported results. In 4Q 2025, Core Scientific (CORZ) generated roughly 44% of revenue from “colocation” or data center services (up from 18% in 3Q), while TeraWulf (WULF) derived about 27% of its 4Q revenue from high-performance computing leasing (up from 14% in 3Q). Even companies that remain primarily Bitcoin miners, such as IREN, derived 9.4% of its revenue from AI cloud services revenue in its most recent quarter (up from 3% in the previous quarter).

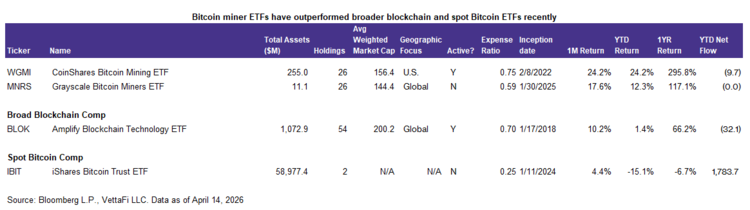

Bitcoin Miner ETFs: few pure-play options

While there are several blockchain/crypto equity ETFs, there are only a couple of pure-play Bitcoin mining ETFs left after some earlier closures.

The CoinShares Bitcoin Mining ETF (WGMI ) is the oldest and largest Bitcoin mining ETF, with almost $200 million in assets. The ETF is actively managed. It invests at least 80% of its net assets in companies that derive 50% or more of their revenue or profits from Bitcoin mining operations (or from providing specialized chips, hardware, software, and other services to miners). Because it is actively managed, it has more flexibility, not just in holdings, but also weightings.

WGMI has around 18% of its weight in Cipher Digital (CIFR), which is up 25% year-to-date. The remaining top five include: IREN, Terawulf, Core Scientific, and HUT 8 Corp (HUT), which are all up from around 30-80% YTD. As of April 14, WGMI was up 24% YTD and up almost 300% in the past year.

The Grayscale Bitcoin Miners ETF (MNRS ) launched in January 2025 and currently sits at around $10 million in assets. MNRS is passively managed and rules-based, tracking the Indxx Bitcoin Miners Index. The index prioritizes companies that generate at least 50% of revenue from Bitcoin mining. These are weighted based on free float market capitalization, with a single security cap of 15% applied to any pure-play stocks. The total weight of non-pure-play companies is limited to only 15% total. This keeps the index (and ETF) from becoming too over-concentrated, while maintaining a fair representation of the crypto mining industry.

Its top five names are around 50% of the ETF’s weight, led by IREN, Applied Digital Corp (APLD), Hut 8, Bitdeer Technologies Group (BTDR), and Terawulf. It holds only one GICS-classified financials name—+Block Inc+ (XYZ) —and one GICS-classified consumer discretionary name—+Cango Inc+ (CANG). As of April 14, WGMI was up 12% YTD and up almost 120% in the past year. MNRS has a slightly lower fee than WGMI (59 basis points vs. 75 basis points).

Many other crypto equity ETFs also have significant weight in Bitcoin miners

Blockchain ETFs can also provide significant exposure to crypto mining companies despite having a broader focus. For instance, top holdings of the Amplify Blockchain Technology ETF (BLOK ) are mostly miners, except for Galaxy Digital (GLXY), Robinhood Markets (HOOD), and Coinbase Global (COIN). Performance of many of these crypto financial companies may be better or worse than Bitcoin miners due to varying drivers, which leads to a large gap in performance with pure-play mining ETFs.

One advantage of broader blockchain ETFs, however, is flexibility. They can potentially add other types of crypto-related firms as they come to market. Because the industry is evolving, new companies will likely emerge and go public over the next few years. A few companies that have recently launched within the past few years are: Bullish (BLSH), Circle (CRCL), and Gemini Space Station (GEMI).

In contrast, certain crypto equity ETFs may also target more specific themes besides mining. Stablecoins and tokenization are a good example of this. At the end of 2025, Amplify launched the Amplify Stablecoin Technology ETF (STBQ) and the Amplify Tokenization Technology (TKNQ), which are both heavily focused on financial equities that issue stablecoins or are active in tokenization efforts, in addition to certain crypto assets like Ethereum, Solana, XRP, and Chainlink ETFs. These ETFs are not focused on miners, but show a different slice of the digital asset universe beyond broad crypto equity exposure. Read more here.

For more news, information, and analysis, visit VettaFi | ETFDB.

VettaFi LLC (“VettaFi”) is the index provider for BLOK, for which it receives an index licensing fee. However, BLOK is not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of BLOK.