Summary

- Midstream/MLPs have been generating significant free cash flow (FCF) in recent years, with excess cash flow fueling shareholder returns through growing dividends and share repurchases.

- FCF yields for energy infrastructure companies have been high relative to the overall energy sector and the broader stock market.

- Given fee-based business models, energy infrastructure companies are able to generate free cash flow indepdendent of oil and gas prices.

Free cash flow (FCF) generation has continued to be a key theme for midstream/MLPs in recent years, with excess cash flow directed initially towards debt reduction and increasingly towards shareholder returns. Compelling FCF yields enhance the midstream investment case, and companies should be positioned to generate FCF for years to come, which should in turn support dividend growth and buybacks. Today’s note looks at midstream/MLP FCF yields, how midstream’s FCF stands out against the broader energy sector, and the durability of this tailwind.

Midstream/MLPs: FCF Powerhouses

From around 2010 until 2020, oil and gas production in the US was growing significantly and required heavy investment in energy infrastructure like pipelines and processing facilities. New export facilities were also needed to connect growing US supply with global demand. As a result, midstream/MLP capital spending soared during that period, peaking around 2018/2019 (read more). Capex was already declining in 2020 before the pandemic caused a further slowdown in production growth and capital investments. Today, oil and gas production growth in the US has moderated and requires less aggressive investment in energy infrastructure (read more).

With projects started before the pandemic generating cash flows and lowered capital expenditures, midstream/MLPs have been generating excess cash flow. Initially, these incremental cash flows were used to rein in debt and strengthen balance sheets. With that box checked, companies were in a position to return excess cash to investors primarily through growing dividends, but also with opportunistic buybacks.

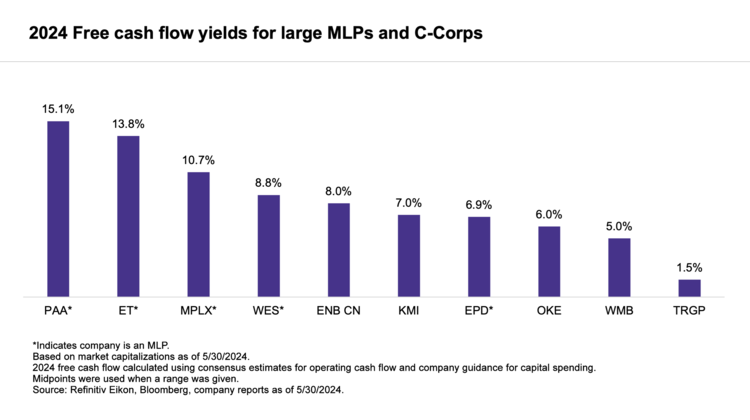

Large midstream corporations and MLPs are expected to generate billions of dollars in free cash flow this year. Even with generous dividends, companies are expected to have excess cash, which enhances financial flexibility. The chart below shows FCF yields for large-cap midstream corporations and MLPs, putting the billions of dollars of FCF into perspective. This analysis uses consensus estimates for 2024 operating cash flow from Refinitiv Eikon and Bloomberg, while 2024 capital expenditures are based on company guidance. The data does not include spending on acquisitions, and bolt-on asset-level deals have been fairly common. As shown in the chart, MLPs have the highest FCF yields of the companies shown below.

Importantly, midstream FCF yields compare favorably to the broader energy sector and the S&P 500. Per Bloomberg, the trailing 12-month FCF yield for the Alerian MLP Infrastructure Index (AMZI) as of June 6, 2024 was 10.6% and was 8.4% for the broader Alerian Midstream Energy Index (AMNA). For comparison, the TTM FCF yield for the S&P 500 was 3.1%, and for the broad Energy Select Sector Index (IXE) the TTM FCF yield was 7.0%.

Balancing Capital Discipline and Growth

While growth capital spending hasn’t neared pre-pandemic levels, midstream/MLPs have still made strategic investments in growth areas, particularly around natural gas and natural gas liquids (NGLs). Companies have generally been allocating growth capital to smaller projects, including the expansion or optimization of current assets. There are still opportunities for new pipelines, but with more moderate production growth, there are fewer major pipeline projects in the works today than there were prior to the pandemic. Midstream has transitioned from a period of aggressive growth to more measured growth. As a result, company guidance for 2024 adjusted EBITDA generally points to modest year-over-year growth (read more).

Stability of Midstream/MLP Free Cash Flow

The energy sector has broadly focused on FCF in recent years, and energy boasts notably higher FCF yields than the broader market as mentioned above. Within the energy secor, midstream stands out for FCF that does not depend on commodity price levels. Recall, midstream companies are providing services for fees under long-term contracts that often have inflation adjustments built into them. This results in more stable cash flows and stable free cash flow. Other energy subsectors will typically see free cash flow fluctuate due to their greater exposure to commodity prices. For example, oil and gas producers generated significant FCF in 2022 when oil and natural gas prices jumped following Russia’s invasion of Ukraine, but their FCF has moderated as commodity prices retreated.

Bottom Line:

The energy infrastructure space has seen strong free cash flow generation in recent years, which has allowed for generous shareholder returns through growing dividends and buybacks. Looking ahead, FCF generation is expected to continue providing tailwinds as companies see modest EBITDA growth and maintain a focus on capital discipline. Importantly, midstream FCF generation does not depend on the commodity price backdrop.

Related Research:

Midstream/MLPs: Free Cash Flow Powerhouse

Midstream Sees Strong Free Cash Flow Generation in 2023

Midstream/MLPs Raising the Bar With Lower Leverage

1Q24 Midstream/MLP Dividends: Growth Story Intact

Midstream/MLP Buybacks Rebounded in 1Q24

Permian Gas Fuels Midstream/MLP Investments

Midstream Investing in NGLs Amid Record Exports

2024 EBITDA Guidance: Midstream/MLPs See Growth

Examining MLP/Midstream Dividend and Buyback Yields

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMNA is the underlying index for the ETRACS Alerian Midstream Energy Index ETN (AMNA).

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, and AMNA, for which it receives an index licensing fee. However, AMLP, MLPB, and AMNA, are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, MLPB, and AMNA.

For more news, information, and analysis, visit VettaFi | ETFDB.