In professional sports, certain teams have a proclivity for trading with one another. It could be due to front office familiarity, complementary trade dynamics that address the needs of both teams, or other reasons. Putting the analogy to ETFs, value and growth have been willing trade partners as of late, especially when it comes to the Magnificent Seven names. The latest Russell reconstitution is proof — though in this case, the style boxes are sharing players rather than swapping them.

Key Takeaways:

- The June annual reconstitution marked FTSE Russell’s official transition back to a semi-annual reconstitution schedule after following a single annual cadence since 1989.

- Because the Russell index model splits a stock’s market capitalization across style boxes, the shifting fundamentals of Amazon, Apple, and Microsoft caused a portion of their weights to migrate into the Russell 1000 Value Index.

- As legacy consumer-tech giants transition into mature value holdings, a new hyper-growth acronym, MANGOS, has emerged on Wall Street to redefine pure-play growth in the Russell 1000 Growth Index.

See More: Dual Commencement: The Russell Index Shift to Semi-Annual Rebalancing

June's Annual Reconstitution

June’s reconstitution wasn’t all about constituent reshuffling. As noted in a previous article, it also marked the end of the annual reconstitution schedule it followed since 1989 by reverting back to a semi-annual schedule.

For those in the capital markets tracking large-cap portfolios, the reconstitution acts as a major reality check. Shifting fundamental metrics can trigger monumental weight adjustments across billions of dollars in passive products that could alter a fund’s risk profile overnight. This includes changes in the ETFs that track Russell indexes. That said, it translates into heavy trading volume, which the Nasdaq saw on June 26, when the reconstituted indexes took effect after market close.

“Russell Reconstitution is a cornerstone event for the US equity markets, ensuring the full suite of Russell US Indexes remain precise and representative of the ever-evolving marketplace,” said Fiona Bassett, CEO of FTSE Russell. “Today’s record notional volume underscores the continued trust the investment community places in our transparent and rules-based process."

Blurred Lines: Is It Value or Growth?

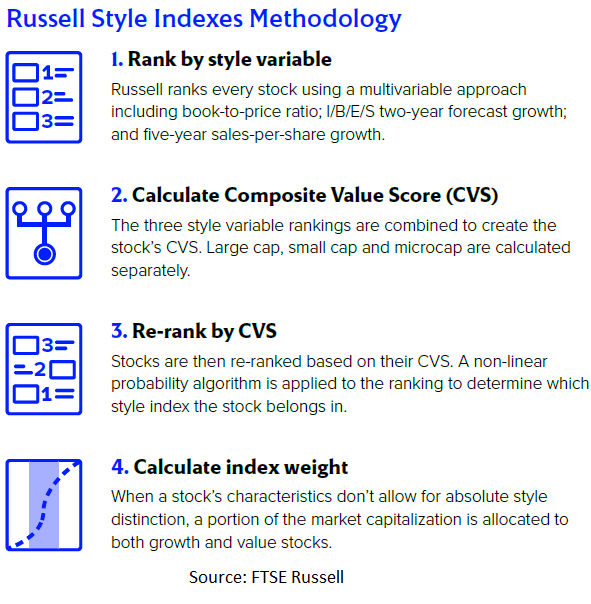

To truly grasp what changed inside Russell-based ETFs, it’s important to note that the Russell reconstitution operates on a multivariable approach that uses metrics such as book-to-price ratio in combination with growth and sales forecasts. A company isn’t simply labeled as either growth or value. Rather, Russell’s quantitative model splits a stock’s market capitalization across both factors, depending on its core valuation characteristics.

For example, when a stock’s price exceeds its fundamental book value, its growth classification score increases. Conversely, if a company exhibits a change in fundamental metrics like a higher book-to-price ratio, this increases that stock’s value profile. As noted in the Russell graphic above, certain stocks can exhibit both growth and value characteristics when they don’t fit into a singular style category.

Additionally, the June index reconstitution reflects changes in the market compared to the previous year. If a megacap tech stock exhibits greater value characteristics based on the aforementioned metrics, the Russell model automatically shifts a larger percentage of its market cap into the value basket. For investors who are used to associating certain Magnificent Seven names with growth, they will also start seeing them anchored to value.

“For investors accustomed to viewing growth and value as distinct styles, this year’s reconstitution reinforces that today’s market leaders no longer fit neatly within this framework, with many stocks no longer clearly aligned to a single style,” wrote Chris Morahan, Morgan Stanley portfolio manager and managing director.

Changes in Russell 1000 ETFs

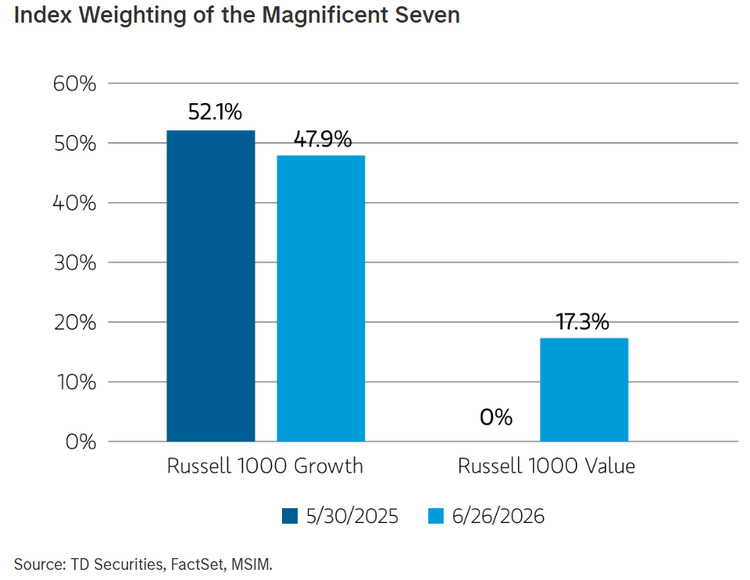

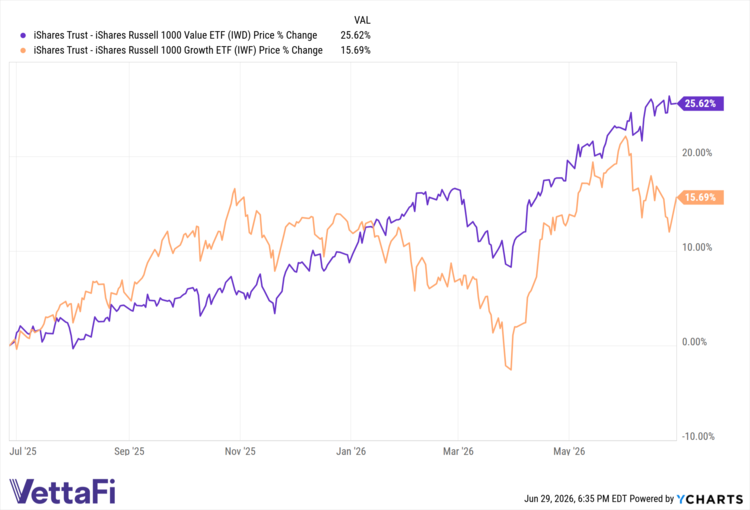

With the methodology established, the newly reconstituted Russell indexes went live on the market open June 29. In this most recent reconstitution, the style scores for Amazon, Apple, and Microsoft migrated into value territory. Because the Russell 1000 Value Index is still cap-weighted, sheer size dictates what dominates the top of the portfolio. In this case, the trio occupied the top holdings in the iShares Russell 1000 Value ETF (IWD ) as of June 26, 2026.

A peak under the hood of the iShares Russell 1000 Growth ETF (IWF ) further supports the notion that the lines between value and growth are blurring amongst the biggest names. As mentioned, the Russell 1000 Growth Index evaluates its universe through a blend of various fundamental factors. In the end, Apple and Microsoft both find themselves in the top holdings of IWF as well as IWD.

However, times are changing. Though still recognized as growth stalwarts, Amazon, Apple, and Microsoft now continue to exhibit strong fundamental characteristics like robust free cash flows and share buyback programs. In effect, this ticks the boxes for quantitative value metrics. In their place, newer, higher-multiple AI hardware plays push the boundaries of pure growth, while the trio of tech giants are pushed down the spectrum, creating an overlap between the growth and value style boxes.

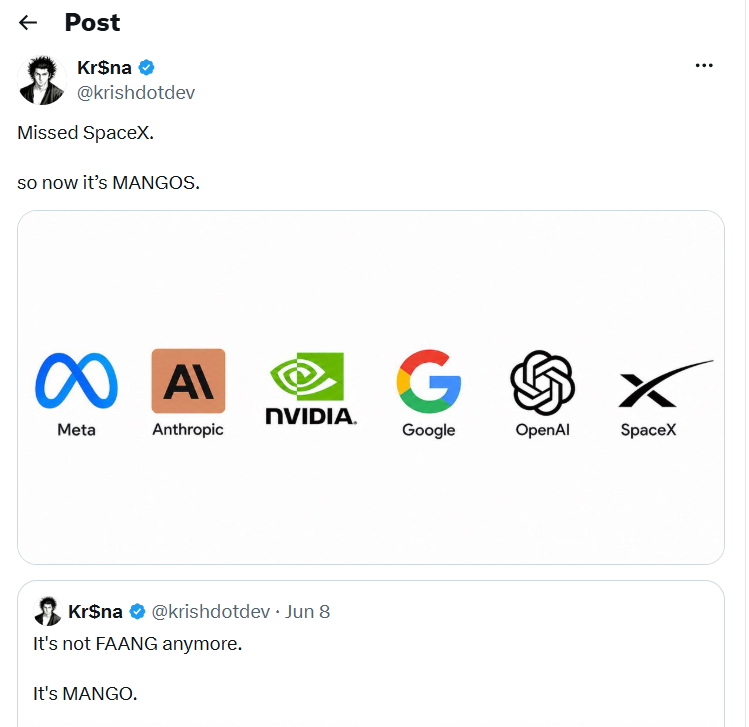

The capital markets love acronyms. Investors who grew up on the FAANG acronym have a new one to get to know, touting the latest crop of hyper-growth darlings — the MANGOS (Meta, Anthropic, Nvidia, Google, OpenAI, and SpaceX). Driven by secular AI growth, advanced infrastructure buildout to support AI, and unmatched operational scale, the MANGOS are redefining the growth factor. The MANGOS have effectively left the remaining legacy consumer-tech giants of yesteryear looking like today’s mature value plays.

Now What: Value, Growth, or Both?

The latest June reconstitution and subsequent changes in IWF and IWD serve as a reminder that passive factor investing isn’t a static strategy. For advisors building core equity models, understanding these behind-the-scenes structural changes is critical in helping to build client portfolios. However, it brings another question to the fore: Should portfolios tilt towards value or growth in the current market?

The two funds crisscrossed this year, as geopolitical tensions, persistent inflation, and other factors brought value back in vogue. However, there’s no denying the dominance that the growth factor has exhibited in the last decade. With that, ETFs don’t have to be siloed in separate style buckets. Pairing a growth fund with a value fund via an IWF-IWD combo could give investors comprehensive exposure. That combination encompasses the largest companies poised for upside, irrespective of which factor is exerting its dominance and/or despite some holdings parity in both funds.

For more news, information, and analysis, visit the Equity ETF Content Hub.