Thanks to constant innovation, there are plenty of ways for investors to craft a portfolio these days. And that doesn’t just include which asset classes to hold or what account to put them in. There’s plenty of variety in investment vehicle structures as well.

For many asset classes, the difference between choosing an exchange-traded fund (ETF) or traditional mutual funds comes with a variety of pros and cons. But the difference in both structures when it comes to bonds is striking. Making the wrong choice depending on your situation can mean a lot of headaches and problems for investors.

But how do you know which – bond ETFs or bond mutual funds – is right for you? Luckily, here at ETF Database we’ve come up with a handy guide.

Be sure check out our News section to keep track of the latest news on ETFs.

Two Very Different Structures

There are plenty of reasons why investors should be attracted to bonds and other fixed income investments. Thanks to their steady coupon payments and maturity/return of capital profiles they can be used to lower the overall volatility of a portfolio, provide much-needed income and reduce correlation to create plenty of diversification. So, adding bonds to a portfolio does make a ton of sense.

The question is, how do you add them?

Both ETFs and mutual funds offer access to hundreds, if not thousands, of individual bonds. However, the two structures could be as different as night and day. And because of the differences – ETFs with their creation/redemption mechanism and bond funds with their pooling of capital – the two operate vastly different in your portfolio.

For one thing, how you buy them is vastly different.

Bond mutual funds can only be bought/sold once per day. After the market closes, a fund company will price shares based on the fund’s net asset value (NAV). Basically, they add up all the individual bond’s values to determine its NAV. Excluding sales loads, which are quickly disappearing from most funds, mutual funds do not trade at a premium or a discount to this NAV. This makes it easy to determine precisely how much a fund’s shares will generate if sold or how much money you need to buy them. The flipside to this is that many bond funds do not release their holdings data on a daily basis and only do so quarterly or semi-annually.

This contrasts with ETFs. One of the benefits of exchange-traded funds is that, thanks to their creation/redemption profiles, ETFs can be traded throughout the day. This intraday tradability can be a blessing and a curse. Wide swings in pricing can greatly affect what an investor pays to own shares in a bond ETF.

Likewise, ETFs – especially small and illiquid ones – can fluctuate around their NAV if marketmakers cannot keep bid/ask spreads close to the portfolio’s underlying index. This “spread” is the difference between the lowest price a trader is willing to sell the ETF and the highest price a buyer is willing to pay to own it. Market makers are able to keep the spread very low on heavily traded and large ETFs. However, with smaller ETFs, this becomes much more difficult and results in NAV premiums or losses. When you trade ETFs with large spreads, it eats away at potential returns and could result in losses.

However, investors can easily find NAV and daily holdings data for ETFs.

Click here to learn about the hidden risks and costs of ETFs.

A Difference In Costs & Performance

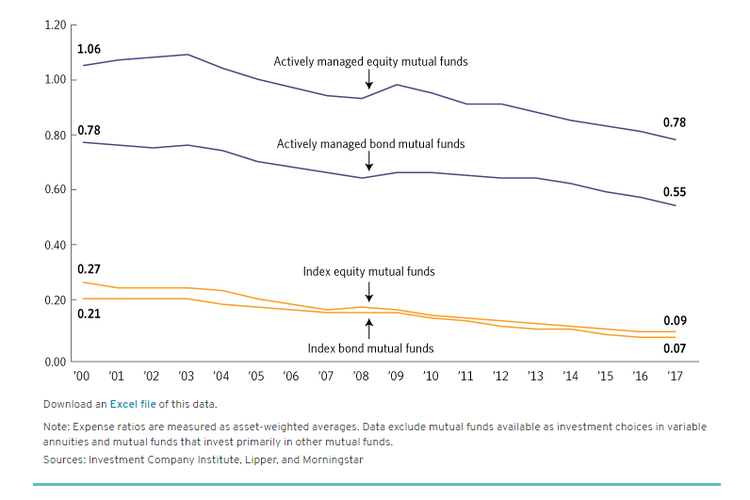

Aside from the difference in how we purchase bond ETFs and mutual funds, costs play a huge role in the debate. We all know that index funds are cheaper to own. Active management and trading costs do end up being paid for by shareholders. This shows up in the average expense ratios for the two types of investment structures.

According to the Investment Company Institute (ICI), the average actively managed bond mutual fund costs 0.55% or $55 per $10,000 invested in annual expenses. This contrasts to just a 0.09% average annual expense ratio for bond index ETFs. Just take a look at the following chart.

All things being equal, funds with lower expenses ratios will outperform those with higher ones. The kicker is that bond mutual funds and bond ETFs aren’t equal.

It seems that bonds are one area of the market that a human touch actually works. Bond funds tend to have a very high active share – that is, they don’t look like their index twins. And it turns out, this actually helps in performance. Despite being more expensive to own, bond mutual funds have typically outperformed bond index ETFs by a wide margin.

For example, take bread & butter investment grade intermediate-term bonds. According to Morningstar, mutual funds in this category have had a five-year annual return of 6.02%. This contrasts with a 4.64% total return for bond ETFs in the sector. And they aren’t alone. Nearly every category of bonds has mutual funds outperforming their ETF twins.

Another problem for bond ETFs is their higher volatility. Thanks in part to their daily tradability, their prices fluctuate with the market throughout the day. However, bond mutual fund holders miss all of those waves as they are priced at the end of the day. The Vanguard Total Bond Market Fund (VBMFX) and Vanguard Total Bond Market ETF (BND ) track exactly the same index and assets. However, the max drawdowns for the two funds are vastly different because of the pricing mechanism. During the worst period of the recession in 2008, VBMFX only lost 5.42%, while BND lost 7.74%.

This could explain why bond mutual funds still have the lion’s-share of assets over bond ETFs.

Don’t Count Out Bond ETFs

Investors shouldn’t be so quick to cast away bond ETFs, however. There are a few unique benefits to using them. For one thing, you can short ETFs. This can provide plenty of hedging opportunities for investors or allow them to participate in the downside of certain sectors. Rising rates tend to push down the prices of longer bonds or a struggling economy will hurt junk bonds. Investors can go short ETFs in these sectors to profit from their fall.

And there is no holding period for bond ETFs. That makes them ideal for short-term traders looking to put cash to work before quickly making a trade somewhere else. Many mutual funds come with short-term trading fees if held less than a certain period. Usually 30 days. Moreover, there’s no minimum investment for an ETF. You just need to buy one share. That makes them perfect for smaller or younger investors just starting out.

Use our Screener to find the right ETFs.

Which Is Right For You?

As you can see, both bond ETFs and bond mutual funds have plenty of pros and cons. And as such, they can function very differently depending on our situation. So, which is right for your portfolio? Well, if you’re strictly looking for bonds as a small allocation or looking for dirt-cheap indexing, then ETFs are great. Likewise, if your timeline is short term, then bond ETFs could be the way to go.

However, if you’re an older investor or one near or in retirement, bond mutual funds make a ton more sense. The higher allocation to fixed income necessitates taking the time and choosing active bond funds. The higher returns will make the effort worth it.

All in all, both structures offer an easy way to tap the word of fixed income. The thing is to make sure you choose the right structure for your needs.

For more ETF news and analysis, subscribe to our free newsletter or sign up for ETFdb.com Pro to get access to our ETF Guides.