The growth and widespread adoption of exchange-traded funds (ETFs) has had a profound impact on retirement planning. As the need for low-cost diversification continues to grow, ETFs provide a new model for generating sustainable retirement income.

The transition from asset accumulation to retirement planning is a critical period for most investors. Unfortunately, this transition is often riddled with complex decisions. From deciding how to allocate assets to when to tap into Social Security benefits, planning for your golden years isn’t as straightforward as it seems.

How ETFs Can Help

The $5 trillion ETF market can provide solutions to the complex challenges facing retirement planners. Put simply, the ETF universe offers funds that cover every segment of the financial system, including stocks, bonds and commodities. With ETFs, retirement planners can tailor their portfolios to suit their specific needs, circumstances and available investment capital.

Use our ETF Screener to find the right ETFs for your portfolio.

Although many investors can’t differentiate between ETFs and mutual funds, understanding this crucial difference can have a dramatic impact on their investment returns. Whereas many traditional mutual funds are actively managed, ETFs are usually passive in nature and follow an index. More aggressive strategies are available but usually require a concerted effort to identify and include them in your portfolio. Additionally, following a more active management style must conform with your risk tolerance and investment timeframe; in the case of retirement planning, these factors are usually more conservative in nature. For example, conservative investors focused on long-term growth will find funds like SPDR S&P 500 ETF (SPY ) and iShares MSCI Core Emerging Market ETF (IEMG ) highly effective.

Actively managed funds are costlier than those that simply track an index or other performance indicators. This means mutual funds are costlier in the long run. Often, the returns do not justify the added cost when compared with low-cost ETFs. Case in point: the average expense ratio for actively managed traditional mutual funds is 1.09%, according to data provider Morningstar. For passive index funds, the expense ratio is a paltry 0.57%.

Another crucial difference is in how mutual funds and ETFs are traded. Traditional mutual funds can only be bought and sold once daily – that is, after the market closes at 4 p.m. ET. ETFs can be traded like stocks at any point during the day. However, it’s important to note that ETFs and stocks differ vastly in structure (in the case of ETFs, you are investing in a specific segment of the market, which often means gaining exposure to several stocks versus just one).

In terms of cost-benefit analysis, it’s clear that ETFs have the following benefits: low-cost, ease of diversification, liquidity and lower volatility than individual stocks.

In terms of disadvantages, ETFs face: intraday pricing changes, which are pointless for long-term investors, potentially larger bid-ask spreads, and limits on the types of stocks/indexes being tracked.

To learn more about ETF Investing Strategies, click here.

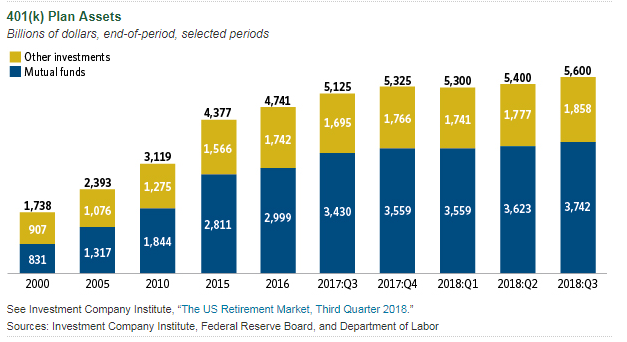

ETF Adoption Among Retirement Planners

As of Q3 2018, roughly two-thirds (66%) of total 401(k) holdings were devoted to mutual funds, according to the Investment Company Institute. However, the sizes of other investments have grown considerably in recent years, which suggests retirement planners are venturing beyond mutual funds exclusively.

The size and growth rate of the ETF market is also a clear indication that retirement planners are making greater use of passive fund strategies. According to Ernst & Young, the total value of ETFs under management is expected to grow a whopping 40% to $7.6 trillion by 2020. According to the researchers, one of the prevailing themes is the “shift to self-directed retirement saving,” which makes ETFs more attractive.

According to Matt Fellowes, founder and CEO of United Income, today’s retirees have a 42% greater chance of their money lasting through retirement if they used a less-expensive investment vehicle that also helped them lower their taxes and measure their risk profile accurately. ETFs certainly fit that bill.

Be sure to check our News section to keep track of the latest news on ETFs.

The Bottom Line

ETFs are permeating every segment of society, including early- and late-stage retirement planners. It’s important to weigh the benefits and drawbacks of ETFs versus traditional mutual funds to develop an optimal strategy for retirement planning.

In this article, we introduced you to the basics of what you should look for when comparing the two asset classes.

For more ETF news and analysis, subscribe to our free newsletter or sign up for ETFdb Pro to get access to our ETF Guides.