Commodity exchange-traded products (ETPs) have raised some eyebrows over the years because their returns don’t always line up with the respective spot prices they are designed to track.

Below, ETF Database takes a look at the various types of exchange-traded commodity investment vehicles and why their returns don’t always line up with spot prices as one might expect.

The Basics Behind Commodity ETPs

The Appeal

Commodity ETPs have opened up the doors to an asset class historically respected for its diversification and inflation-fighting benefits among investors. Indeed, traders too have embraced these vehicles for their easy access to a variety of once hard-to-reach corners of the market.

How They Work

When all is said and done, these investment vehicles are able to accomplish all of the above feats in one of two ways. First, they may do so by providing futures-based exposure to the said natural resource. For example, a futures-based oil fund would consist of crude oil futures contracts; in other words, a futures-based ETP takes care of the futures-related nuances and upkeep so you don’t have to.

These types of commodity ETPs do bear a few noteworthy nuances which are discussed in greater detail below.

Second, these investment vehicles may actually buy and hold the said resource, thereby providing physically backed exposure. Obviously, this type of approach clearly does not lend itself to most of the commodities market, as many resources are perishable and just outright difficult (and expensive) to store. The thought of a physically backed energy (or grains) ETF that hoards barrels of crude oil (or bushels of corn) in existence is laughable.

With that said, while physically backed exposure may be out of the question for most commodities, this strategy is highly sought after in the case of precious metals. The key benefit of this approach is that these products tend to exhibit near-perfect correlation with spot prices. Again, an inherent downfall here is the fact that this approach does not lend itself to practically any other commodity family.

Nuances to Consider

There are number of reasons why futures-based commodity ETPs will not move in perfect unison with spot prices, namely:

- Outside of the ETF scope, commodity futures prices are by nature not exactly the same as spot because they are just contracts and thereby instruments themselves after all. In other words, without even getting into the complexities of managing a futures-based fund, futures are inherently going to lack perfect correlation with spot. Some of the variables that affect futures prices include interest rates, carrying costs, income yield and storage costs.

- Constructing a portfolio out of futures contracts, in lieu of obtaining physically backed exposure, leaves the fund susceptible to four factors:

- Changes in the futures contracts prices themselves, be it gold or oil contracts fluctuating in value.

- Uninvested cash in the portfolio.

- The cost, known as “roll yield”, that is incurred when front-month contracts are swapped for longer-dated ones to keep the portfolio’s exposure in line with spot as best as possible.

- Contango, which refers to the situation when longer-dated futures contracts are more expensive than those that are closest to expiration. This means that ETPs which hold only front-month futures will be forced to sell low and buy high come portfolio rebalancing time.

For these reasons, investors simply cannot expect futures-based commodity ETPs to perfectly correlate with spot prices, and especially so over the long haul.

There are some “remedies” however, including the proliferation of so-called third-generation commodity products, made popular by firms like Teucrium, which are built to reduce the negative impact of contango by taking a more balanced/proactive approach when it comes to selecting the contracts they hold.

Commodity ETPs vs. Spot Price Returns

Let’s consider some real-life examples of how well futures and physically backed products track commodity spot prices.

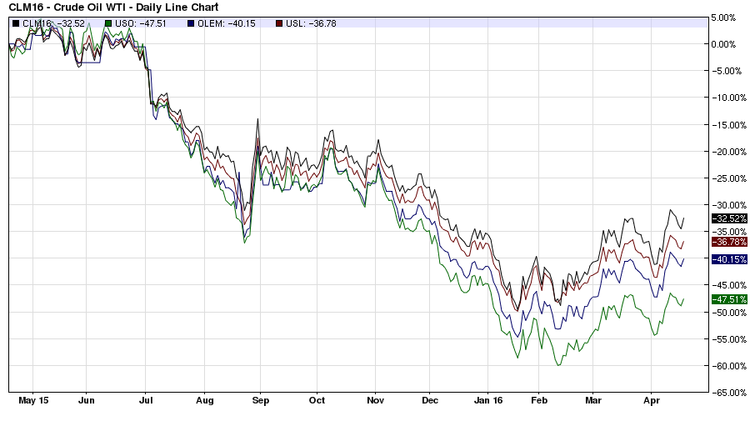

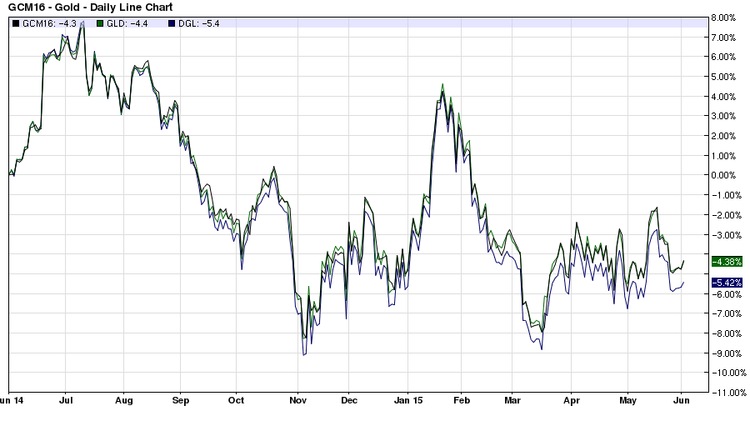

One-year daily returns as of 4/19/2016.

Oil ETPs

The worst tracker has been the front-month-based fund (USO ), whereas the best tracker has been (USL ), which is based on the average price of 12 futures contracts on crude. Stuck in the middle, albeit much closer to the best tracker, is (OLEM ), which may roll its exposure into contracts with varying expiration dates in lieu of a pre-determined roll schedule.

The key takeaway here is that front-month-based products may come with more nuances than others, and because commodity ETPs are already imperfect tracking tools to begin with, this leaves even more room for divergence from spot prices.

Gold ETPs

The best tracker in this case is the physically backed (GLD ), which has offered more precise exposure to gold prices than its ETN, futures-based brethren (DGL ). While the divergence in this case is not as drastic as the oil comparison above, this is still notable, and especially so for longer-term investors.

Ways to Play

Investors can pick their commodity ETP based on exposure type:

Alternatively, they can also navigate the investable commodity ETP universe by resource type:

The Bottom Line

Commodity ETPs can be utilized in a variety of ways, ranging from portfolio building blocks to tactical trading instruments. Investors should, however, be well aware of the inherent nuances, and by many measures, drawbacks, associated with some of the futures-based products on the market. Be sure to do your homework on any product, be it front- or multi-month contract-based, futures or physically backed, before pulling the trigger.

Follow me @SBojinov