This section of the Energy Infrastructure University is intended for people who have worked through EI 101 or people who already have a solid understanding of the midstream space. Our 201 section is designed to provide readers with a deeper understanding of the nuances behind the energy infrastructure business model and expand their knowledge beyond the basics.

Shale Revolution

For many decades, producers drilled for oil and gas in rock formations such as carbonates, sandstones, and siltstones. These formations, known as conventional formations, have multiple porous zones that allow the oil and gas to flow naturally through the rock. This ability of rocks to allow fluids to flow is known as permeability. Conventional formations have higher permeability than unconventional formations like shale rock. Vertical drilling, which involves drilling straight into the ground, worked for many years on conventional formations because once the drill bit hit a particular area, the high permeability would allow the hydrocarbons to be extracted easily.

Shale is a type of geological formation found in sedimentary rocks. For quite some time, the energy industry has known that oil and gas existed in shale. But because shale rock is not as permeable, using old techniques with vertical drilling did not make it economically feasible to recover resources because it would only capture a limited amount. Three technologies together truly changed the game for extracting shale resources: 3D seismic imaging, horizontal drilling, and hydraulic fracturing.

In short, 3D seismic drilling tells producers where to drill, horizontal drilling increases the amount of area drilled, and hydraulic fracturing solves the issue of low permeability.

Here’s a more in-depth look at each.

• 3D seismic technology: uses acoustic energy, vibrations, and reflected signals to determine the location and density of rock formations. Think of it like an underground map.

• Horizontal drilling: allows the operator to drill a well, and then manipulate the drill bit underground to make a 90-degree turn and cover a much larger area. Multiple (up to 20 or more) horizontal wells can be drilled from a single drill pad, lowering drilling costs, increasing efficiency, and minimizing the impact to the environment. After the well is drilled and lined with casing, it is ready for hydraulic fracturing.

• Hydraulic fracturing: describes the process in which a mixture of water, sand, and other chemicals is pumped into a well at a very high pressure to break up shale rock. The highly pressurized mixture lets a driller open all those tiny pockets. The water is then removed, and the remaining sand props open the rock, allowing hydrocarbons to flow freely to the surface.

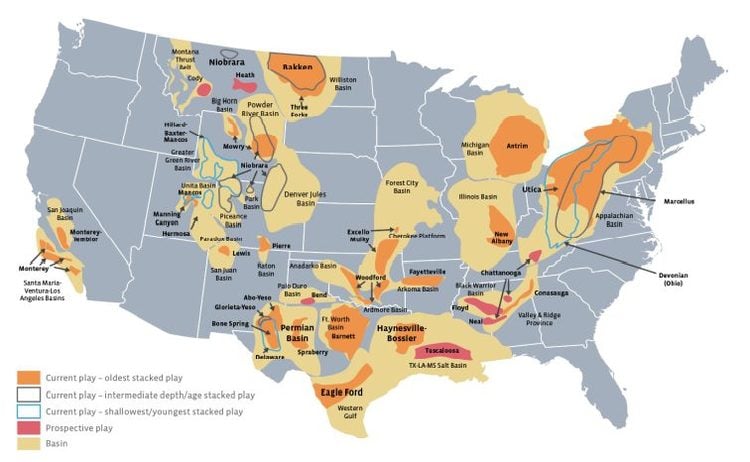

The map below shows some of the major natural gas, crude oil, and NGL plays in the U.S. There are shale plays in Canada as well, such as the Montney Shale in Alberta and British Columbia. Energy infrastructure companies built the pipelines, terminals, storage facilities, and processing plants to get production from these regions to end markets or the coast for export in usable form.

Energy Infrastructure Business Models

In Energy Infrastructure 101, we examined the pipeline business. Pipelines are perhaps the most familiar of the assets that energy infrastructure companies operate, but these companies are also involved in a much larger swath of the energy value chain.

Gathering & Processing – Before hydrocarbons enter a large pipeline, they need to be gathered and, in the case of natural gas, processed. Gathering involves connecting wells to major pipelines through a series of small diameter pipelines. Gathering pipelines transport either crude oil or natural gas from the wellhead to hubs. Processing is required for natural gas and involves the removal of potential contaminants and separation of NGLs so the gas can meet purity standards for pipeline transmission.

Gathering and processing companies focus on obtaining fee-based revenues by charging upstream companies a set fee for every million British Thermal Unit (MMBtu) of natural gas or barrel of oil that is gathered or processed. The contract often includes a minimum volume commitment or acreage dedication, which helps provide cash flow stability. Occasionally, some companies will have different compensation structures, which may include payment in the form of keep-whole contracts. This allows them to keep the extracted NGLs and sell them to third parties at market prices. Another contract structure is percent of proceeds (POP), in which the processor is paid by retaining a percentage of any processed natural gas or NGLs. As keep-whole and POP contract structures expose gathering and processing companies to volatility in commodity prices, the vast majority of companies have moved (or attempted to move) to a purely fee-based revenue structure.

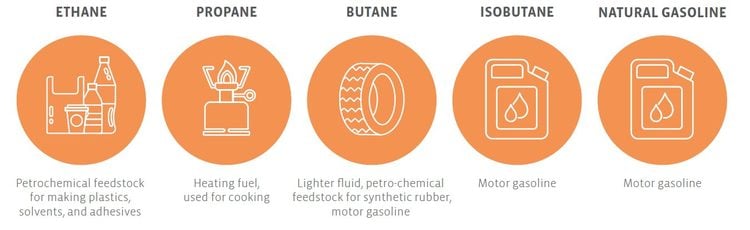

Fractionation – At a fractionation facility, NGLs are separated into their individual usable components of ethane, propane, butane, isobutane, and natural gasoline. Ethane is primarily used as a feedstock, or input, into petrochemical plants to make ethylene, which is used to make plastics and other chemical products such as solvents and adhesives. Propane by itself can be used as a heating fuel or used as a feedstock to make propylene, which can be used in the manufacturing of textiles or plastics, such as headlights, eyeglasses, foam bedding, and water bottles. In general, ethane and propane make up the bulk of the NGL stream, with a concentration ranging from 55% to 85%. Butane, isobutane, and natural gasoline are used to produce motor gasoline. Butane is the primary component of lighter fluid and can be used as a feedstock to make butadiene, which is used in creating synthetic rubber.

The majority of fractionation is done on a fee-for-service basis. However, the amount of fees earned depends on the amount of volumes fractionated, which in turn depends on something called the frac spread. Essentially, the frac spread is a measure of the reverse of the adage “the whole is greater than the sum of its parts.” With NGLs, the sum of the parts is worth more than the whole. Some NGLs must be removed for the natural gas stream to meet purity standards, but often they are only removed for additional profitability. The frac spread is the difference between the value of the NGLs if removed and the value of the NGLs if they are left in the natural gas stream and sold at the same price as natural gas. Ethane rejection is the industry term for when ethane prices are so low that it is better to leave ethane in the natural gas stream than extract it.

The relatively high cost of NGL handling, storage, and transportation additionally factors into the volumes of NGLs that will be fractionated. In order for the hydrocarbons to remain liquids, they must be kept under high pressure or cooled to very low temperatures. Additionally, gaseous NGLs are heavier than air and flammable, requiring increased safety measures. NGL storage typically takes place in underground caverns for these reasons, while the smaller amounts stored above ground are placed in insulated tanks and thicker steel.

Transportation – Transportation companies are the bread and butter of the sector. This fee-based business model is the most well-known and most frequently referenced, perhaps because it is one of the simplest to understand. Typically, midstream companies will enter long-term contracts with customers committing to use a certain amount of pipeline capacity. The midstream company will collect a fee per unit of hydrocarbon transported. Contract provisions such as take-or-pay agreements or minimum volume commitments allow the pipeline company to collect specified fees even if the customer does not fully use its committed capacity.

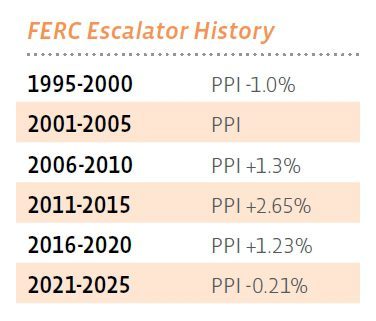

Interstate liquids pipelines are regulated by the Federal Energy Regulatory Commission (FERC), and rates are most often based on the FERC’s oil pipeline index. Every five years, the FERC sets the ceiling rate by which tariffs will be increased, with the rate based on the Producer Price Index for Finished Goods plus an adjustment. Through 2026, these FERC-regulated pipelines will increase the tariff they charge by PPI – 0.21%2 every July 1.

Interstate natural gas pipelines generate revenue by collecting a tariff for each unit of natural gas transported under long-term commitments. Customers enter contracts for capacity for these pipelines in much the same way that apartments are rented, but instead of year-long leases, interstate natural gas pipeline contracts are often for five to 20 years.

Like with a lease, customers are obligated to pay regardless of whether or not they use the space. Additional fees are charged when a customer needs to inject or withdraw hydrocarbons to meet demand spikes or oversupply. For new-build projects, the length and terms of these contracts allow the pipeline company to earn the rate of return necessary to construct the pipeline.

Transportation companies have historically avoided building speculative projects, given the capital intensity of pipelines. Instead, pipeline companies will move forward with projects once they have sufficient customer commitments.

Storage – Natural gas that is not immediately required for electricity generation or heating is stored until needed. The same is true of crude oil waiting to be refined and refined products (such as gasoline, diesel, and jet fuel) waiting to be consumed. Storage facilities operate a fee-based business model similar to rent, with contract lengths generally ranging from one to five years. Storage tanks for crude oil and refined products may also have inflation escalators.

Liquefaction – Liquefaction refers to cooling natural gas and transforming it into a liquid state so it can be shipped overseas for export. Exports of liquefied natural gas (LNG) from the U.S. have increased in recent years as LNG export capacity has increased and projects have come online.

Pipeline Permitting

Natural Gas Pipelines

According to the Natural Gas Act, companies that would like to build an interstate natural gas pipeline must obtain a “Certificate of Public Convenience and Necessity” from the Federal Energy Regulatory Commission before beginning a project. This is a multi-step process, and the timeline for this process can vary:

- Pre-Filing and Environmental Review. Pre-filing involves notifying all stakeholders of the proposed project and offering a medium for stakeholders to voice concerns related to the project. This phase also includes a study of the potential project site. This process begins several months before the application for the actual certificate is filed.

- Application for FERC Certificate. This is the beginning of the formal process. Applicants must provide a great deal of data on the project, such as construction plans, route maps, schedules, and more.

- Environmental Review. An official study is carried out on how the project will impact the environment. The public is then given an opportunity to comment on the results of the study. After this, the FERC will consider the comments and issue formal approval or denial of the project.

Petroleum Pipelines

The permitting of oil pipelines is not subject to FERC regulation. While companies constructing oil pipelines are required to obtain federal permits such as those described under the Clean Water and Clean Air Acts, state approvals are the only governmental authorizations required for oil pipeline construction projects to move forward.

This may initially seem like an advantage for oil pipelines. Many would agree it is easier to acquire permits to build a pipeline from Oklahoma to Texas than from Pennsylvania to New York, for example. However, dealing with landowner issues in multiple states is not necessarily easy. If a landowner does not agree to the path of a pipeline and eminent domain authority does not exist in that landowner’s state, the oil pipeline could be forced to take a more expensive alternative route. For natural gas pipelines, FERC approval includes federal eminent domain—a primary advantage of building a natural gas pipeline over building an oil pipeline.

Pipeline Regulation

In the United States, interstate liquids pipelines are regulated by the Federal Energy Regulatory Commission. Unlike the antagonistic relationship most utilities have with their regulators regarding pricing, the FERC focuses on the safe and efficient transportation of energy throughout America. The FERC sets the ceiling rate for tariff increases on all interstate liquids pipelines following FERC’s oil pipeline index. Through June 2026, the index will be based on PPI – 0.21% The FERC reviews the PPI escalator every five years, and the historical values are shown below for context.

For interstate natural gas pipelines, the FERC enforces the Natural Gas Act, which mandates that the rates charged must be “"just and reasonable":https://www.ferc.gov/.” This is determined by calculating the pipeline company’s cost of service, plus a return on its investment.

Intrastate pipelines are regulated by the states themselves. The most famous state regulatory agency is The Railroad Commission of Texas (a legacy name). State regulatory agencies work with pipeline companies to maintain standards of safety and maintenance.

Canada

Headquartered in Calgary, Alberta, the Canada Energy Regulator (CER) regulates the interprovincial oil, natural gas, and utilities industries in Canada. It does not create energy policy; it merely regulates construction, operation, and tariffs, and includes the energy-related functions that the EPA would provide in the United States.

Similar to the FERC, the CER regulates pipeline tariffs to ensure that the rates are just and reasonable. The CER establishes tariffs in a way to allow companies to cover their costs and earn a reasonable return for their investors. Canadian pipeline companies may only charge a toll that has first been approved by the CER. This process typically includes review and negotiation of the terms and conditions of pipeline access and the responsibilities of both parties. Tariffs are often based on cost-of-service regulation. As a result, lower throughput can lead to greater tariffs as costs are shared by fewer shippers, or an expansion of a pipeline could lead to higher or lower tariffs depending on the change to throughput and revenue.

Aside from cost-of-service regulation, pipelines may also operate under negotiated settlements with the pipeline company and its customers reaching an agreement on tariffs and operational matters, which is then approved by the CER. Most of the major CER-regulated pipelines have operated under negotiated settlements in recent years.

Valuation

The most common valuation metrics for midstream companies are enterprise value to EBITDA (EV/EBITDA), free cash flow yield, and the dividend discount model. Valuation metrics for MLPs have historically been based on yield or distributable cash flow, but valuation methods for MLPs are evolving as the MLP business model evolves (read more). Price-to-earnings ratios may also be used to value midstream companies, but P/E ratios can sometimes be distorted by the high depreciation expense for energy infrastructure companies, which may make earnings appear minimal or negative when in reality their cash flows remain stable and growing.