The incredible breadth of MLP investment product selection is due to the wide variety of aspirations and risk tolerances investors have for their MLP allocation. This section is intended to help investors distinguish between and sort through the various investment products.

Energy Infrastructure in Portfolios

Now that you’ve read about the business models, risks, and fundamentals for MLPs, perhaps you have decided that an investment in MLPs is right for you and your portfolio. Now what? The first thing to do is decide how much of your portfolio to allocate to MLPs.

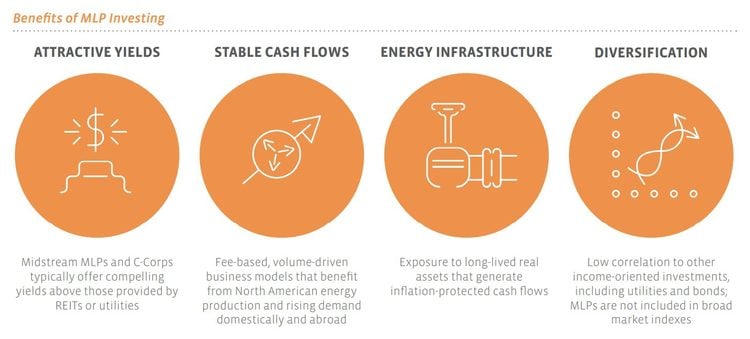

Many investors use MLPs in their equity income sleeve, their real asset sleeve, or their energy equity sleeve. In Alerian’s conversations with investors over the years, we’ve seen a typical allocation of 3%-6%; although depending on the portfolio’s objective, we’ve also seen upwards of 10%. It’s important to keep in mind that investments in MLPs come with risks, as do all equity investments.

Buying Individual MLPs

One of the lines that we repeat over and over is, “For a U.S. taxable investor comfortable filing K-1s and state taxes and building a diversified portfolio, s/he will always be better off buying individual MLPs directly.” “Always” isn’t a word financial folks use very often. To break that down, we mean an investor who is taxed in the U.S. and is investing in a taxable account (not an IRA, 401(k), or other tax advantaged vehicle). Also, that investor is willing to receive and file K-1s (as opposed to 1099s) as well as filing any associated state taxes. Or, the investor is willing to pay an accountant to do so on her behalf. Also, the investor is willing to do the work of researching and choosing individual MLPs and taking on the associated risks with security selection and portfolio construction. If all those constraints are not a problem, the most tax-efficient way to access the asset class (and incidentally, pay the lowest fees) is to buy MLPs directly.

MLPs can be more tax-efficient investments than many other stocks due to their features associated with distributions. From an estate planning perspective, if units are passed along to heirs, upon death of the unitholder, the basis is “stepped up” to the fair market value of units on the date of transfer, thereby eliminating a taxable liability associated with the reduction of the original unitholder’s cost basis.

For investors who are willing to research individual securities and who are comfortable with single-security risk, direct investment in individual MLPs may be an attractive option.

Of course, once investors have decided to buy individual securities, there is the question of which one(s) to buy. As an indexing and market intelligence firm, our desire is to equip investors to make informed decisions about energy infrastructure and MLPs. To maintain objectivity, we do not make stock picks, and Alerian employees do not own individual MLPs or energy infrastructure corporations.

However, after years of following the space, we have these recommendations for investors looking to put together a portfolio containing MLPs.

- Management Teams – Consider the management team of the MLP. Solid management teams are those that have led the company to build new projects on time and on budget, that have been effective and efficient stewards of investor capital, and that work well together and have excellent relationships with their customers, investors, and other industry stakeholders. They do what they say they will do and have a deep bench of talent.

- Asset Footprint – MLPs that already own land and rights of way in growth areas benefit from their established position by being able to expand their position without excessive political or regulatory headwinds. Additionally, companies that own a variety of assets along the energy value chain can clip multiple coupons along the way while also realizing cost savings from integration. MLPs with basin diversity have a natural hedge against changing hydrocarbon flows.

- Capital Allocation – In recent years, the energy industry has shifted from a grow-at-all-costs mentality to being more focused on returns and the best use of capital. This holds true for energy infrastructure MLPs as well. Companies should allocate capital based on what has the best returns for investors, whether it is pursuing an attractive growth project, increasing the dividend, or repurchasing equity.

- Balance Sheets – In recent years, financial flexibility has proved to be important as companies have navigated challenging macro environments, including the temporary but severe demand destruction for oil associated with the COVID-19 pandemic. Strong balance sheets and low leverage ratios provide for a greater margin of error in challenging environments.

- Size – Larger MLPs can more easily access the capital markets and are more likely to get investment grade credit ratings, have higher trading liquidity, and reach a broader investor group. However, it also takes bigger projects, built or acquired, to move the needle for the company’s bottom line.

The Myriad of MLP Investment Products

Many investors do not fit the criteria listed above for buying individual MLPs, but thankfully, a variety of MLP access products are available to investors.

MLPs are pass-through structures that do not pay taxes at the entity level. Instead, income and deductions are passed through to the end investor. Regulated investment companies (RICs) such as closed-end funds (CEFs), mutual funds, and exchange-traded funds (ETFs) under the Investment Company Act of 1940 (collectively, “40 Act Funds”) are also pass-through structures. Under current law, 40 Act Funds seeking to retain pass-through status are prohibited from owning more than 25% of their assets in MLPs. Funds that abide by this law are called “RIC-compliant.”

There are funds that have more than 25% of their assets in MLPs; however, these funds are no longer pass-through structures and are required to pay taxes at the fund level. Functionally, this means that fund performance is reduced by the amount of taxes accrued (i.e., will be owed when positions are sold). Think of it like your employer withholding a certain portion of income taxes. In this case, the fund withholds (or accrues) a portion of the returns. Some funds will use leverage to offset some of the effect of taxes. While leverage can increase returns when performance is positive, leverage will also magnify losses when performance is negative. These funds are also able to preserve the return of capital benefit for their investors, and since they can own 100% MLPs, the proportion of income that is classified as return of capital is greater. They tend to be favored by investors seeking to maximize after-tax income.

Some funds are passively managed, where performance is linked to an index or benchmark. These funds tend to have lower fees. An actively managed fund has higher fees to account for the fact that a portfolio manager must be paid to choose individual stocks.

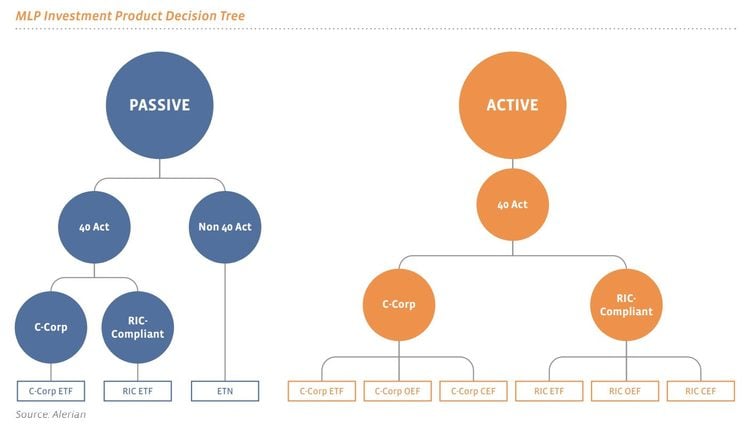

To help navigate the variety of investment products available, Alerian has provided the decision tree below.

40 Act Funds – C-Corporation taxation – 100% MLPs

A 40 Act Fund, such as a mutual fund or ETF, that owns more than 25% MLPs will be taxed as a C-Corporation. As the underlying positions increase in value, the fund will accrue a deferred tax liability (DTL) to account for taxes that will be owed should the position be sold. This DTL is assessed at the corporate tax rate of 21% plus an assumed rate attributable to state taxes. The DTL is removed from the net asset value (NAV) of the fund, meaning that if the value of the underlying portfolio rises from $100 to $110, the fund’s NAV will move from $100 to $107.90. As the position falls, the DTL will be reduced.

When the fund is in a net DTL position, the DTL effectively reduces the volatility of the underlying portfolio, assuming no leverage is employed. Some funds (typically closed-end funds) will use leverage to offset some of the effect of taxes. While leverage can increase returns when performance is positive, when performance is negative, leverage will also cause the fund to lose more money. If the fund has no DTL to unwind, it will track the underlying portfolio on a one-for-one basis. Fund distributions track the return of capital proportion of the underlying basket of securities and lower an investor’s cost basis. This allows investors to enjoy the tax deferred income associated with MLPs without the hassle of filing a K-1. Additionally, investors in 40 Act Funds with C-Corporation taxation do not need to worry about UBTI if investing in a tax-advantaged account.

Advantages:

- Owning the underlying securities

- Generally higher after-tax income due to:

- Tax character of distributions mirrors that of underlying portfolio

- Fees are taken from the NAV, preserving the yield

Disadvantages:

- DTL mutes gains when the fund is in a net DTL position

Suitability:

- Taxable investors seeking after-tax yield

40 Act Funds – RIC Compliant – Less than 25% MLPs

Funds that own less than 25% MLPs do not pay taxes at the fund level, enabling them to pass through the entire return to their investors. The return of capital benefit from owning MLPs is muted due to the limit imposed on MLP ownership. Investors interested in RIC-compliant energy infrastructure funds should research what the fund owns for the other 75%. Common positions include midstream C-Corporations, utility companies, exploration and production companies, refiners, and MLP affiliates structured as C-Corporations.

Advantages:

- Ownership of the underlying securities

- Little to no tracking error

Disadvantages:

- Generally lower yield

Suitability:

- Tax-advantaged investors

- Total return investors in a taxable account

- Comfortable with non-MLP investments

- Prefer broad exposure to energy infrastructure (corporations and MLPs)

RIC compliant 40 Act funds may be mutual funds, closed-end funds (CEFs) or ETFs.

ETFs vs Mutual Funds

ETFs trade throughout the day, whereas mutual funds price only at the end of the day. However, mutual funds always price at NAV, while ETF prices are determined by the market. ETFs may also be sold short. Typically, MLP ETFs have lower fees, ranging from around 50 basis points (bps) to 100 bps. Mutual funds fees in this category are a bit higher and range from around 70-140 bps. Mutual funds may also use up to 33% leverage.

Closed-End Funds (CEFs)

CEFs were the first 100% MLP C-Corporation, 40 Act products. Like mutual funds, they can also use up to 33% leverage. Because CEFs do not have a creation/redemption feature, pricing may stray from NAV, causing them to trade at a premium or discount. Their liquidity is also constrained by the fund itself as opposed to the underlying securities held.

Exchange-Traded Notes (ETNs)

An ETN is an unsecured debt obligation of the issuer. It is an agreement between an investor and an issuing bank under which the bank agrees to pay the investor a return specified in the issuance documents. MLP ETNs may track a basket that is 100% MLPs without accruing for DTL.

Advantages:

- Little to no tracking error as the bank agrees to pay the return

- Intraday knowledge of portfolio holdings

Disadvantages:

- Coupons are taxed at ordinary income rates

- Lower income as the expense ratio is removed from coupon payments

- Exposure to the credit risk of the underlying bank

Suitability:

- Tax-advantaged accounts such as 401(k)s or IRAs

- Total return investors in a taxable account

- Investors comfortable with the credit risk of the financial institution

Separately Managed Accounts (SMA)

An SMA is an account that is managed by a portfolio manager. Unlike owning a basket of individual MLPs and receiving multiple Schedule K-1s, an SMA consolidates everything so that the investor only receives one Schedule K-1. SMAs may generate UBTI. Once UBTI exceeds $1,000 in an account, additional taxes may be assessed.

Advantages:

- Preserves tax characteristic of the underlying investment

- Typically lower fees than publicly traded products

Disadvantages:

- May generate UBTI

- Issues a Schedule K-1

- High minimum investment

Suitability:

- Large institutions such as pensions and endowments

- Very wealthy individual investors

Active Versus Passive

Although this will vary by investor, the next thing to decide in regards to an MLP investment philosophy is active versus passive management. While this decision is germane to any sector, there are a few things unique to the midstream space. Advocates of passive investing note that over the long term and after factoring in fees, active managers are unable to consistently outperform the index to which they benchmark their performance. Advocates of active investing argue that with extensive research on individual companies, selective investing, and close monitoring of securities, a portfolio manager can generate alpha, or risk-adjusted outperformance versus a benchmark.

Individual MLP market capitalizations range from a couple hundred million dollars to tens of billions of dollars. If an active manager running a $1 billion portfolio would like to put on a 1% position in a small MLP, liquidity constraints may prevent the manager from being able to enter or exit the position in a reasonable amount of time. This may cause active managers to take large positions in the larger, more established MLPs, which are the same MLPs in a market-cap weighted index. This phenomenon is known as closet indexing.

Choosing an Active Manager

For those investors who are not comfortable choosing their own securities, but who still would like active management, Alerian recommends considering the following factors when selecting an active manager.

- History – While past performance is not an indication of future returns, it is worth looking into the track record of an active manager being considered.

- Outperformance – The entire purpose of paying for active management is to outperform the benchmark index after fees. If the active manager is not consistently outperforming the index or is underperforming the index after fees, an investor is better served by investing in a passively managed product. Outperformance in a single year may be notable but consider whether the manager has outperformed in previous years and under various market conditions.

- Differentiation – An active manager whose portfolio closely mimics an index may be engaging in closet indexing. Investors are encouraged to examine the underlying portfolio to be sure it matches the investment thesis and philosophy of the manager.

Choosing an Indexed Product

As an indexing firm, Alerian constructs and maintains energy infrastructure and MLP indexes, which it licenses to its partners for the creation of passively managed investment products. Alerian launched the first real-time MLP index in 2006, which has since become the industry standard benchmark, and Alerian continues to work hard to maintain energy infrastructure and MLP indexes that meet the most rigorous standards. With that bias in mind, Alerian recommends that investors looking for a passive investment consider the following when researching underlying indexes.

- Transparency – Passive investors should know what they are buying. The constituents of the underlying index should be available to investors, as should the methodology used to determine those constituents. If a change is to be made, that information should be public as well. Any index that lacks transparency is more like active management than a truly passive investment. A transparent portfolio allows investors to be sure the underlying portfolio matches their investment thesis. For example, not all MLP indexes are the same—some are midstream focused and include corporations, others are focused on income, and others are 100% MLPs.

- Objectivity – An index provider may be tempted to include certain energy infrastructure companies for subjective reasons: a personal investment, a relationship with the management team, or to juice returns on a stock already included in an actively managed fund. For each index, there should be rules in place to prevent personal opinions and emotions from impacting the construction and rebalancing of the index. Having a codified set of rules that is transparent and freely available to the public, as well as prohibiting index committee members from taking positions in individual energy infrastructure companies in their personal accounts, all help maintain objectivity. Additionally, indexing firms should be careful to avoid conflicts of interest with actively managed investments.