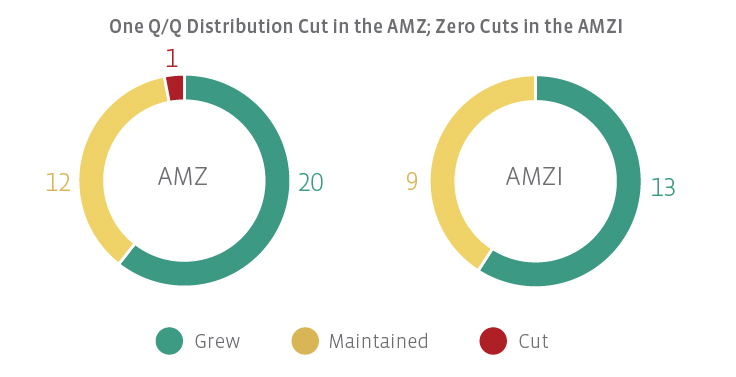

In total, there was one distribution cut for the AMZ and no cuts for the AMZI in 2Q19. AMZ constituent Sanchez Midstream Partners (SNMP), with an index weighting of only 0.02% as of the July 29, 2019, special rebalancing, announced it would suspend its distribution. Andeavor Logistics (formerly ANDX) did not declare a distribution for 2Q19 and was not included in the charts in this piece as it was removed from the Alerian Index Series in late July. Following the closure of the partnership’s merger with MPLX (MPLX), ANDX unitholders received the 2Q distribution paid by MPLX. After adjusting for the exchange ratio of 1.135 MPLX units for each ANDX unit, the transaction resulted in an implied distribution cut of 26.4% for legacy ANDX unitholders. Rattler Midstream (RTLR), which went public in late May and was recently added to the AMZ, did not declare a distribution for 2Q19 but guided to an annualized distribution of $1.00 per unit for 2019.

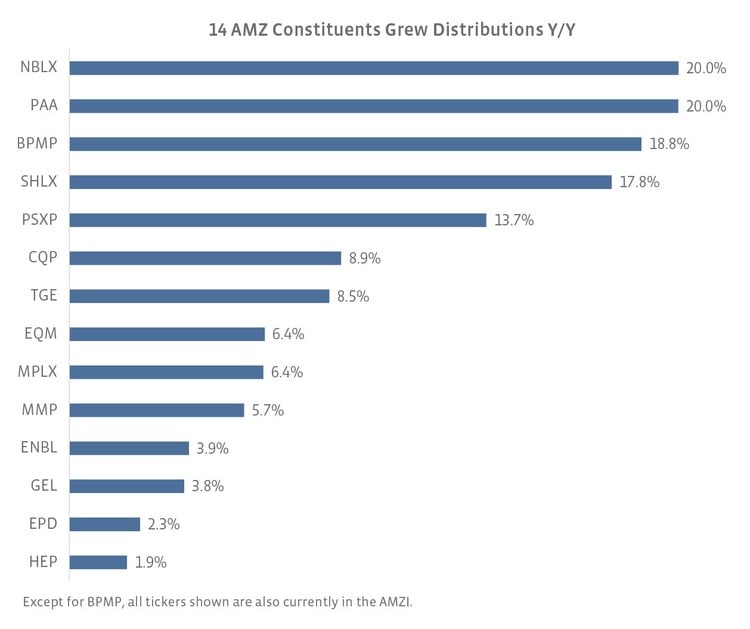

Looking at distributions more broadly, 61% of AMZ constituents grew their distributions on a quarter-over-quarter basis, and eight constituents increased their distribution by more than 3.5% sequentially. Like the AMZ, the majority of AMZI constituents (59%) grew their distribution on a quarter-over-quarter basis. Notably, Enable Midstream Partners (ENBL) announced a 3.9% distribution increase, raising its distribution for the first time since October 2015. Other large quarterly growers in the AMZI include Noble Midstream Partners (NBLX) at 4.7% and Shell Midstream Partners (SHLX) at 3.6%, both of which are dropdown MLPs that possess incentive distribution rights (IDRs) in the high splits (though SHLX’s parent has waived $50 million in IDR payments for 2019).

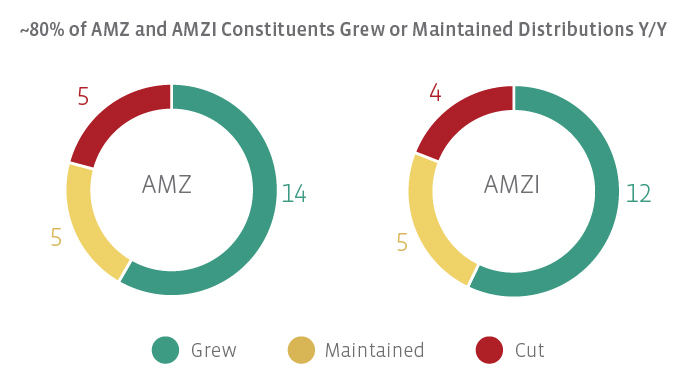

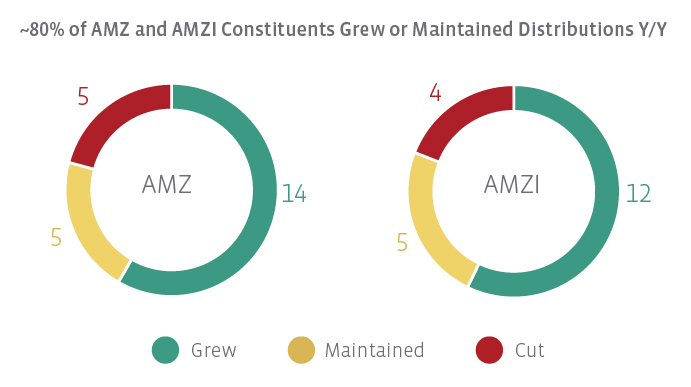

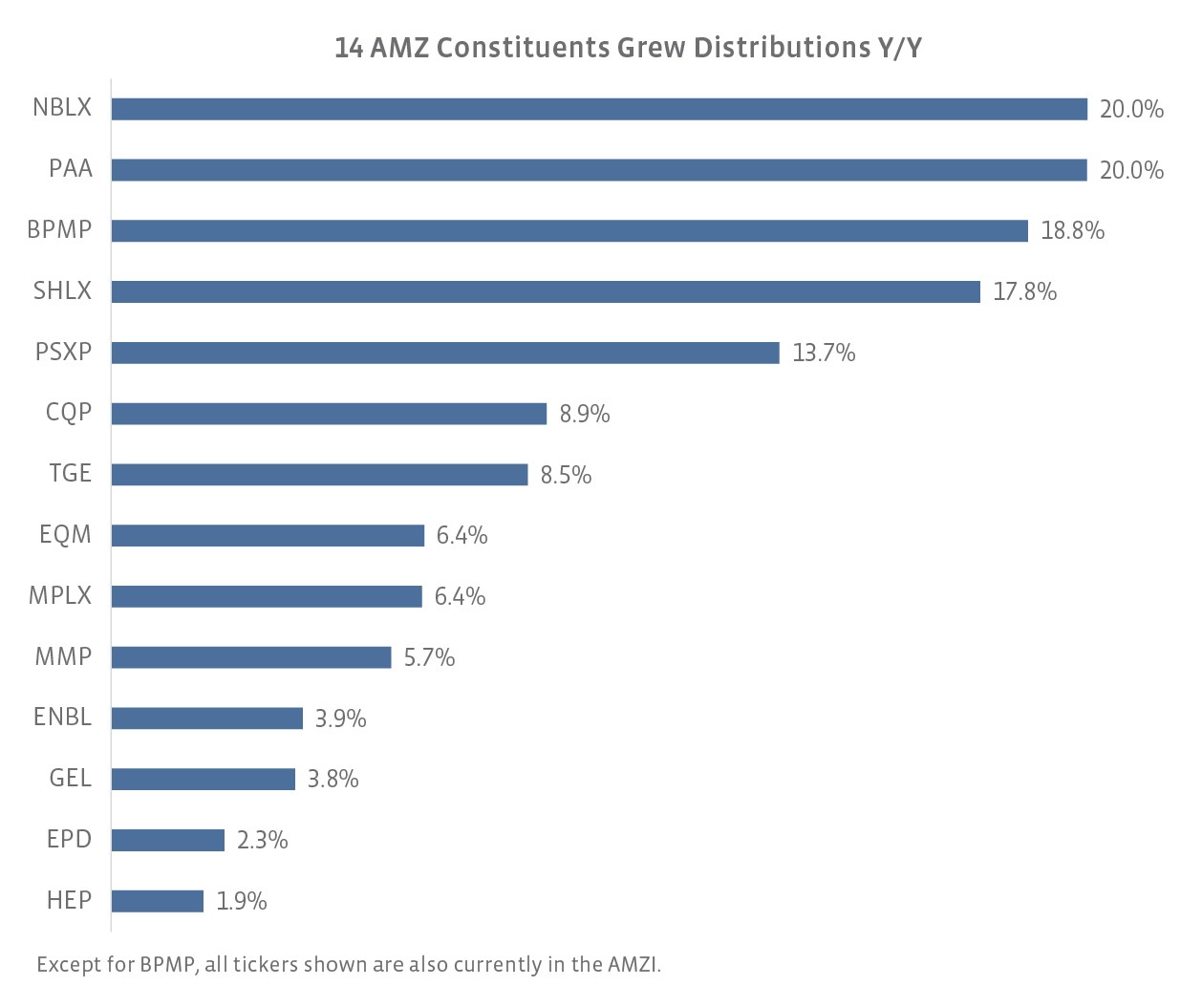

Most AMZ and AMZI constituents grew their distributions year-over-year.

The charts below compare the 2Q19 distribution with the 2Q18 distribution for those names that were in the index in both periods. Note that this approach introduces survivorship bias. As a result of the AMZ methodology change that became effective in December 2018, eleven tickers have been excluded from the year-over-year comparison for the AMZ since they were not in the index in 2Q18. Similarly, one ticker, NBLX, was excluded from the AMZI since it was not in the index in 2Q18. The charts below compare the 2Q19 distributions for EnLink Midstream (ENLC), Energy Transfer (ET), and Western Midstream Partners (WES) with the 2Q18 distribution of their related predecessor in the index.

AMZ constituents that maintained their distribution in 2Q19 relative to 2Q18 include (all names listed are also in the AMZI):

Crestwood Equity Partners(CEQP)

DCP Midstream(DCP)

NGL Energy Partners(NGL)

NuStar Energy(NS)

TC PipeLines(TCP)

Of the four year-over-year distribution cuts for the AMZI, three of the cuts (ENLC, ET, WES) were backdoor cuts as a result of transactions, while the other cut was from Buckeye Partners (BPL). BPL maintained its distribution at $0.75 per unit in advance of its buyout by IFM Investors (read more). The AMZ had an additional cut from Summit Midstream Partners (SMLP), which announced a distribution decrease as part of a series of strategic actions in 1Q19.

MLP distributions continue to trend positively.

As discussed last quarter, the outlook for MLP distributions continues to improve as evidenced by some MLPs resuming distribution growth, consolidation transactions subsiding, and improving distribution coverage. ENBL cited its steady growth in distributable cash flow, rising distribution coverage, and progress with self-funding equity growth capital as underpinning its decision to increase its distribution. Similarly, Plains All American (PAA) increased its 1Q19 distribution by 20% after achieving its deleveraging goals. These distribution increases reflect both improved financial positioning and a positive outlook. With consolidation transactions in late innings (read more), backdoor cuts seem to largely be behind the space, which should also lead to more stable distributions. Finally, distribution coverage remains healthy, implying that MLPs are better able to afford their payouts. Stay tuned for more on that topic next week.

{kind=link}

{kind=link}

{kind=link}