AMZ constituent American Midstream Partners (AMID) disclosed it would stop paying a distribution as a result of entrance into an amended credit agreement. AMID cannot pay a distribution until its leverage ratio falls below the 5.0x threshold as specified in its credit agreement.

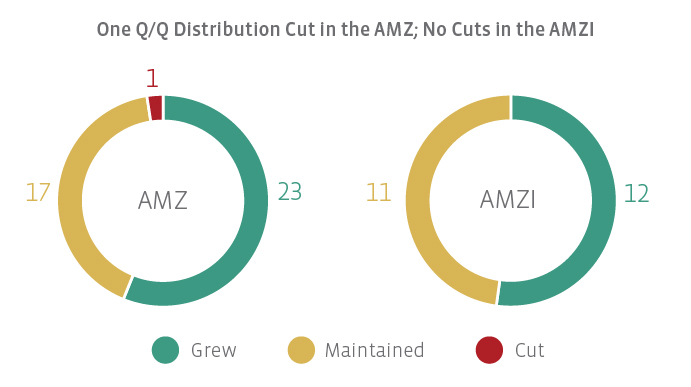

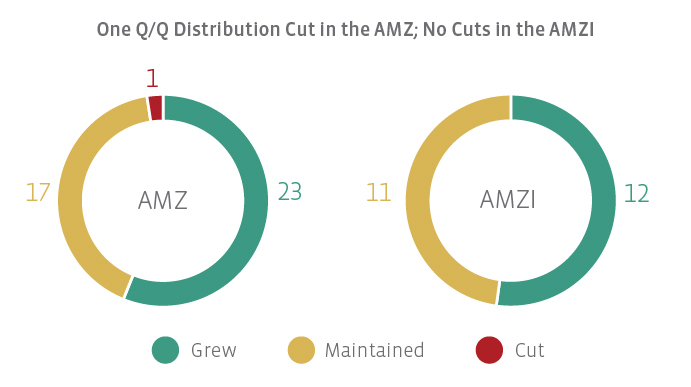

Notable Q/Q data points for the AMZ and AMZI.

The majority of constituents in both the AMZ and AMZI grew their distributions quarter-over-quarter. General partner Antero Midstream GP (AMGP) led the AMZ with the highest sequential increase by raising its distribution 13.0% sequentially to $0.29 per unit. For the sixth straight quarter, Antero Midstream Partners (AM) was the leader in the AMZI, increasing its distribution by 6.8% to $0.47 per unit. Other constituents with notable sequential growth were Phillips 66 Partners (PSXP) with a 5.4% increase and Shell Midstream Partners (SHLX) with a 4.7% increase.

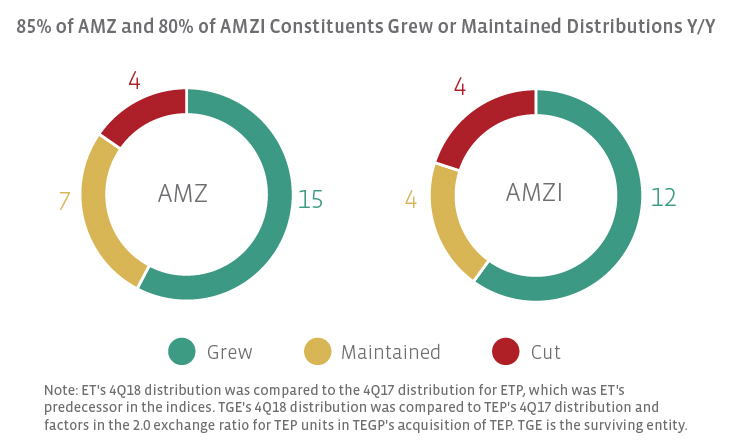

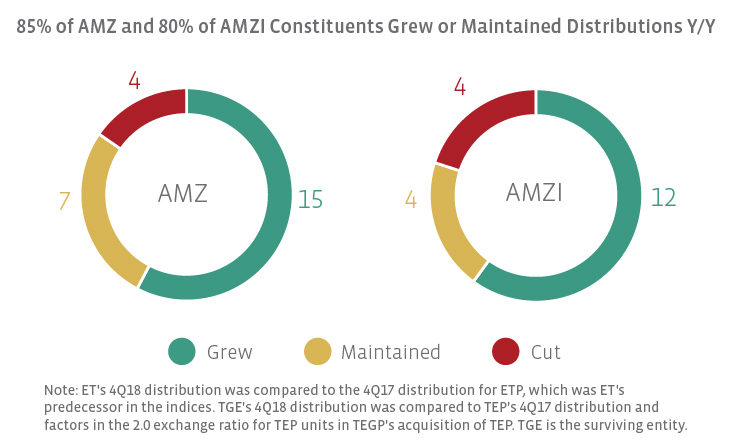

Most AMZ constituents grew their distributions year-over-year.

The charts below compare the 4Q18 distribution with the 4Q17 distribution for those names that were in the index in both periods. Please note that this method introduces survivorship bias. As a result of the recent methodology change in the AMZ, sixteen tickers are not reflected in the year-over-year analysis since they were not in the index in 4Q17. EQGP Holdings and Valero Energy Partners were not included due to the corporate actions mentioned previously.

AMZ constituents that maintained their distribution in 4Q18 relative to 4Q17 include (names with an asterisk are also in the AMZI):

- Crestwood Equity Partners (CEQP)

- DCP Midstream (DCP)

- Enable Midstream Partners (ENBL)

- EnLink Midstream Partners (formerly ENLK)

- NGL Energy Partners (NGL)

- Plains All American Pipeline (PAA)

Summit Midstream Partners (SMLP)

Four constituents in both the AMZ and AMZI had a year-over-year decrease in their distributions, including: NuStar Energy (NS), TC PipeLines (TCP), Buckeye Partners (BPL), and Energy Transfer (ET). ET’s 4Q18 distribution was compared to Energy Transfer Partners’ (former ticker ETP) 4Q17 distribution, as ETP was the predecessor in both indices. There were no distribution cuts in 4Q17, so we did not see any distribution cuts roll off this quarter on a year-over-year basis.

Distribution growth continues to trend toward moderation.

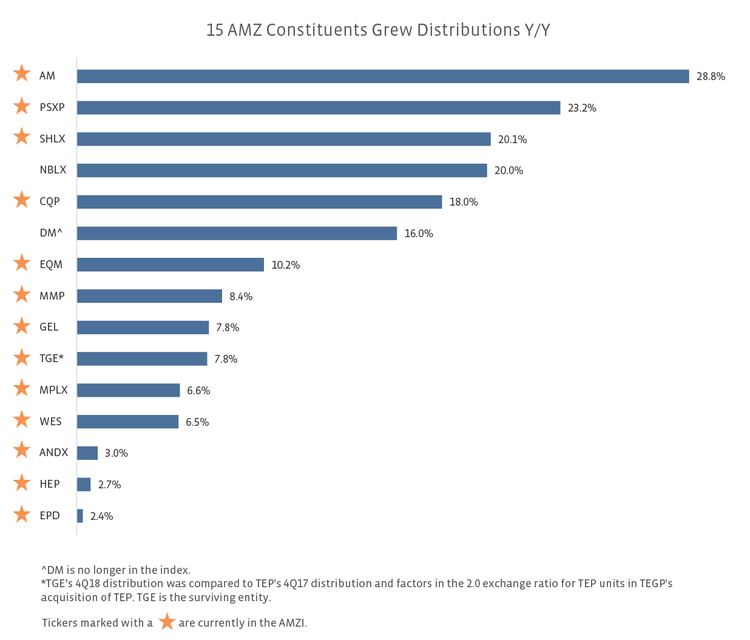

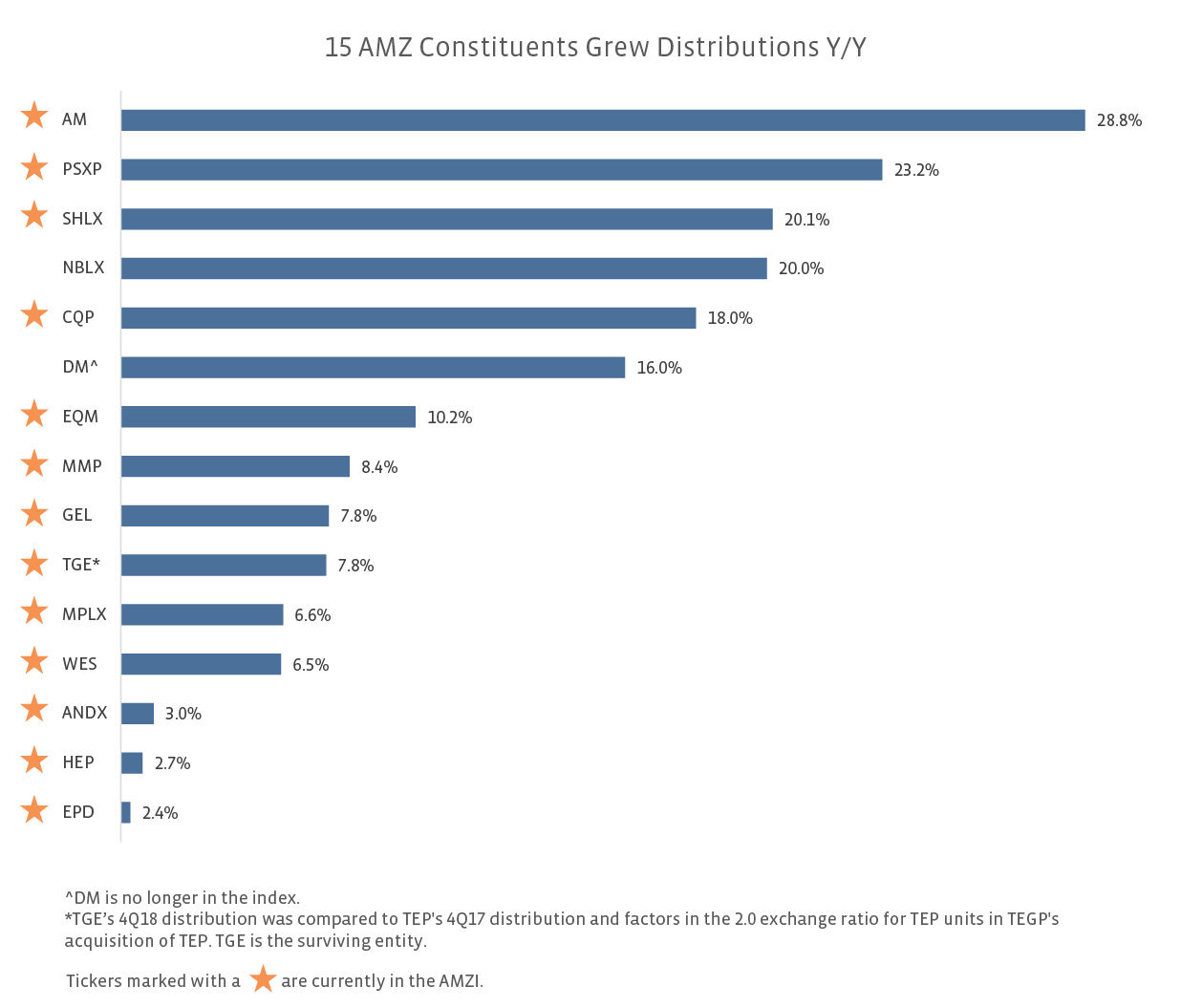

The fastest-growing distributions continue to come from companies with incentive distribution rights (IDRs). AM, PSXP, SHLX, and Noble Midstream Partners (NBLX) saw 20.0%+ distribution growth on a year-over-year basis, and all have IDRs. As we mentioned last quarter, MLP management teams are continuing to consider and pursue IDR eliminations. As part of its merger, EnLink Midstream (ENLC) agreed to eliminate EnLink Midstream Partners’ IDRs. In February, Equitrans Midstream (ETRN) announced it will exchange and eliminate EQM Midstream’s (EQM) IDRs, and refining general partner PBF Energy (PBF) will eliminate the IDRs of AMZ constituent PBF Logistics (PBFX). The reasons cited for these transactions include lowering the company’s cost of capital, increasing financial flexibility, and simplifying and aligning corporate structure. Additionally, the investment community has expressed frustration with IDRs. This is an area to watch as more IDR elimination announcements are possible this year. As of the January 25 special rebalancing, 73% of the AMZI and 68% of the AMZ had eliminated IDRs, with two IDR elimination transactions still pending in 1Q19.

While MLPs with IDRs tend to have higher distribution growth than their peers, it’s important to note that distribution growth in general continues to moderate across the MLP space. In the AMZI, only two constituents had sequential quarterly distribution increases greater than 5%, and the median percentage growth was 1.8% among constituents that increased distributions Q/Q. In a similar vein, only four AMZI constituents and seven AMZ constituents grew in the double digits from 4Q17 to 4Q18. While distribution growth is moderating, it accommodates other positive developments among MLPs, including far fewer equity issuances as companies move toward self-funding, better leverage metrics, improved distribution coverage (a topic we’ll discuss next week), and unit buybacks in some cases. For instance, Enterprise Products Partners’ (EPD) management recently commented that their investors expressed a clear preference for buybacks over distribution growth. Distributions and buybacks are both means of returning capital to unitholders, but as we’ve discussed, buybacks may not make sense for everyone.

Bottom Line

The fourth quarter was a nearly spotless quarter for MLP distributions, and most constituents in both the AMZ and AMZI grew their distributions quarter-over-quarter and year-over-year. Distribution growth has downshifted to a lower rate as MLPs pursue self-funding equity, better leverage metrics, and improved distribution coverage. Today’s high growers will likely see moderation over time as MLPs move to eliminate incentive distribution rights.

{kind=link}

{kind=link}

{kind=link}