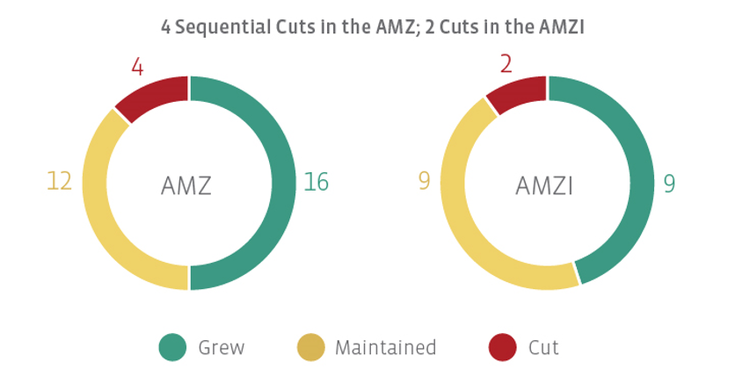

After a cut-free 3Q19 for both indexes, there were four distribution cuts in the AMZ and two cuts in the AMZI in 4Q19. EnLink Midstream’s (ENLC) 33.7% sequential distribution cut came as little surprise given its lofty yield of over 18% at the end of December, even after a 29.1% increase in price performance for the month. On its January guidance call, ENLC’s management stated that its distribution reset will allow the partnership to fully fund its capital program, generate excess free cash flow after the distribution, and bring leverage below 4x in 2021. As part of its take-private agreement with Blackstone Infrastructure Partners, Tallgrass Energy (TGE) suspended its distribution pending the expected close of the transaction in 2Q20. AMZ constituents Martin Midstream Partners (MMLP) and Summit Midstream Partners (SMLP) both announced their second distribution cut within the last year, cutting by 75.0% and 56.5%, respectively. As of the December 20, 2019 quarterly rebalancing, MMLP and SMLP have a combined weighting of just 0.36% in the AMZ. While the headline of four cuts reads negatively, TGE is a unique situation given its take-private transaction, and the small size of MMLP and SMLP bears noting.

Overall, the vast majority of midstream MLPs either maintained or grew their distributions on a sequential basis. Compared to 3Q19, 50% of AMZ constituents and 45% of AMZI constituents grew their distributions. Notably, Crestwood Equity Partners (CEQP) announced a 4.2% distribution increase, its first raise since it cut in 2016. CEQP management indicated that annual distribution increases will be evaluated based on expected free cash flow generation. Additionally, Rattler Midstream (RTLR) raised its distribution in its second ever payment since its May 2019 IPO. RTLR’s $0.29 per unit distribution, which it intends to maintain throughout 2020, represents a 16% sequential increase.

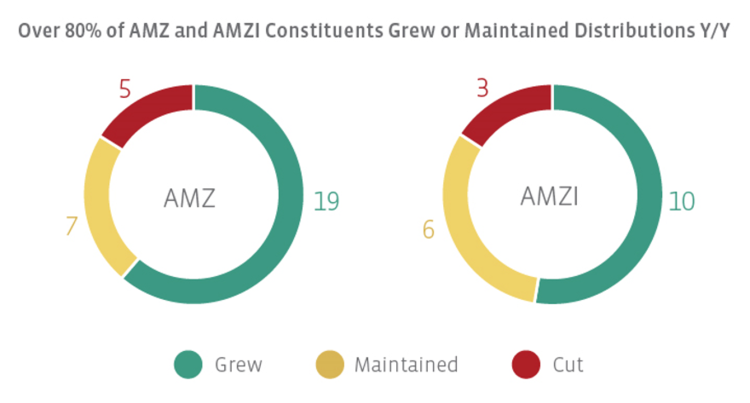

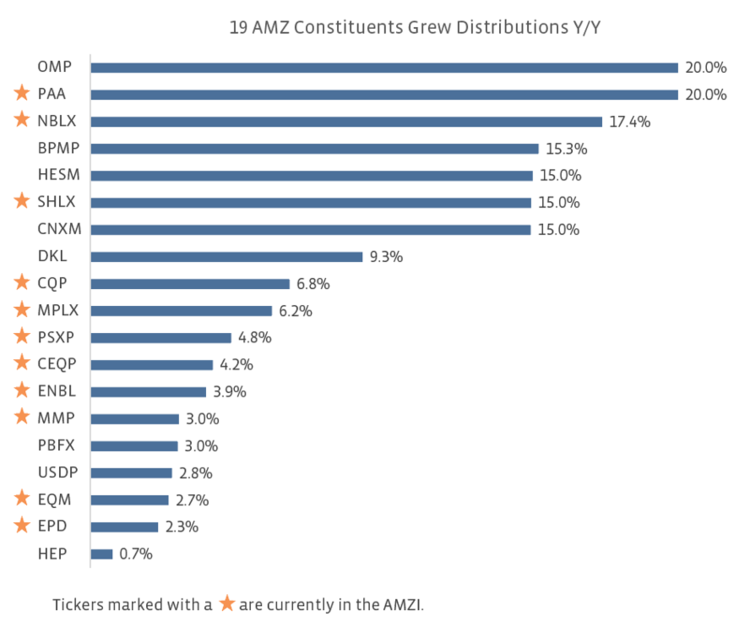

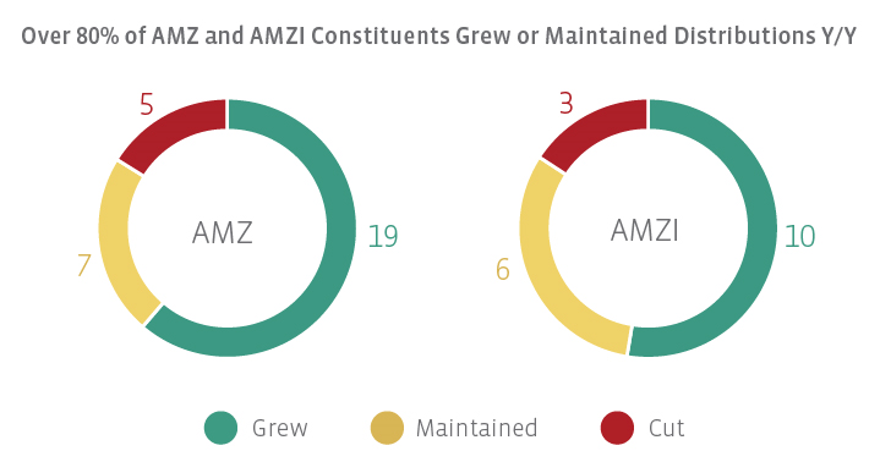

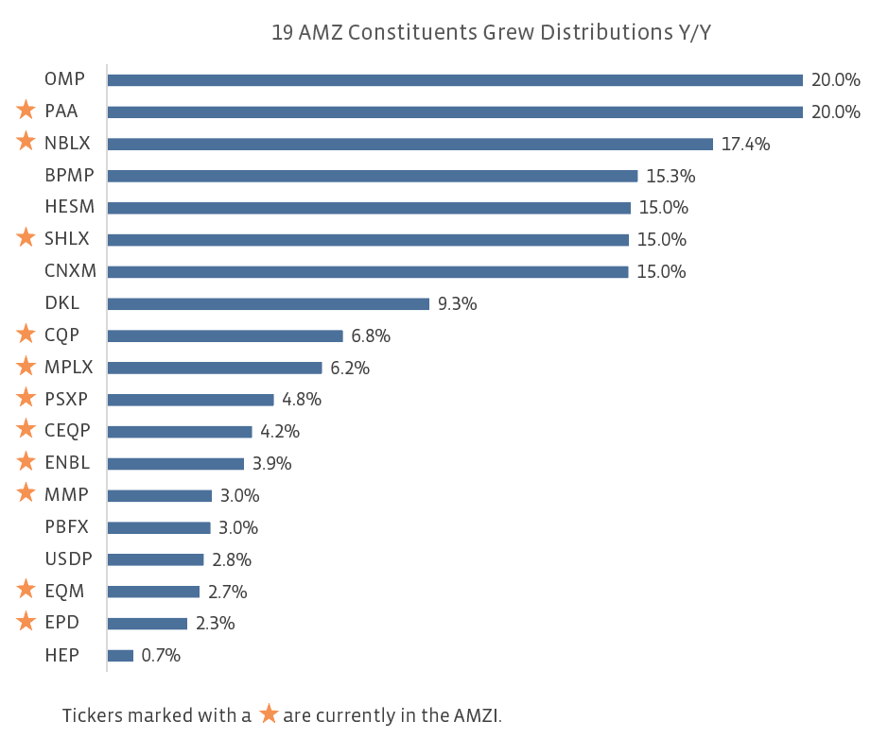

The majority of AMZ constituents have grown their distributions on a year-over-year basis.

The charts below compare the 4Q19 distribution with the 4Q18 distribution for those names that were included in the index in both periods. Note that this approach introduces survivorship bias. Only two partnerships are excluded from this analysis. RTLR was not included in the AMZ in 4Q18, and Noble Midstream Partners (NBLX) was not included in the AMZI in 4Q18. The 4Q19 distributions of Western Midstream Partners (WES) and ENLC are compared to the 4Q18 distributions of their related predecessor in the index.

AMZ constituents that maintained their distributions in 4Q19 relative to 4Q18 include (names with an asterisk are also in the AMZI):

DCP Midstream (DCP)

Energy Transfer (ET)

Genesis Energy (GEL)

Green Plains Partners (GPP)

NGL Energy Partners (NGL)

NuStar Energy (NS)

TC PipeLines (TCP)

Shifting to year-over-year cuts, WES’s distribution cut came as a result of its simplification transaction that closed in 1Q19, and the remainder of the cuts in the AMZ and AMZI were for 4Q19.

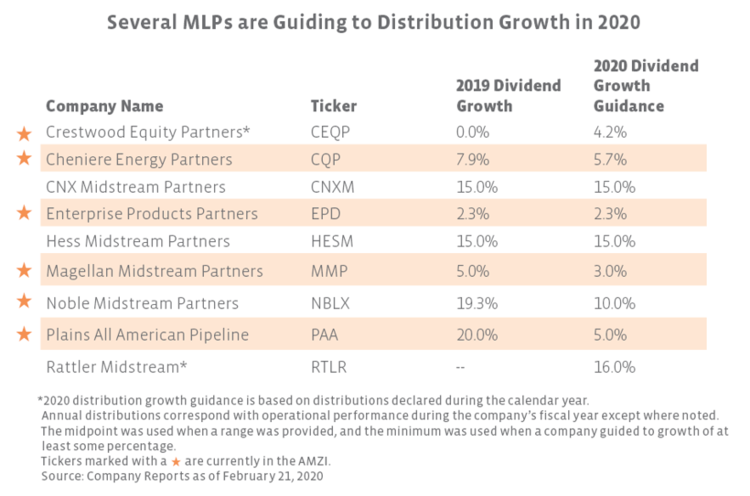

The outlook for MLP distributions remains positive.

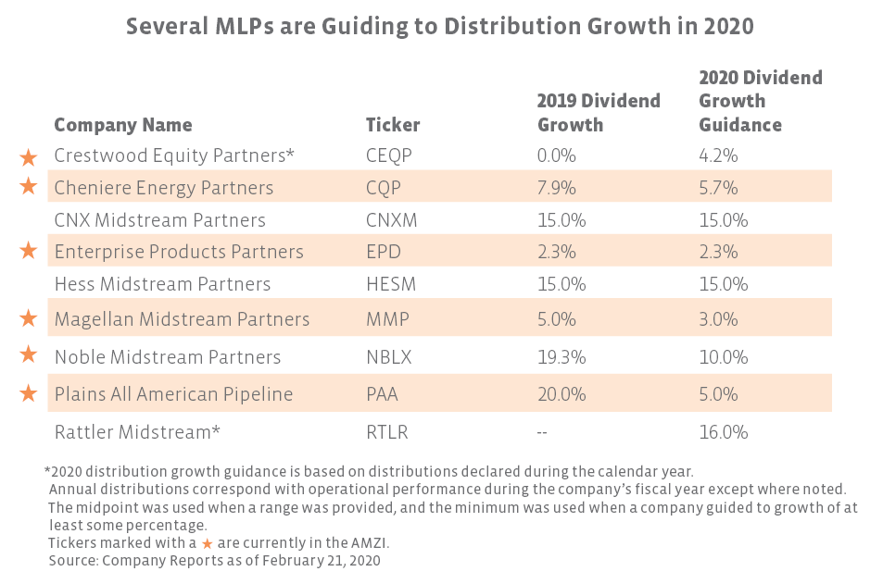

Overall, the outlook for midstream MLP distributions is still constructive. As shown in the table below, many AMZ and AMZI constituents are guiding to robust distribution growth this year, and others have maintained steady distributions for over a year (read more). Some of the largest names in the space, including Enterprise Products Partners (EPD), Magellan Midstream Partners (MMP), and Plains All American (PAA), are forecasting 2020 distribution growth in the range of 2%-5% with distribution coverage ratios for 4Q19 above 1.5×. Additionally, EPD and MMP are supplementing their unitholder returns with unit buyback programs. As capital expenditures moderate across the industry, the resulting potential free cash flow generation could lead to further distribution increases or buybacks (read more). Stay tuned for next week as we examine midstream payout ratios and distribution coverage for MLPs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}