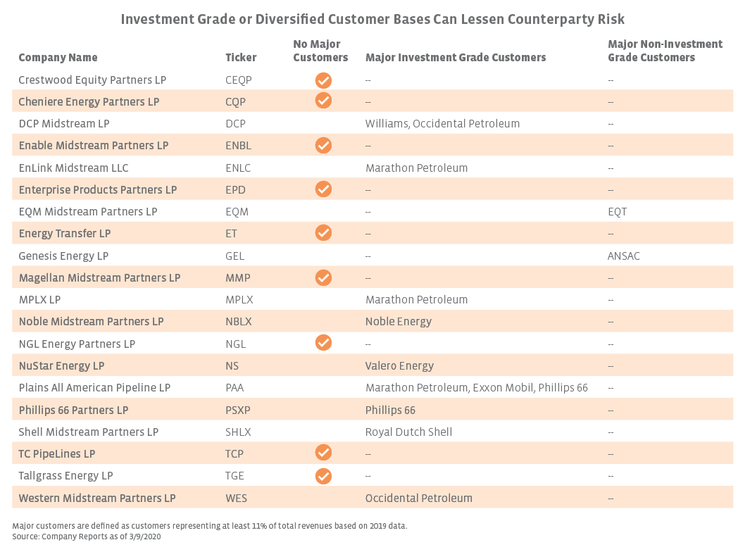

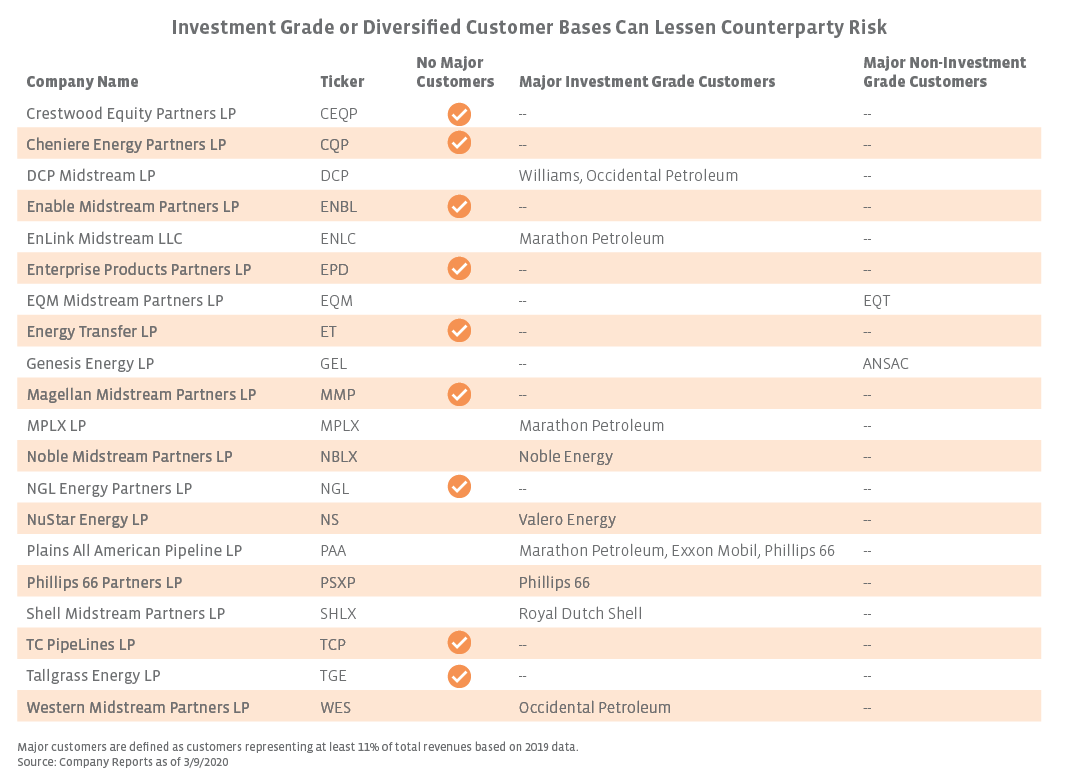

What about counterparty risk and E&Ps as midstream customers?

Counterparty risk reflects the concern that midstream companies are exposed to producer customers that could be under stress and potentially unable to fulfill their end of contracts as activity declines. Overall, the MLPs in the AMZI are either exposed to a large, investment grade customer or provide services to a variety of customers, which helps diversify counterparty risk. In reviewing 2019 annual reports, nine constituents representing 46.3% of the index by weighting have a diverse customer base without a single major customer (those that represent 11% or more of an MLP’s total revenue), while nine constituents possess a major customer that is investment grade rated accounting for 11% or more of total revenue (see table below).

Two AMZI constituents with less than 4% weights in the index – EQM Midstream Partners (EQM) and Genesis Energy (GEL) – have a non-investment grade major customer. EQT (EQT) accounted for 69% of EQM’s 2019 revenue and holds a BB+ rating from S&P (new gathering agreements were recently announced between EQM and EQT), while ANSAC is a private company without a rating that comprised 15% of GEL’s 2019 revenue. The five largest constituents in the AMZI Index seem to be well-positioned in terms of counterparty risk, with three of the five not having a single customer accounting for 11% or more of 2019 revenues – Energy Transfer (ET), Enterprise Products Partners (EPD), and Magellan Midstream Partners (MMP). Plains All American Pipeline’s (PAA) three largest customers accounted for 35% of 2019 revenue, and all were investment grade. MPLX’s (MPLX) biggest customer is its sponsor Marathon Petroleum Corporation (MPC) at 56% of 2019 revenues, which also holds an investment grade rating and as a refiner is less exposed to the absolute price of crude.

Bottom line

Admittedly, the future path of oil prices and the impact to producers remains to be determined. However, for midstream MLPs, yesterday’s selloff may reflect compounded fears that extrapolate some of the issues from 2014-2016 to today – despite the improved financial positioning of MLPs. Counterparty risk will likely remain in focus as the slump in oil prices continues, but AMZI constituents benefit from diversified and/or investment grade customer bases. While the near-term picture is cloudy at best, the long-term view for midstream MLPs remains intact in terms of playing a vital role in energy markets while offering investors attractive income, diversification, and real asset exposure.

{kind=link}

{kind=link}