Alerian’s Suite of Midstream Indices

While MLPs still make up the vast majority of the midstream market capitalization, there have been many changes this year. To continually reflect industry trends, Alerian recently launched the Alerian Midstream Energy Index (AMNA) and the Alerian US Midstream Energy Index (AMUS). In addition, the index name for AMEI was changed from the Alerian Energy Infrastructure Index to the Alerian Midstream Energy Select Index, and the AMEI methodology was revised to reflect more widely traded constituents of the AMNA.

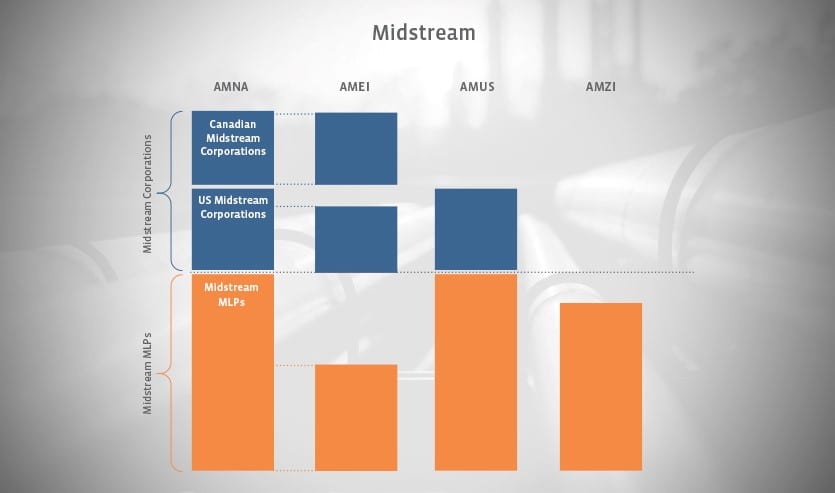

These three indices (AMNA, AMUS, AMEI), along with the Alerian MLP Infrastructure Index (AMZI), together make up Alerian’s suite of midstream energy indices. The four are related in their own ways and best explained in the chart below.

Image source: Alerian (approximate scaling)

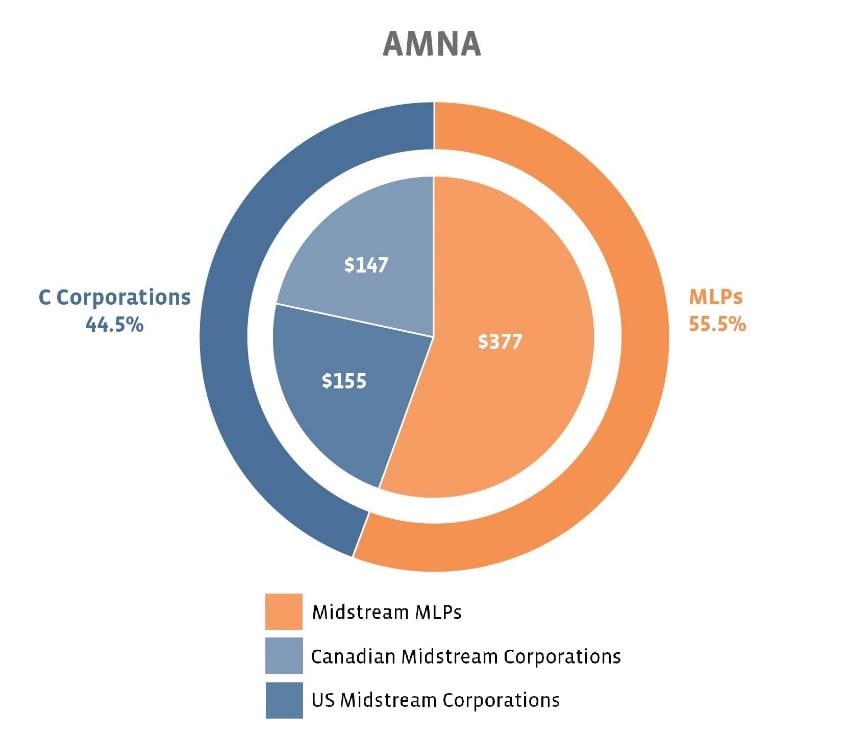

Alerian Midstream Energy Index (AMNA) // AMNA should be viewed as the full midstream universe. It is a composite index of North American midstream energy companies. Constituents can be pass-through entities (i.e. MLPs) or corporations, have principal offices in the United States or Canada, and they must earn the majority of their cash flow from midstream activities. What’s considered a midstream activity? Per the methodology, Gathering & Processing, Liquefaction, Pipeline Transportation, Rail Terminaling, and Storage, as defined by the Energy MLP Classification Standard (EMCSSM). Constituents are capped at a 10% weighting.

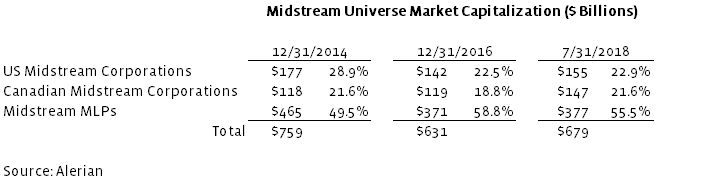

Midstream Universe Market Capitalization (in billions)

Alerian US Midstream Energy Index (AMUS) // Pretty self-explanatory, the AMUS is the US version of AMNA. No Canadian midstream companies. Constituents are capped at a 10% weighting. Sorry Canada, but there are still many other things we love about you: Tim Horton Timbits, JT dancing the Bhangra, poutine, maple syrup, nanaimo bars, Celine Dion. AMUS captures roughly 75%-80% of the midstream universe.

Alerian Midstream Energy Select Index (AMEI) // With a liquidity requirement, AMEI can be viewed as the liquid and investable subset of the AMNA. The index methodology eliminates redundant family exposure by favoring the general partner over a non-general partner. In addition, MLP exposure is limited to 25%. Similar to AMUS, AMEI also captures roughly 75%-80% of the midstream universe. (Broadly speaking, AMUS’ higher MLP weighting roughly offsets AMEI’s Canadian midstream weighting.)

Alerian MLP Infrastructure Index (AMZI) // No methodology changes were made here. The index is comprised only of midstream MLPs (no entities structured as corporations). AMZI captures roughly 50% of the midstream universe. AMZI captures roughly 85% of the midstream MLP universe.

Benchmarking – Which Alerian index to use?

While benchmarking in other asset classes may be more straightforward, for the midstream asset class, additional considerations must be made, particularly given the taxation nuances for different product types.

For products that are total return-focused and with no RIC constraints (i.e. MLPs are not limited to 25%), the AMNA or AMUS represent the cleanest midstream benchmarks. Examples of such products may be total-return focused midstream SMA (separately managed account) strategies that own both MLPs and corporations.

For products where MLPs are limited to 25%, the AMEI represents the most comparable benchmark. Examples of such products are 40 Act funds (ETFs, mutual funds, closed-end funds) that are RIC-compliant.

For products that are income-focused strategies and primarily own midstream MLPs (typically greater than 80%), the AMZI is the more relevant benchmark. Examples of such products may be income-focused SMAs and 40 Act funds (ETFs, mutual funds, closed-end funds) that are taxed as C Corporations. (Note: Depending on the percent of non-midstream MLPs owned, the AMZ may be more relevant.)

Ultimately, Alerian’s suite of four midstream indices is designed to provide more relevant benchmarking for industry stakeholders, furthering Alerian’s mission to equip investors to make informed decisions about energy infrastructure and MLPs.

{kind=link}

{kind=link}

{kind=link}