In part 1 of our “By the Numbers: The Alerian Effect” series, we highlighted how names entering the Alerian MLP Index (AMZ) and Alerian MLP Infrastructure Index (AMZI) outperform the respective index on the date of the rebalancing announcement by an average of 316 bps. We also discussed how the outperformance is magnified for names joining the AMZI versus the AMZ due to higher weightings and more AUM tracking the AMZI relative to the AMZ. Today, we’ll analyze the same announcement date impacts for names exiting the index.

Before beginning, we want to make clear that a removal from (or addition to) an Alerian index does not represent an opinion by Alerian on the company’s operations, growth projections, or management. It’s purely a methodological determination and generally comes down to three factors: market capitalization, adjusted market capitalization, and trading liquidity.

Now, onto the study.

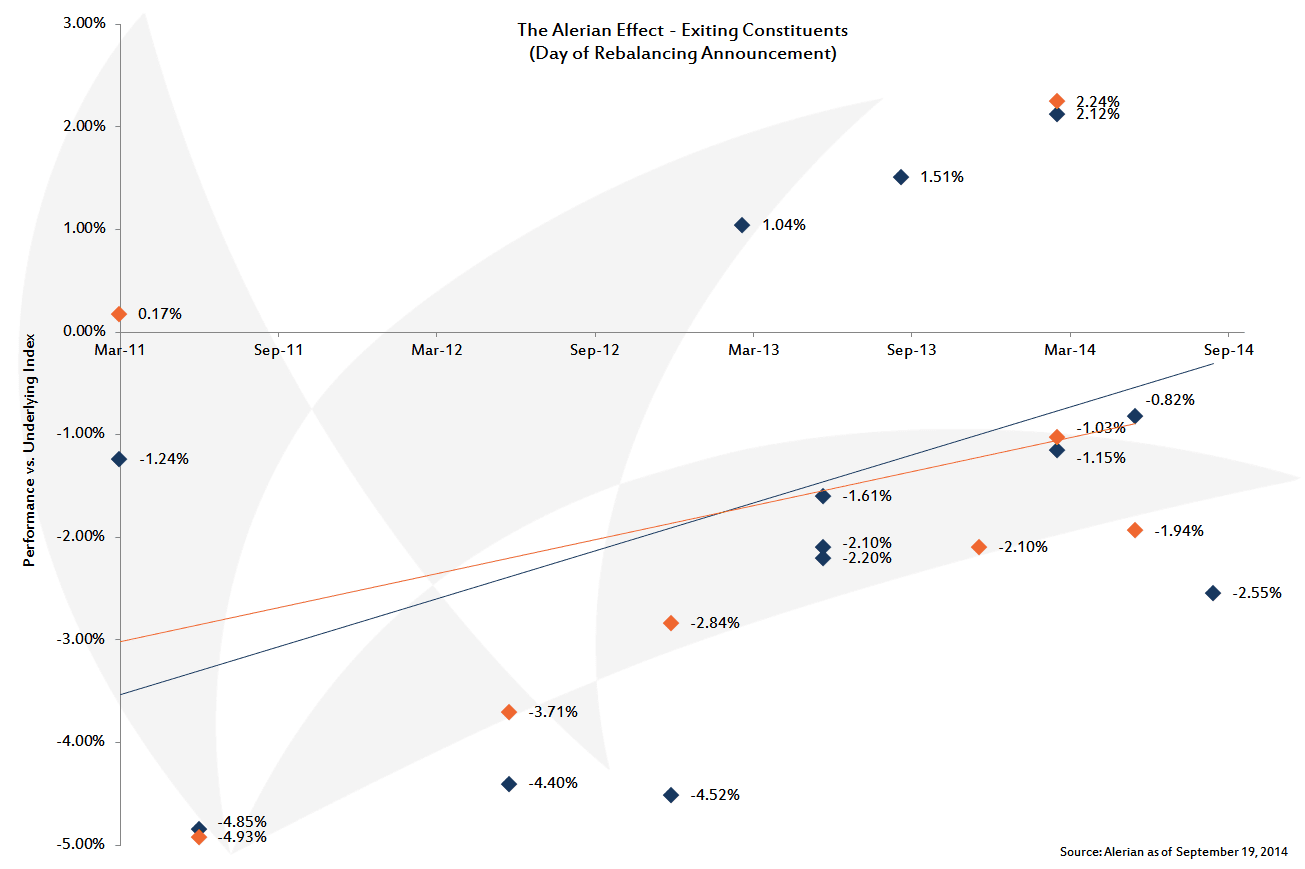

I hate to be the bearer of bad news, but since March 2011, the names that have been removed from the AMZ or AMZI have underperformed their respective index by 166 bps on the day of announcement, on average. On the bright side, this represents a more muted impact—nearly half—versus the names entering the index, which as we noted above is +316 bps. In addition, out of the 21 quarterly rebalancings with constituent changes, five MLPs actually outperformed the underlying index on announcement date.

As for whether the impact is more magnified for the AMZ (blue diamonds) or AMZI (orange diamonds), the difference is marginal. On average, names leaving the AMZ underperform the index by 160 bps on the announcement date versus 177 bps for names leaving the AMZI. Based on the upward trending lines, it would seem that the “Alerian Exit Effect” is becoming more muted over time. Visually that may be the case, but the data isn’t conclusive (yet). The R-squared values for the AMZ and AMZI trendlines are 0.20 and 0.14, respectively, suggesting little statistical significance.

The removal from (or addition to) a passive index does not affect the underlying business of a company. So if markets are truly efficient, meaning equities trade on fundamentals of all available information and not on sentiment, then savvy investors may see non-fundamental-based market reactions (such as the interpretation of index removal as a negative sign) as opportunities to buy. The more rebalancing iterations there are, the more investors start catching on and the less exaggerated corrections may be. Keep in mind, the key word in the phrase “if markets are efficient” is “if”.

Some could argue that one day may not be enough time for the markets to correct. In the next “By the Numbers: The Alerian Effect” series, we’ll delve into the performance of names entering and exiting the index during the period from the rebalancing announcement date to the actual rebalancing date to test this efficient markets theory further.

{kind=link}