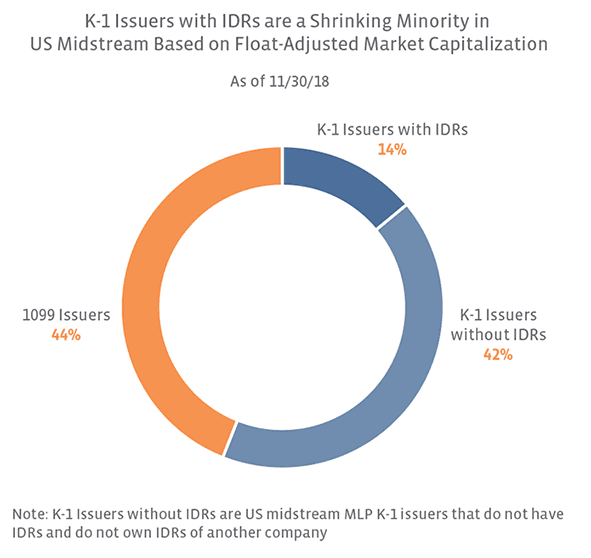

There were consolidation announcements that were not on our radar in July, including Valero’s (VLO) October announcement that it would acquire Valero Energy Partners (VLP). We discussed the potential consolidation of dropdown MLPs last month (read more), and in short, we would assign a greater probability to dropdown MLPs eliminating their IDRs over time than being consolidated by their parents. As we discussed in Part 2, an MLP does not have to be consolidated to eliminate its IDRs. As a recent example, Equitrans’ (ETRN) announcement that it would acquire EQGP Holdings (EQGP) included a proposal for ETRN to exchange EQM Midstream’s (EQM) IDRs for EQM units. As shown below, a significant weighting of K-1 Issuers has already eliminated IDRs. We would expect the weighting of K-1 Issuers with IDRs to continue shrinking.

Who could still be saying bye?

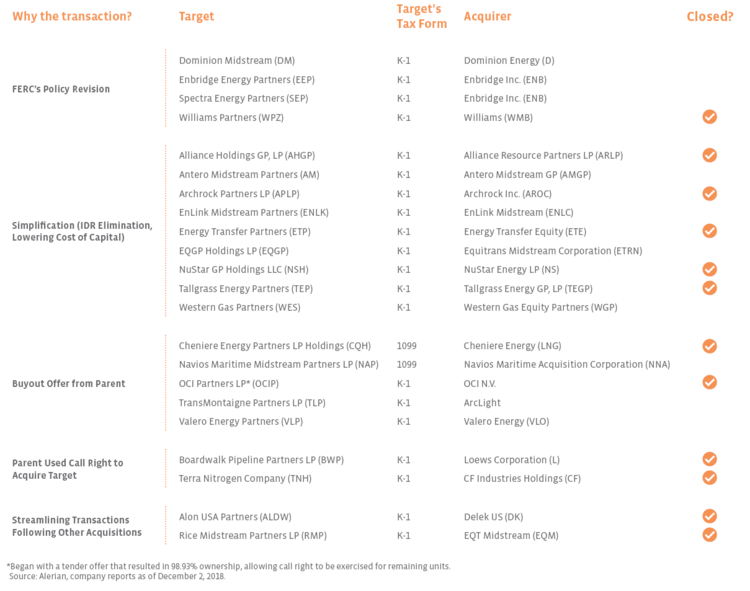

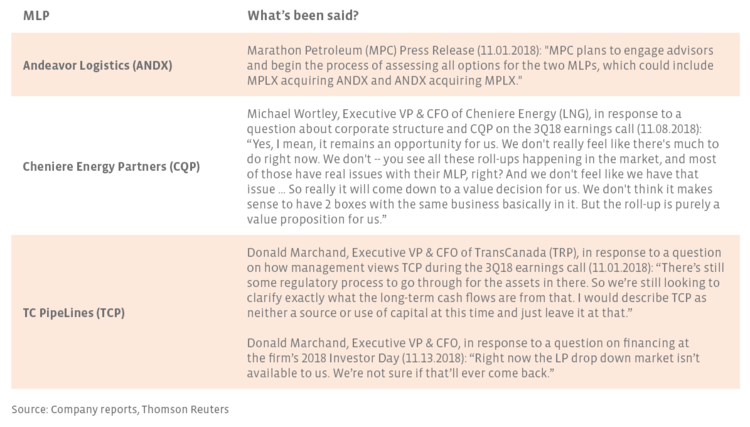

Of the ten MLPs/parents we identified in Part 2 that made comments regarding a restructuring or simplification, seven have announced transactions if we include Hi-Crush (HCLP) eliminating its IDRs. HCLP has been clear recently on its intention to pursue a corporate conversion. For those names that were included in Part 2 and have not announced a transaction, we provide updated commentary below. Andeavor Logistics (ANDX) is unique in that its parent, Andeavor, was acquired by Marathon Petroleum (MPC), which is now the general partner of both ANDX and MPLX (MPLX).

What’s an investor to do?

This question was addressed in Part 3 of our series, and the fundamental takeaway still holds true. If an investor primarily invested in the MLP sector for tax-deferred yield, he or she will still want to own individual MLPs or an access product that is predominately MLPs. If an investor is more focused on total return or broad exposure to midstream, which includes MLPs and corporations, that investor will probably find a RIC-compliant product (MLPs capped at 25%) more suitable to their needs. The trade-off for investors is that broad exposure comes at the expense of giving up some income since corporations have lower yields than MLPs.

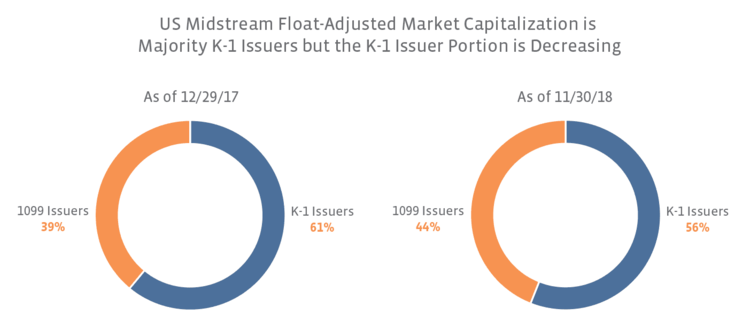

The pie charts below show how the US midstream float-adjusted market capitalization has changed from the end of 2017 to the end of November 2018. Pending transactions are not reflected in the chart, so this mix will continue to shift as transactions close. Clearly, K-1 Issuers have become less representative of the US midstream space and are likely to see their share of float-adjusted market capitalization decrease further in the near term as pending transactions close. However, we believe many MLPs will choose to remain in the structure for various reasons (including the fact that many have already eliminated IDRs) and primarily because the MLP structure remains the most tax-efficient way to hold midstream assets.

Bottom line: The consolidation trend is in late stages, and that should be welcomed by investors.

Aside from the few companies discussed above that could still be saying bye, we think most consolidations have been announced at this point, and we are in the late stages of this trend. We see the conclusion of these transactions as a potential catalyst for the midstream sector. As the pending transactions are closed and structure questions move out of the spotlight, investors should be better able to focus on the fundamentals and the positive implications for EBITDA growth (see table with 2019 EBITDA guidance from last week’s post). While restructurings and distribution cuts have been frustrating for investors, we think the space has much less baggage (i.e. IDRs, anticipated distribution cuts, etc.) today than it did a year ago or two years ago – a situation that should not be lost on both midstream and generalist investors.

{kind=link}

{kind=link}

{kind=link}

{kind=link}