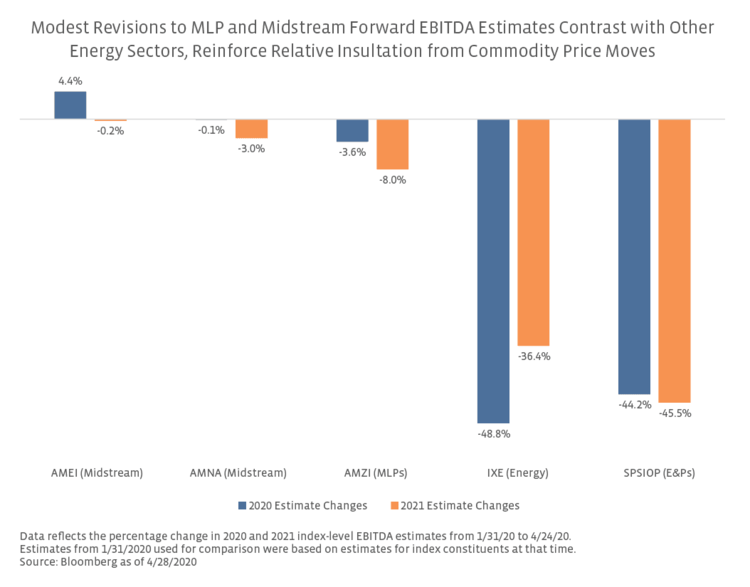

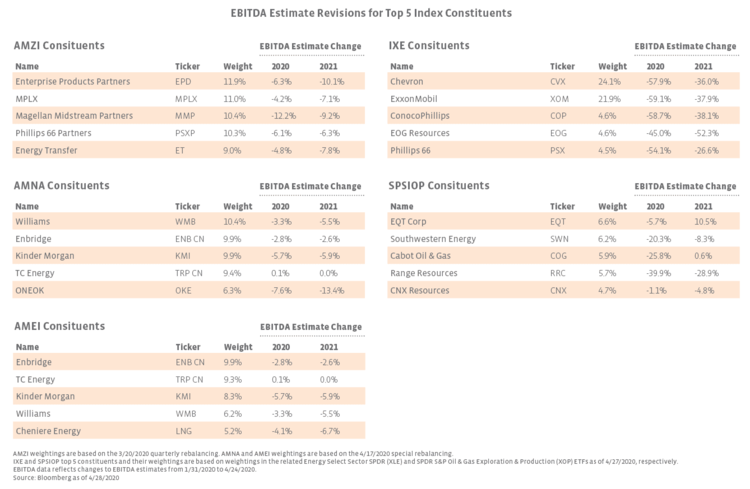

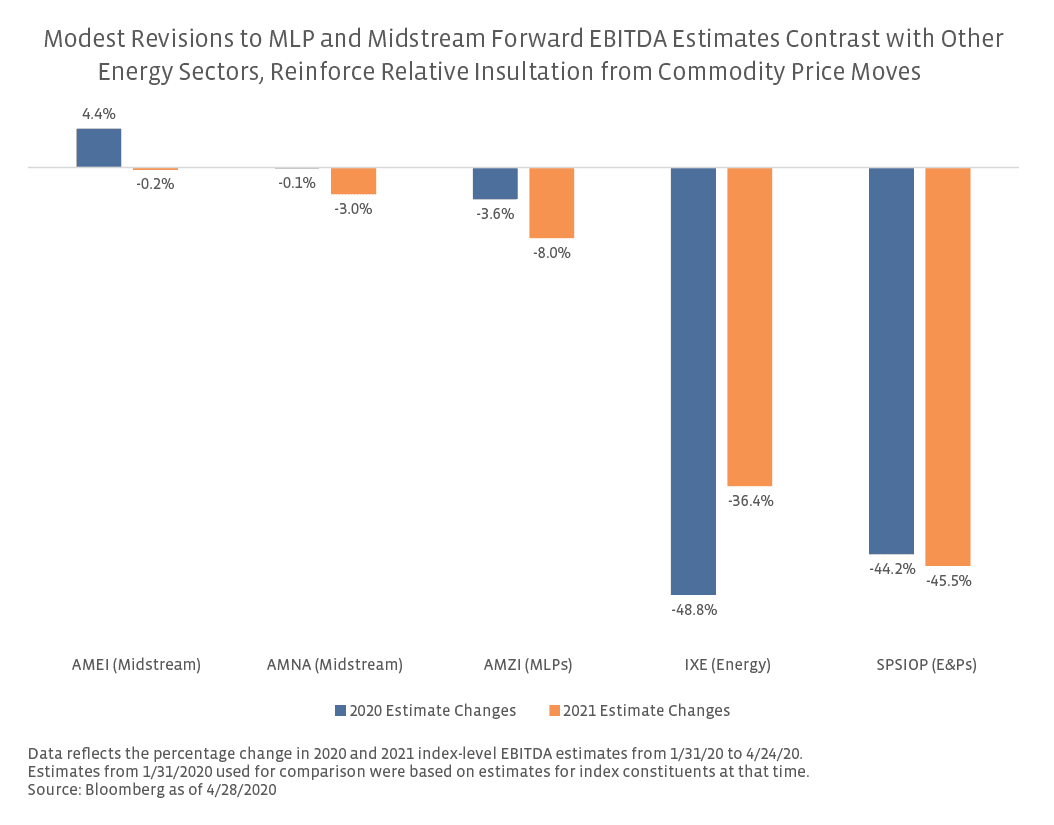

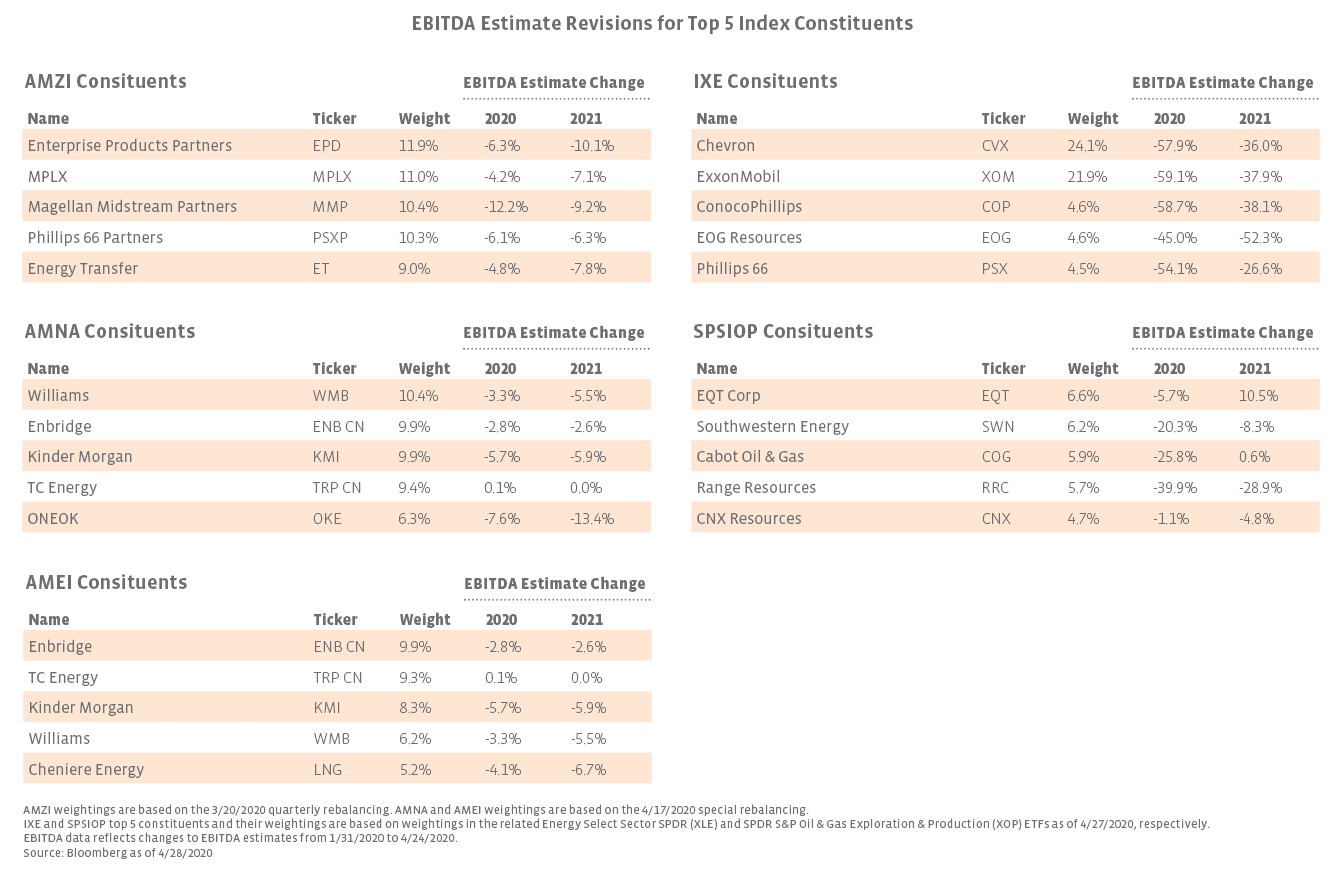

Given that we are in the early innings of earnings season for midstream and the energy space more broadly, analyst estimates may be further adjusted in the coming days as updated company outlooks are incorporated. Admittedly, estimates for all indexes, which aggregate consensus estimates for constituents, could include stale estimates. It also bears noting that Alerian’s indexes were rebalanced in March. As a result of the rebalancing, two constituents were added to the AMZI, while one was removed. Five names were removed from the AMNA Index, with the five names having a combined weight of less than 0.1% in AMNA after the last rebalancing in December. There were no constituent changes for the AMEI Index, but Tallgrass Energy (former ticker TGE) was removed from AMNA and AMEI in a special rebalancing earlier this month. While changes were relatively modest, they could somewhat distort the comparison between the two time periods. The IXE and SPSIOP were not rebalanced in between the end of January and April 24. To provide additional context, the table below shows 2020 and 2021 EBITDA estimate revisions for the five largest names by weighting in each index. The revisions for midstream names on the left and the IXE and SPSIOP constituents on the right are clearly very different in terms of magnitude.

To further frame midstream EBITDA outlooks, we highlight recent company commentary from the last few days. In its distribution cut announcement and update on Monday, NGL Energy Partners (NGL) provided EBITDA guidance for fiscal 2021 (year ending March 31, 2021), which represents a slight year-over-year increase relative to the high end of reiterated full-year EBITDA guidance for fiscal 2020 (year ended March 31, 2020). While asset sales and acquisitions complicate year-over-year comparions for NGL, it bears noting that the partnership expects to be free cash flow positive in fiscal 2021 after distributions, capex, and deferred payments related to an acquisition. In its earnings announcement last week, Kinder Morgan (KMI) reduced its 2020 adjusted EBITDA forecast by 8%, which also represents an 8% decline from 2019. ONEOK (OKE) indicated yesterday that full-year 2020 adjusted EBITDA would likely be between $2.6 and $3.0 billion, which would imply a 13.2% reduction to prior 2020 EBITDA guidance at the midpoint. OKE noted that it was impractical to provide traditional guidance for 2020+ at this time. While a small sample size, the updates help to reinforce the resilience of midstream EBITDA in a lower oil price environment and mark a strong contrast with the ~40% downward revisions for the IXE and SPSIOP.

The benefits of midstream’s fee-based business model are clearly evident in the more minor revisions for 2020 and 2021 EBITDA estimates compared to broader energy and E&Ps. While there are shortcomings in the comparison given index changes and the potential for stale estimates to skew the EBITDA estimates for all indexes, the data helps frame the relative insulation from commodity prices for midstream.

{kind=link}

{kind=link}