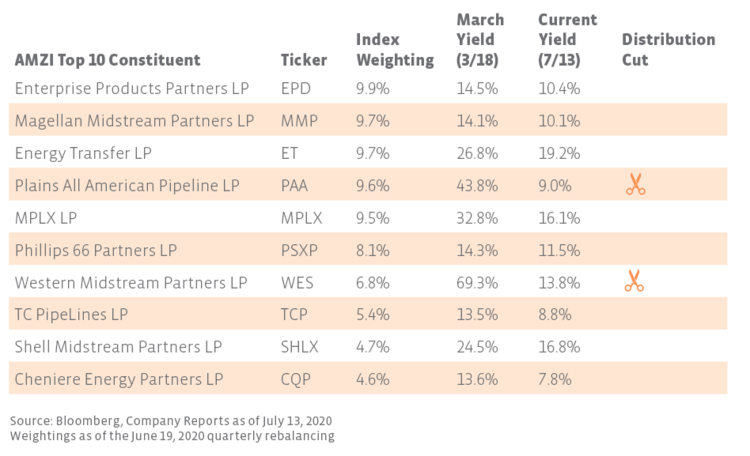

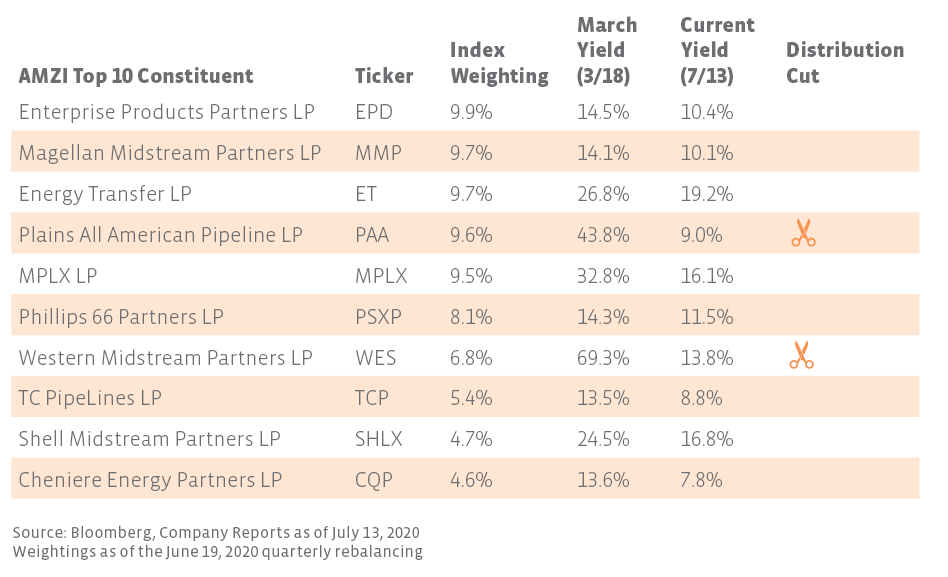

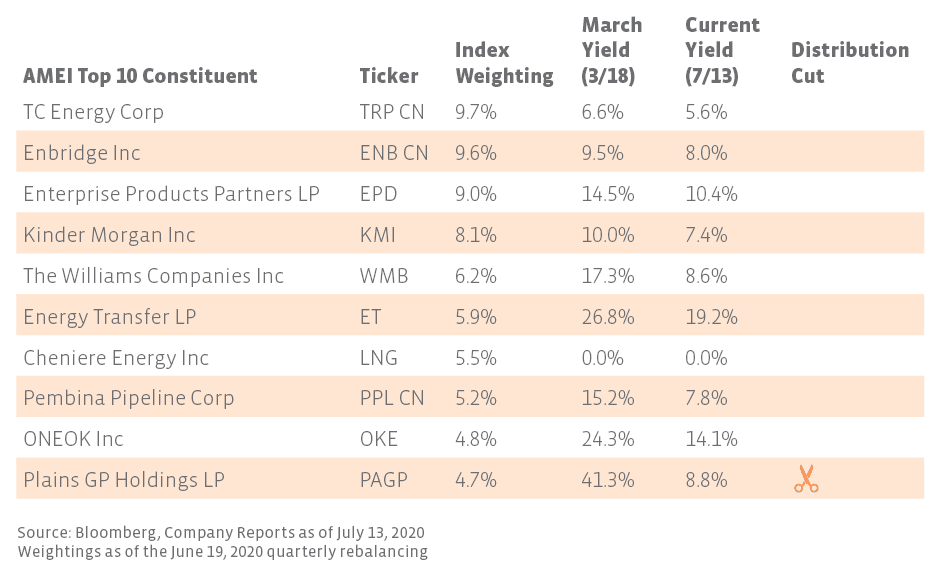

Top 10 AMZI and AMEI constituents highlight resilience among larger names.

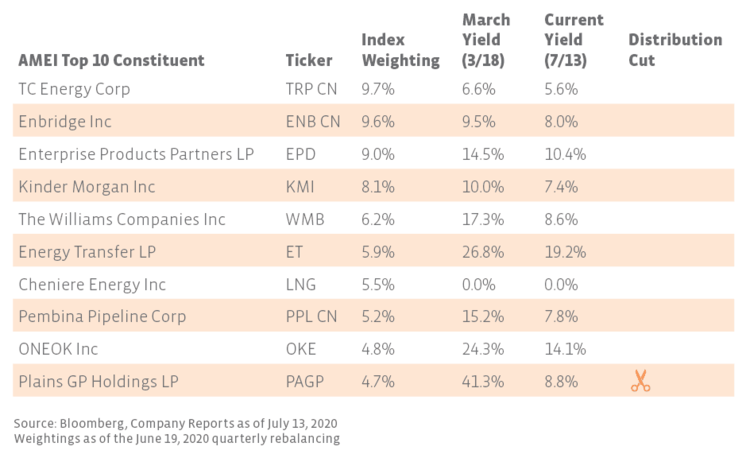

Focusing on the names with the greatest weighting in each index provides context for how yields have moved since March. The tables below compare yields on March 18 against current yields as of July 13 for the top ten names in the AMZI and AMEI indexes. Notably, for the AMZI, the companies with the highest yield spikes in March – Plains All American (PAA/PAGP) and Western Midstream (WES) – were also the two MLPs in the top ten that cut their distributions for the first quarter, indicating heightened investor expectations of a cut. There were 12 distribution cuts in the AMZI and 14 cuts in the AMEI for 1Q20, although 68.5% of the AMZI and 74.5% of the AMEI by weighting grew or maintained their dividends. While additional cuts are possible, we view cuts as less likely overall for this quarter and believe most midstream companies that needed to cut their dividends have likely done so at this point.

Among AMEI’s top ten constituents, PAGP represented the only dividend cut for 1Q20. Notably, the yields of Canadian C-Corps TC Energy (TRP CN) and Enbridge (ENB CN) have not experienced as much volatility and did not even reach double-digits as the space bottomed. The stability is not surprising considering their defensive performance within midstream (read more). Year to date through July 13, TRP CN and ENB CN have only fallen -17.0% and -21.8% on a price-return basis, respectively, compared to -36.4% for the AMEI. Relative to the other top ten constituents, Energy Transfer’s (ET) yield remains elevated at 19.2% as of July 13. ET has had to contend lately with uncertainty related to a potential shutdown of the jointly owned Dakota Access Pipeline (DAPL), which transports crude out of the Bakken. Last week, Moody’s revised its outlook on ET’s Baa3 investment grade rating to negative and pointed out the risks to earnings that would be caused by a prolonged halt of DAPL. On Wednesday, a federal appellate court temporarily stayed the order for DAPL to shut down while the case is being reviewed.

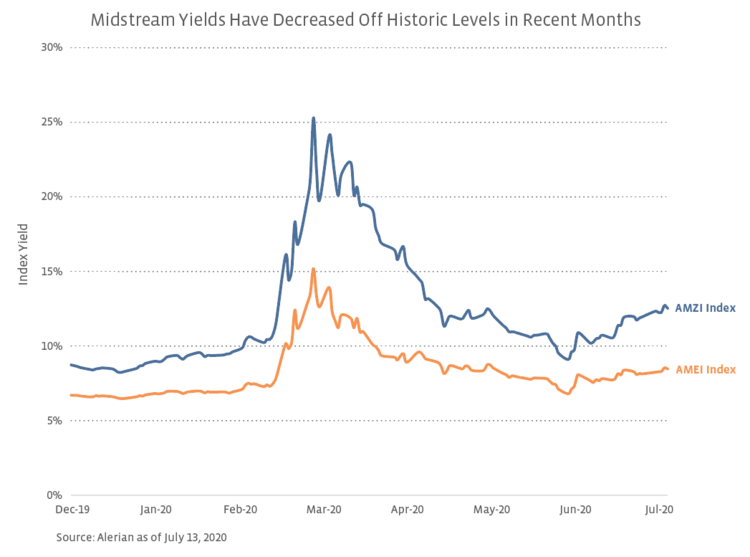

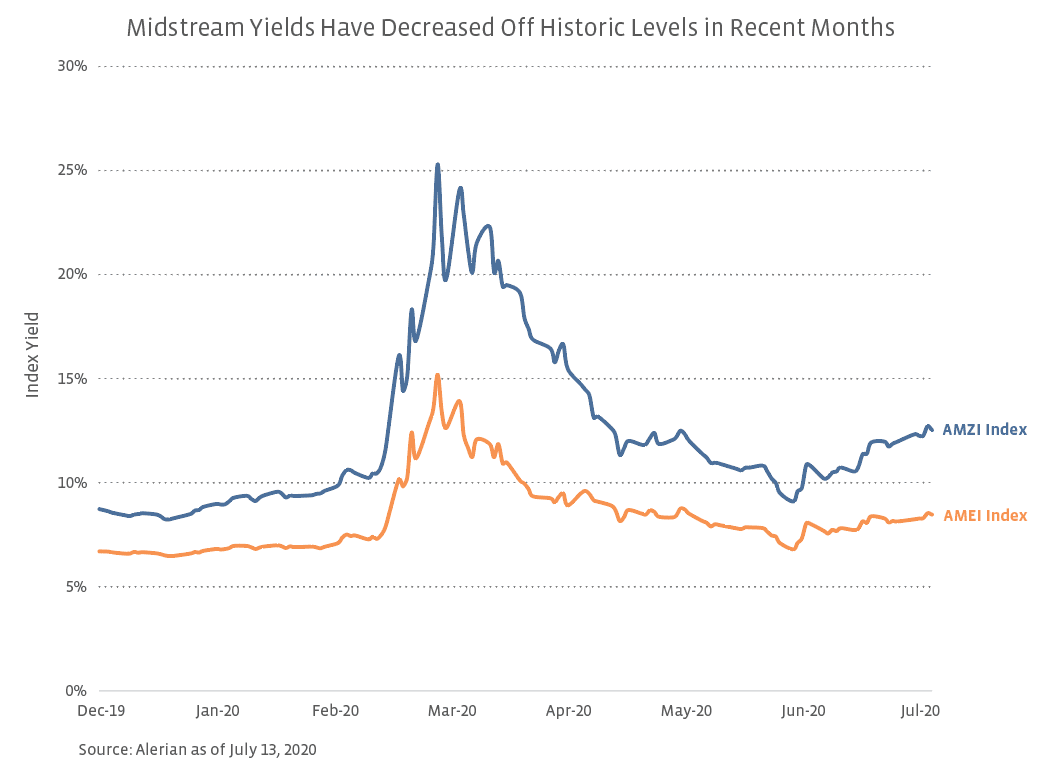

Yields reflect individual company situations and risk profiles, with factors such as financial positioning, contract protections, and geographic exposure to certain basins contributing to performance and yield levels. Overall, company yields have eased, though they are still loftier than they were prior to the pandemic and relative to history. In general, dividends have proven resilient for the top constituents in each index, with most large companies maintaining their dividends (read more).

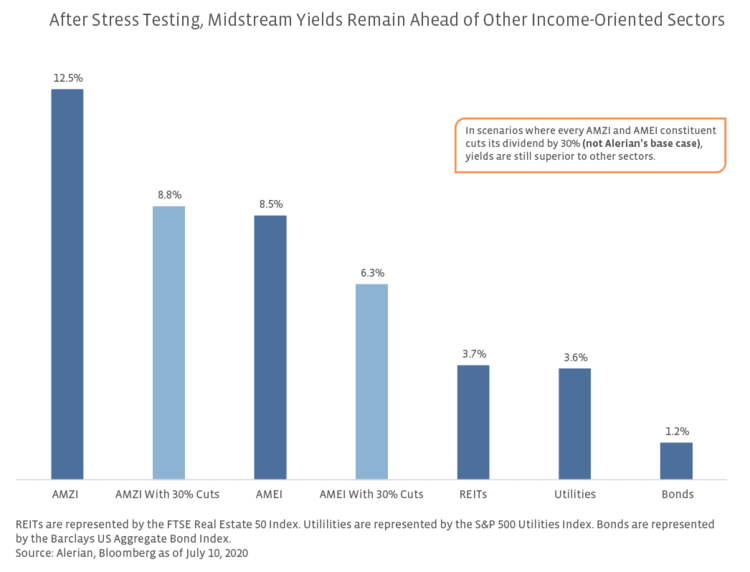

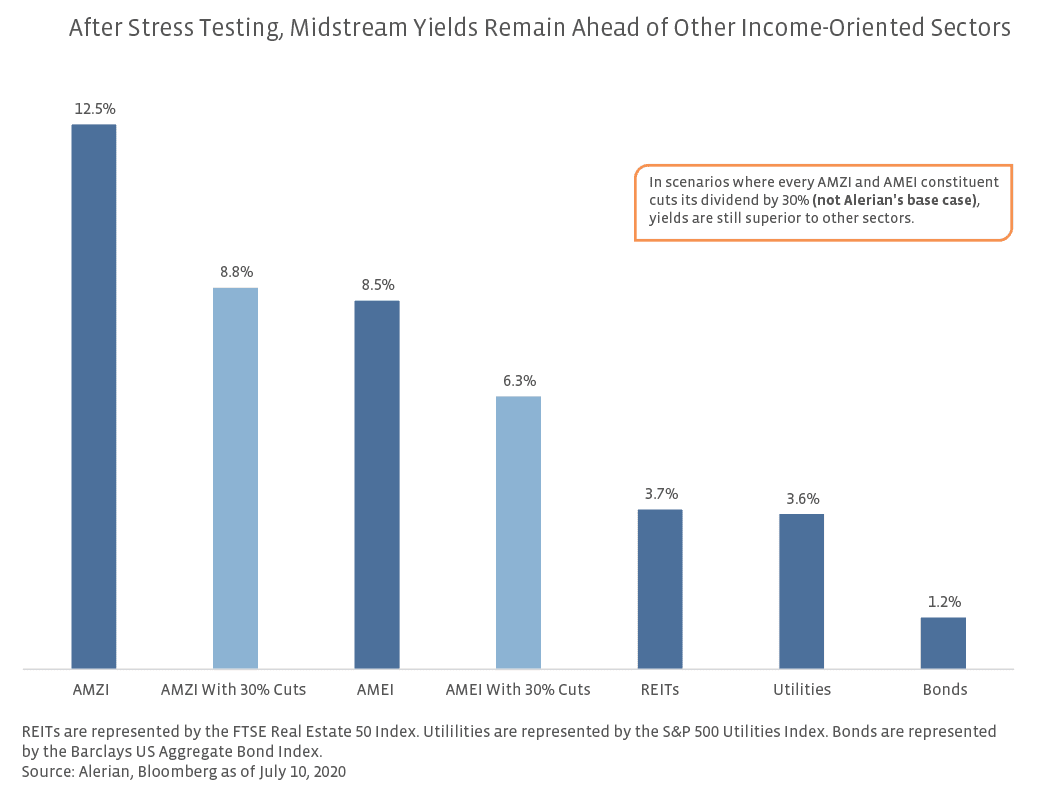

Updated stress tests show midstream maintains a yield advantage even in draconian scenarios.

With midstream yields coming down as a result of improved equity performance and some dividend cuts for 1Q20, we are updating the AMZI and AMEI yield stress test scenarios introduced in March to look at how midstream yields would compare to other income-oriented sectors under hypothetical 2Q20 dividend cut scenarios. The scenario tests assume all constituents in each index cut their dividends by an additional 30% on top of what has already been announced for 1Q20. Cuts are assumed even for names that have already announced dividends. To date, PAA/PAGP, Enterprise Products Partners (EPD), Genesis Energy (GEL), Antero Midstream (AM), Keyera (KEY CN), Pembina Pipeline (PPL CN), and Inter Pipeline (IPL CN) have already announced they are maintaining their dividends for 2Q20 or for July 2020 if paid monthly. Please note these stress tests are designed for illustrative purposes only and do not represent Alerian’s base case. To reiterate, Alerian views cuts as less likely overall for 2Q20 and believes necessary cuts have largely been announced. In the charts below, the base index yields are current as of July 10 and incorporate all announced dividend cuts. The chart compares the two midstream indexes and their stress tests with other notable income-oriented sectors – REITs, Bonds, and Utilities.

For the AMZI, index yields are well above the other income sectors in the comparison. Assuming an additional 30% distribution cut for the constituents of the index, the AMZI would yield greater than 500 basis points more than REITs and Utilities. Shifting gears, the AMEI has a lower yield than the AMZI due to the 25% cap on MLPs. However, AMEI’s yield is still generous relative to other income-oriented investments. Even a hypothetical 30% reduction in dividends for AMEI constituents would result in a yield advantage of over 200 basis points versus REITS and Utilities. Whether looking solely at MLPs (AMZI) or broader midstream (AMEI), the income advantage for midstream is significant – even when stress tested.

Bottom Line

Midstream yields remain at elevated levels and are considerably greater than other income-oriented sectors. In an environment of low interest rates, the attractiveness of midstream yields may give investors a reason to take another look at the space. Given improved financial positioning entering the current downturn and with most needed dividend cuts likely already completed, midstream income appears to be more durable today, and even stress tested yields are generous. Mathematically speaking, yields should fall as performance improves and macro headwinds and uncertainty subside. With the income for the space more durable today after significant cuts in 1Q20, a further reduction in yields is expected to be driven by better performance as opposed to more dividend cuts.

{kind=link}

{kind=link}

{kind=link}

{kind=link}