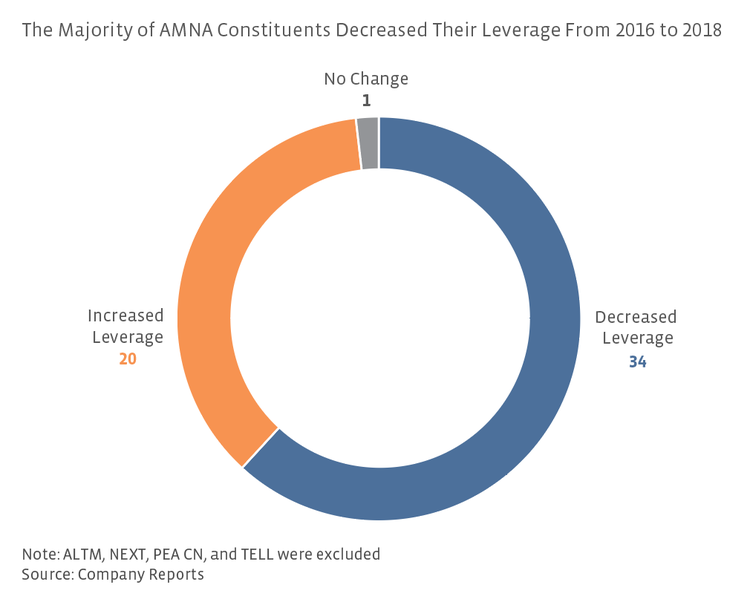

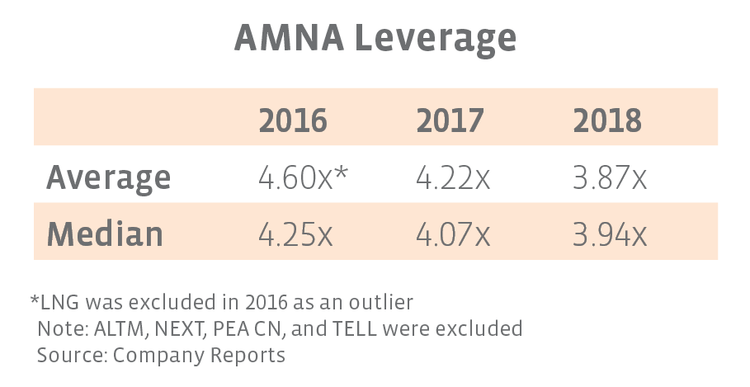

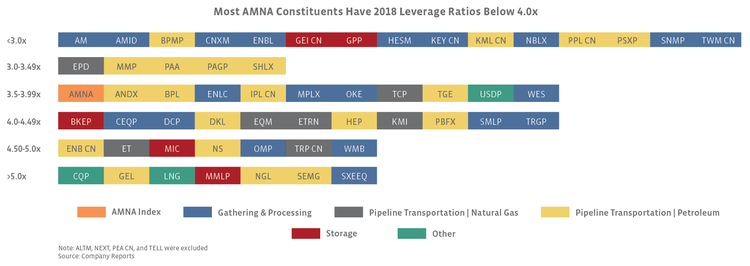

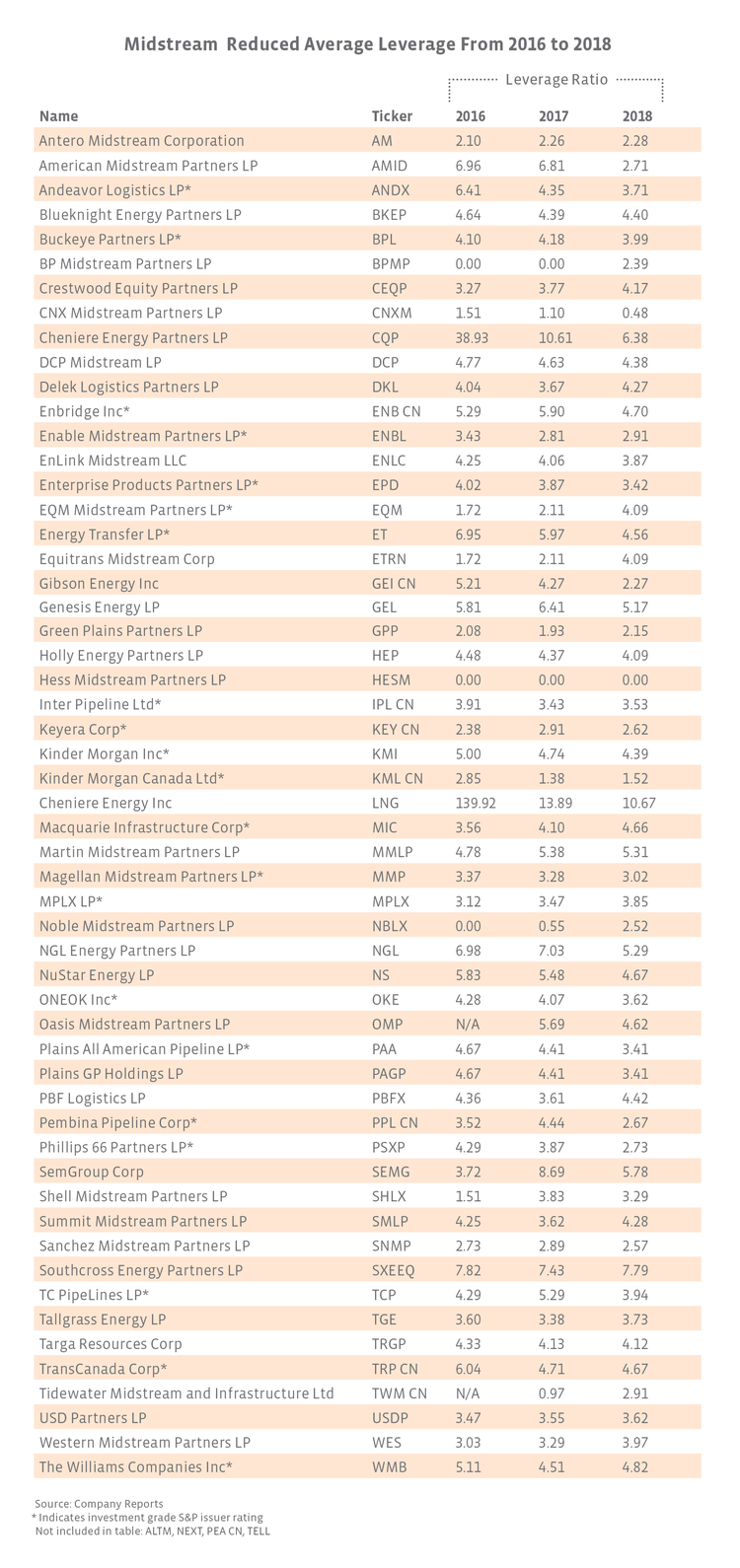

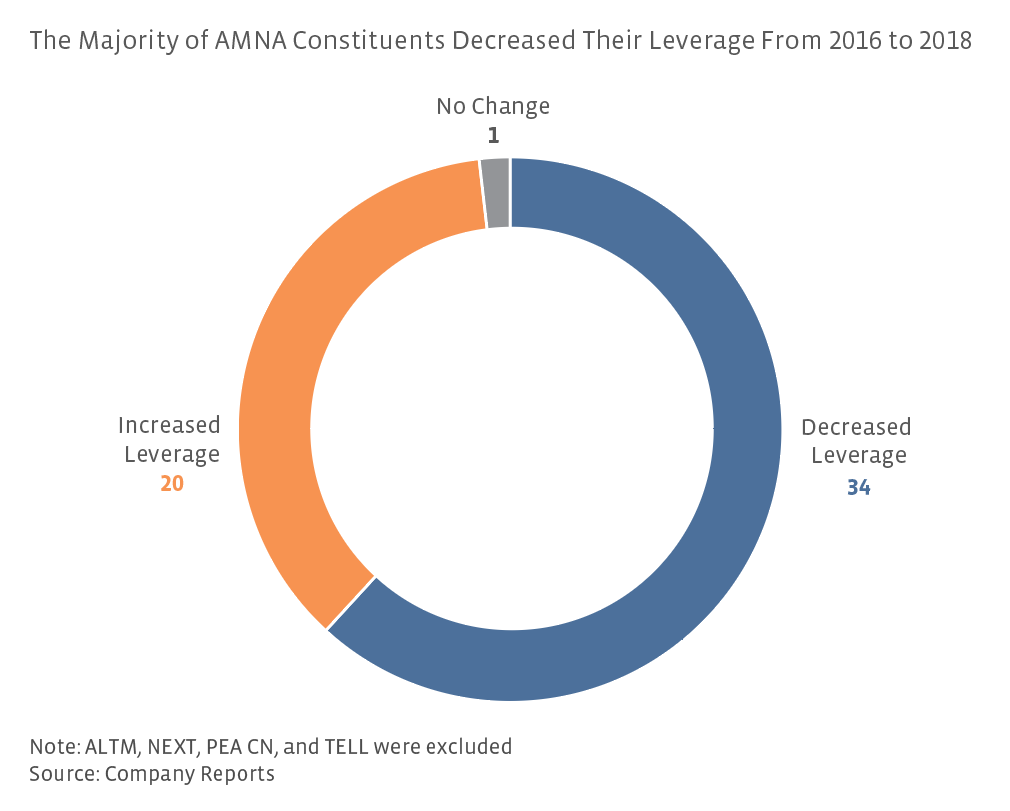

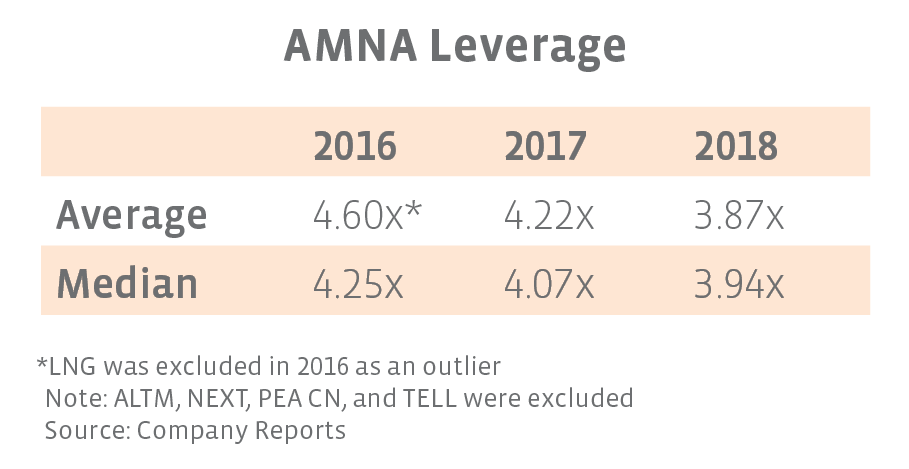

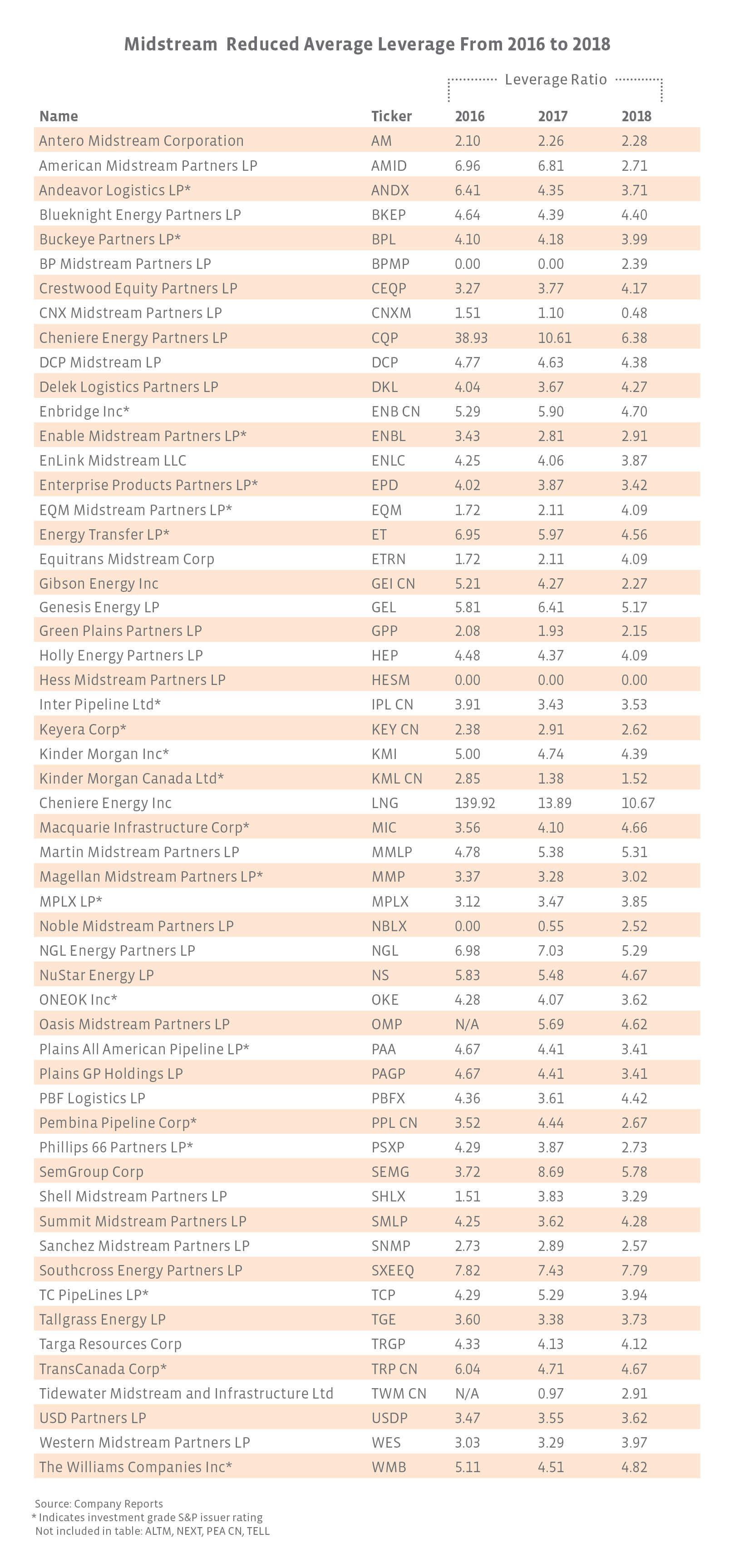

Several midstream companies have prioritized deleveraging as part of strategic, long-term plans. For example, Plains All American (PAA) recently completed its deleveraging plan announced in August 2017, with its leverage falling from 4.7x in 2016 to 3.4x in 2018. Going forward, the company is targeting leverage of 3.0-3.5x and plans to grow its distribution contingent on meeting its leverage and distribution coverage targets. Gibson Energy (GEI CN) has also decreased leverage significantly from 5.2x in 2016 to 2.3x at the end of 2018, well below the company’s long-term target range of 3.0-3.5x, with asset sales helping to fund growth capital and reduce the need to issue debt. While its leverage remains elevated compared to the rest of midstream, Cheniere Energy (LNG) has reduced its leverage since 2016 as a function of higher adjusted EBITDA stemming from the start-up of its LNG export capacity. In early June, the company released a capital allocation plan, which included achieving an investment grade corporate rating by reducing debt as one of its primary goals. Notably, the ten largest companies in the AMNA Index by weighting all reduced their leverage from 2016 to 2018.

Earlier-stage midstream companies and companies deploying capital for major projects were more likely to see leverage increase from 2016 to 2018. EQM Midstream Partners (EQM) saw its leverage rise from 1.2x in 2016 to 4.1x in 2018 and is in the process of constructing the Mountain Valley Pipeline, a $4.9-billion Northeast gas pipeline expected to be completed in mid-2020 (EQM is funding $2.4 billion of the overall cost). Similarly, Crestwood Equity Partners (CEQP) has increased leverage from 3.3x to 4.2x but has said it expects leverage to fall below 4.0x in the first half of 2020 after major projects come online. Among the names that have increased leverage are early stage companies and dropdown MLPs such as Noble Midstream Partners (NBLX) and BP Midstream Partners (BPMP), which went public in 2016 and 2017, respectively. While NBLX expects leverage of 4.0-4.25x in 2019, the company is targeting long-term leverage of 3.0×.

Lower leverage clears the way for a capital return focus.

Manageable leverage is important for running a sustainable midstream business through periods of market volatility, but it can also be viewed as a requirement before pursuing greater returns to shareholders. In short, it’s impractical to pursue accelerated distribution growth or share repurchases if leverage and the balance sheet in general are suboptimal. Furthermore, if growth capital expenditures are in the process of peaking for midstream broadly (as we suspect), that should support greater free cash flow generation, which enhances financial flexibility and the potential for returning capital to shareholders. Clearly, the progress being made across midstream to reduce leverage is positive for investors as companies become financially healthier. Reduced leverage provides an added benefit as a steppingstone to potentially greater shareholder returns.

Appendix

{kind=link}

{kind=link}

{kind=link}

{kind=link}