In our conversations this year with management teams, sell-side analysts, portfolio managers, even retail holders, the basic thesis that MLPs are an investment in the long-term build-out of North American energy infrastructure hasn’t changed, even as the Alerian MLP Index (AMZ) plunged 33.5% on a price return basis from August 2014 to August 2015. Given that, one would expect a flight to quality. Enterprise Products Partners (EPD), the largest MLP, fell 30.8% during the period, in line with the median. Some large caps like Plains All American Pipeline (PAA) underperformed (-39.8%) the median, while others like Energy Transfer Partners (ETP) and Magellan Midstream Partners (MMP) outperformed the median, falling 14.5% and 15.9%, respectively. There’s not enough of a trend to believe that flight to quality is occurring.

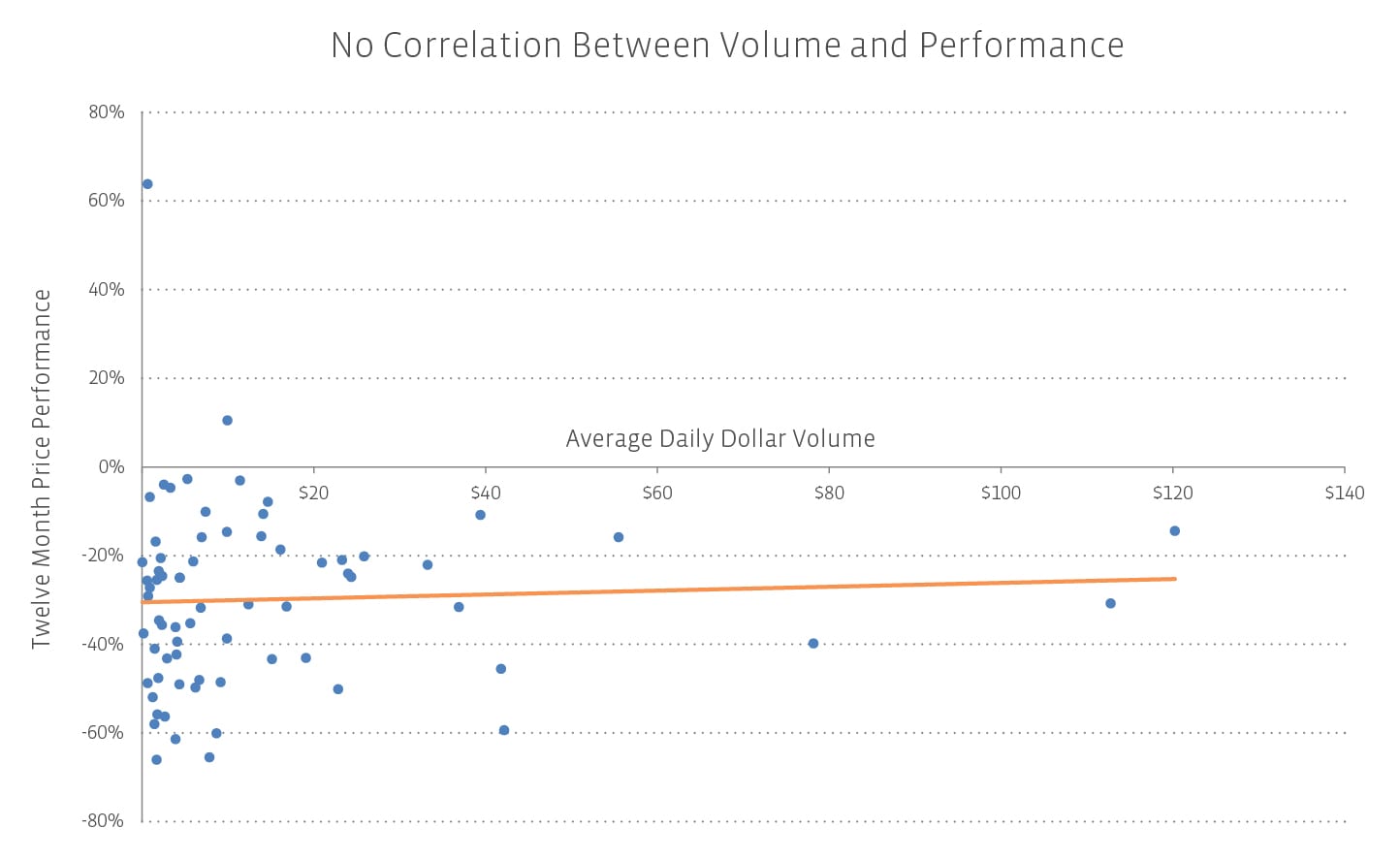

Since these names are industry MLP-beta proxies, perhaps instead of flight to quality, the explanation is simply that investors are exiting their most liquid positions in an effort to remove MLP exposure. To find out, we charted 12-month performance (August 29, 2014 – August 31, 2015) against average daily dollar volume.

If this was a flight to quality, we’d expect a positive correlation (upward sloping line). If it was a risk-off beta play , i.e. cutting MLP exposure quickly by selling the most liquid names first as a proxy for beta, a negative correlation (downward sloping line). Turns out, there’s no correlation. That doesn’t necessarily mean that these dynamics are absent, but rather that the sell-off can’t be explained by a single factor. For example, the market could be defining quality as greatest visibility to multi-year distribution growth, with an additional screen favoring demand-pull midstream assets.

{kind=link}