A core principle of finance is the tradeoff between risk and return. The higher the risk, the greater the potential return. Given this concept, investors may assume that equity indexes offering high yields must comprise of companies with weak balance sheets and low credit ratings, implying lower quality and higher risk. The credit quality of companies in Alerian and S-Network income indexes may be a positive surprise to investors who equate higher yields with low quality constituents. Specifically, this piece looks at the representation of companies with investment-grade credit ratings in select Alerian energy infrastructure indexes and the S-Network Sector Dividend Dogs Index (SDOGX).

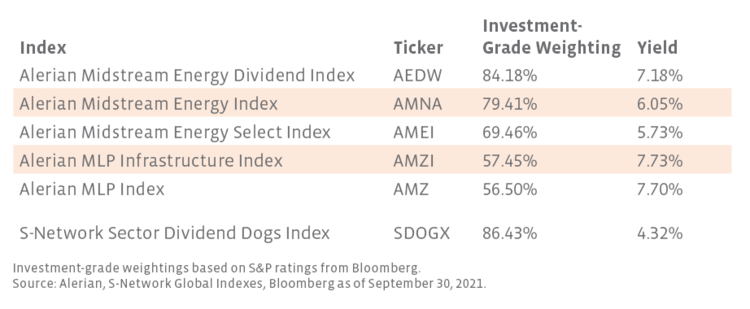

Within the Alerian energy infrastructure index suite, companies with investment-grade credit ratings represent approximately 57% of MLP indexes by weighting and upwards of 80% for broad midstream indexes as shown in the table below. The Alerian Midstream Energy Dividend Index (AEDW) has the highest weighting of investment-grade companies at just over 84%. Because the index is dividend weighted, it also boasts the highest yield among the midstream indexes that include both MLPs and corporations. MLPs have typically provided higher yields than midstream corporations in part because they do not pay taxes at the entity level (read more on MLP taxation). The Alerian MLP Index (AMZ) and Alerian MLP Infrastructure Index (AMZI) offer more generous yields than the broader midstream indexes but also have a lower representation of investment-grade companies.

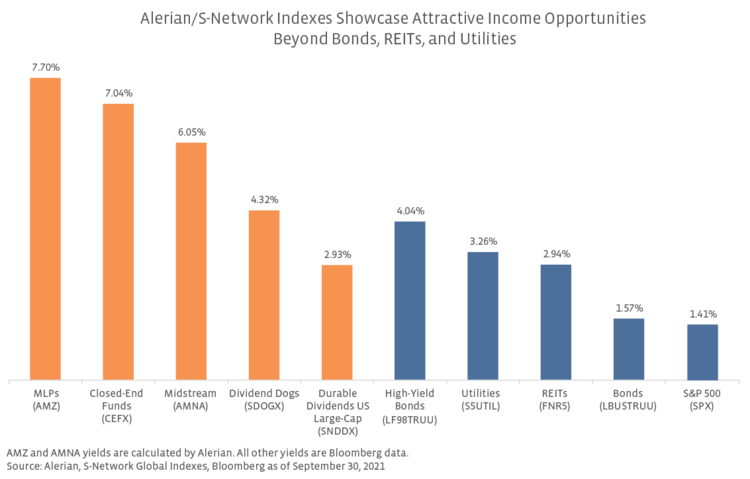

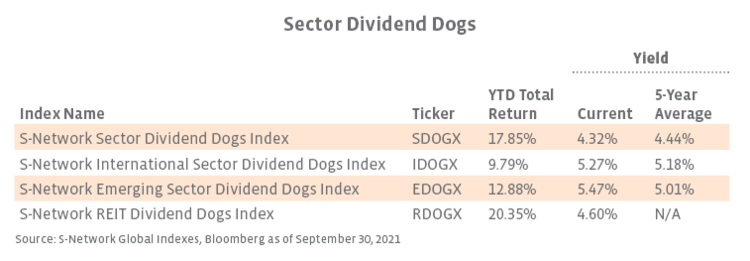

Shifting to a broad equity income index, the S-Network Sector Dividend Dogs Index (SDOGX) offers attractive income from quality companies, with investment-grade companies representing over 86% of the index by weighting. The starting universe for SDOGX is the S&P 500, and the five stocks with the highest yields in ten sectors (real estate is excluded) are selected for inclusion in the index during its annual reconstitution in December. Constituents are then equally weighted. At the end of September, SDOGX was yielding 4.32% compared to a yield of 1.41% for the S&P 500. Looking at total return through September, SDOGX has returned 17.85%, outpacing the S&P 500’s total return of 15.92%.

Finally, for additional context, the Bloomberg US Corporate High Yield Index (LF98TRUU) was yielding 4.04% at the end of September. By definition, securities included in the index cannot be investment grade. Admittedly, comparing bond and equity yields is a bit like comparing apples and oranges given different risk profiles and interest payments on bonds taking priority over dividend payments to equity holders. However, it is possible to attain more generous equity yields from companies with a higher credit quality relative to accepting a lower yield on bonds from companies with lower credit quality.

AMNA is the underlying index for the ETRACS Alerian Midstream Energy Index ETN (AMNA). AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR). AEDW is the underlying index for the Alerian Midstream Energy Dividend UCITS ETF (MMLP) and the ETRACS Alerian Midstream Energy High Dividend Index ETN (AMND). SDOGX is the underlying index for the ALPS Sector Dividend Dogs ETF (SDOG).

Current Yields vs. History

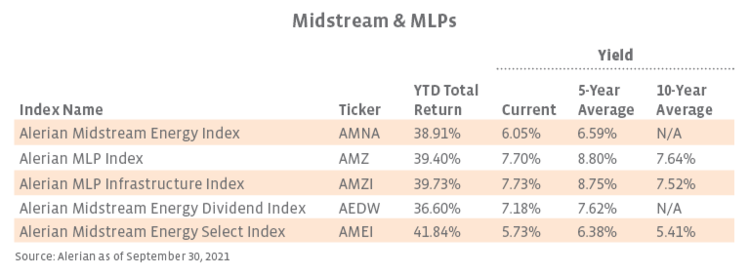

Following significant price improvement year-to-date through September, midstream yields are below 5-year historical averages but are modestly above the 10-year averages.

Of the S-Network Sector Dividend Dogs, IDOGX and EDOGX stand out for offering yields above their 5-year average. The current yield for SDOGX is just modestly below its 5-year average.

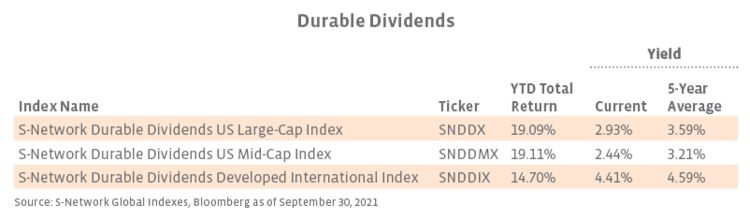

Multiple screens for dividend durability, including evaluating cash flows, EBITDA, and debt-to-equity ratios, help ensure reliable income from the durable dividend indexes. While current yields are below the 5-year average, they are well above the S&P 500’s current 1.41% yield.

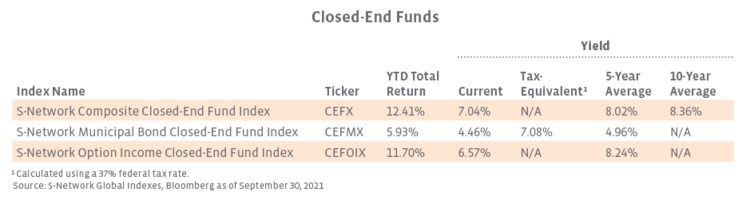

Though current yields are below historical averages, closed-end funds continue to represent an attractive option for enhancing the yield of an income-oriented portfolio.